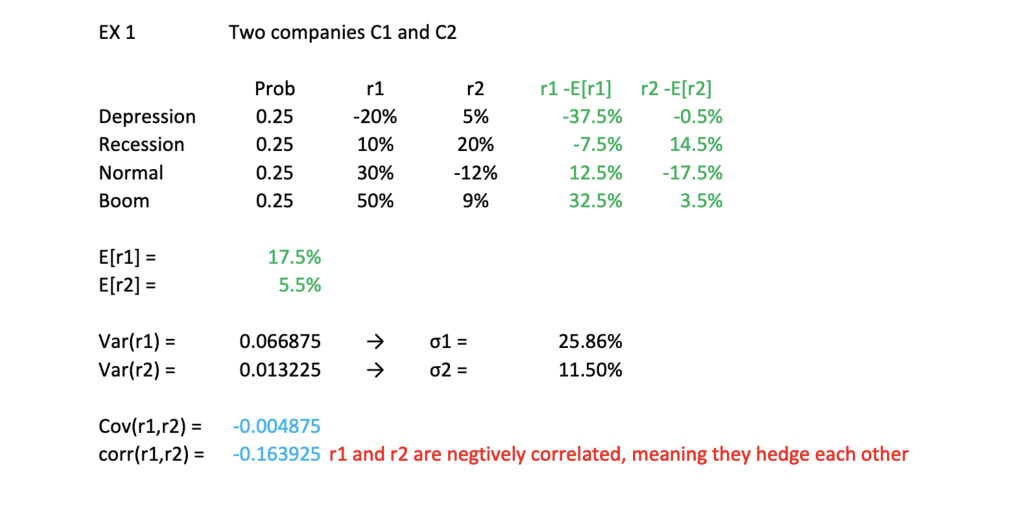

Question

In an Excel file, plot the risk (portfolio standard deviation) - expected return of the portfolio from two stocks from Examples 1 and 2 (refer

In an Excel file, plot the risk (portfolio standard deviation) - expected return of the portfolio from two stocks from Examples 1 and 2 (refer to the image below) such that:

1. The risk goes to the horizontal axis

2. The weight alpha of stock 1 should vary from 0 to 1, with increment of 0.05, to yield 20 point plot

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

De Gruyter Handbook Of Entrepreneurial Finance

Authors: David Lingelbach

1st Edition

3110726750,3110726351