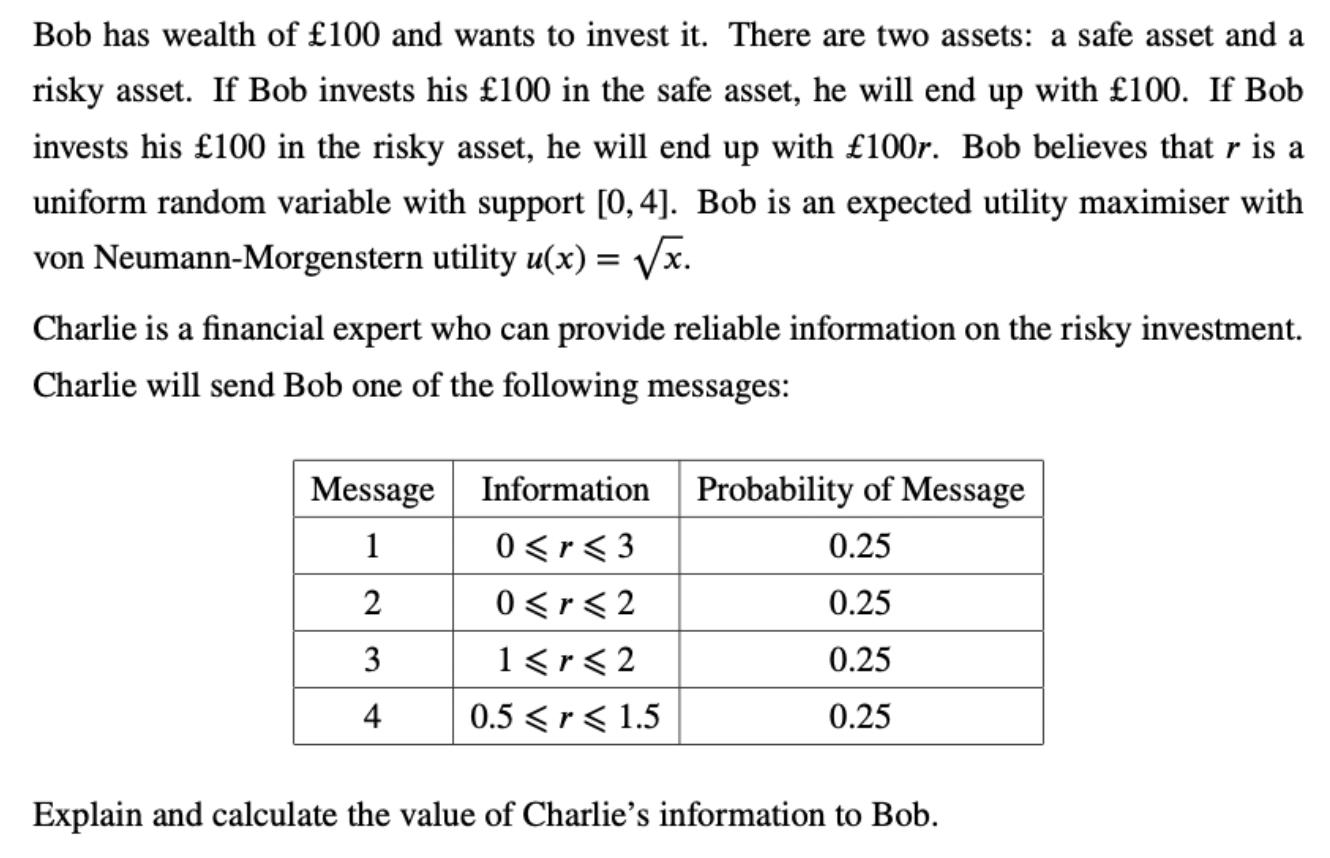

Bob has wealth of 100 and wants to invest it. There are two assets: a safe asset and a risky asset. If Bob invests

Bob has wealth of 100 and wants to invest it. There are two assets: a safe asset and a risky asset. If Bob invests his 100 in the safe asset, he will end up with 100. If Bob invests his 100 in the risky asset, he will end up with 100r. Bob believes that r is a uniform random variable with support [0,4]. Bob is an expected utility maximiser with von Neumann-Morgenstern utility u(x) = x. Charlie is a financial expert who can provide reliable information on the risky investment. Charlie will send Bob one of the following messages: Message 1 2 3 4 Information Probability of Message 0.25 0.25 0.25 0.25 0

Step by Step Solution

3.31 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER The value of Charlies information to Bob is 05 This is be...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Bernard Rosner

8th Edition

130526892X, 978-1305465510, 1305465512, 978-1305268920