Answered step by step

Verified Expert Solution

Question

1 Approved Answer

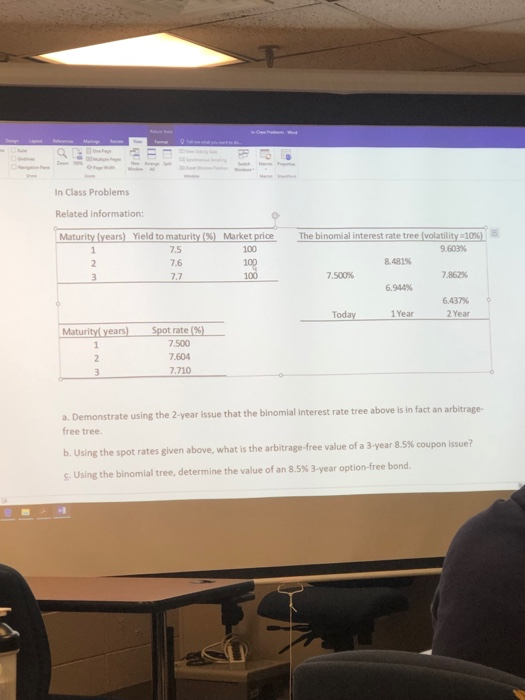

In Class Problems Related information: Maturity years Weldtomaturity(%) Market rice The binomial interest rate tree (volatility 110%) 100 100 100 603% 7.5 7.6 7.7 481%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Your Windows Infrastructure Intranet And Internet Security A Practical Audit Program For Assurance Professionals

Authors: Nwabueze Ohia

1st Edition

1521804133, 978-1521804131