Question

In accessing and cleansing client data, the auditor must consider the completeness and accuracy of the Information Produced by the Entity, as well as the

In accessing and cleansing client data, the auditor must consider the completeness and accuracy of the Information Produced by the Entity, as well as the appropriateness of the data for the purposes of the audit. This often involves summarizing the data and reconciling differences with reported client balances

a. What are the total sales included in the Product Sales Summary database? b. What are the total dollar amount of returns in the Product Returns Summary database? 2. In assessing the cleanliness of the data, are any of the following issues present in the database?

| Data Cleansing Issue | Number of Instances |

| Characters in dollar amount fields | |

| Negative dollar amounts | |

| Characters in PRODCAT | |

| Duplicate or missing months or categories |

- To obtain a better understanding of the data, complete the table below

| Question | Answer |

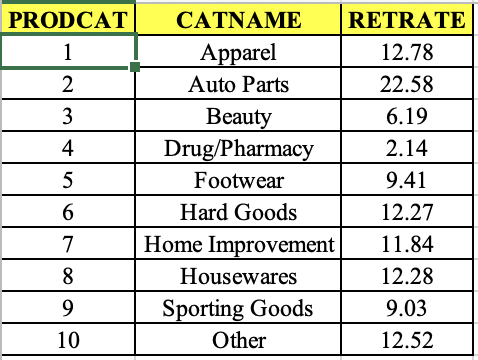

| Which Product Category (PRODCAT) had the highest dollar amount of sales? |

|

| Which Store (STOREID) had the highest dollar amount of returns during the month of February 2021? |

|

| Which Product Category (PRODCAT) had the highest percentage of returns relative to sales for the period presented? |

|

| Which Store (STOREID) had the highest percentage of returns relative to sales for the period presented? |

|

- Your firm has decided to try two approaches to estimating a valuation allowance for sales returns.

a. First, your firm decides to estimate that 10% of all sales will eventually be returned. Using the data provided and the monthly returns information above, estimate the Allowance for Sales Returns as of 1/31/2021. b. Second, your firm decides to use the return percentage information acquired from the auditor specialist. Using the data provided and the monthly returns information above, estimate the Allowance for Sales Returns as of 1/31/2021. 5. Based solely on your above analysis, select the most appropriate conclusion:

| |

| |

| |

|

Information For Use with Jerrys Discount Supplies

Jerrys Discount Supplies, Inc. (JDS) is a regional discount retailer that operates large discount stores in the southeastern United States. They compete directly in their markets with other discount stores. One hallmark of JDS is their generous return policy which allows customers to return any item at any time within 90 days for a full refund. JDS is also notable because they are much smaller in terms of number of stores they only have 20 stores throughout the region. Similar to many retailers, JDS uses an end of January fiscal year end to allow for less uncertainty in holiday season sales returns.

Although JDS allows customers great leniency in their return policy, their return rates have traditionally been in line with other retailers, and they estimate that approximately 5% of their returns are fraudulent, which is also in line with other retailers. This makes estimation of their sales return allowances reasonably predictable, according to company management.

JDS reports that historically, approximately 10% of all sales are returned. 70% of these returns occur in the month immediately following the sale, 25% occur within the next month, and the remaining 5% mostly happen in the third month. Later returns are immaterial since they are not according to policy. JDS estimates their returns using an analysis of economic conditions, historical average returns, as well as a variety of other sources. Because this method is difficult to validate and is not as precise as your firm prefers, your firm has decided to test the estimate by preparing an estimate and comparing it to the clients using data collected from other sources on return rates, as well as using subsequent client information.

Whenever an auditor uses Information Prepared by the Entity, that information must be tested for completeness and accuracy. For the purposes of the following exercises, please assume that your firm has already tested the completeness and accuracy of the Product Sales Summary and the Product Returns Summary and has determined that the amounts reported by the company are reasonable for purposes of your test of the sales return allowance account.

You have been assigned to audit the sales return and allowance account for JDS Retail for the fiscal year ended 1/31/2021. You have been provided with the following information:

- Information for use with JDS Retail document

- Return Rates database

- Product Sales Summary database for November, 2020 January, 2021

- Product Returns Summary database for November, 2020-January, 2021

- The client G/L reports an Allowance for Sales Returns of $3,100,000 as of 1/31/2021.

- Your firm has set materiality for the Allowance for Sales Returns account at $1,200,000

- For the purposes of this exercise, assume that sales occur uniformly throughout the year and month and that all months have 30 days.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wealth Mastery Unveiled By Marcus M Dawson A Millennial S Guide To Financial Freedom And Success

Authors: Marcus M. Dawson

1st Edition

979-8865054313