Question

In early January 1991, Sarah Wolfe was in her office considering new goals and directions for her company for the coming year. Ms. Wolfe was

In early January 1991, Sarah Wolfe was in her office considering new goals and directions for her company for the coming year. Ms. Wolfe was the founder and CEO of the Beta Management Group, a small investment management company based in a Boston suburb. She dealt with a growing number of high-net-worth individual clients and had $25 million in assets under management.

Beta Management's stated goals were to enhance returns but reduce risks for clients via market timing. Given the small size of her accounts, the easiest way for her to maintain and adjust equity market exposure was to "index". She would keep a majority of Beta's funds in no-load, low-expense index funds (with the remainder in money market instruments), adjusting the level of market exposure between 50% and 99% of Beta's funds in an attempt to "time the market". She had toyed with using a few different index funds at first, but soon settled on exclusive use of Vanguard's Index 500 Trust, due to its extremely low expense ratio and its success a closely matching the return on the S&P 500 Index.

Ms. Wolfe had inquiries from some small institutions, and was hoping to expand her business in 1991. However, she had lost some potential new clients who had thought it unusual that Beta Management used only an index mutual fund and picked none of its own stocks. As a result, one of her New Year's resolutions had been to begin looking at some individual stocks for possible purchase for Beta's equity portfolio. She would focus on smaller stocks, since she didn't want to compete with larger, analyst-staffed funds on their own turf, and also because she already had exposure to the S&P 500 stocks through investment in the index fund.

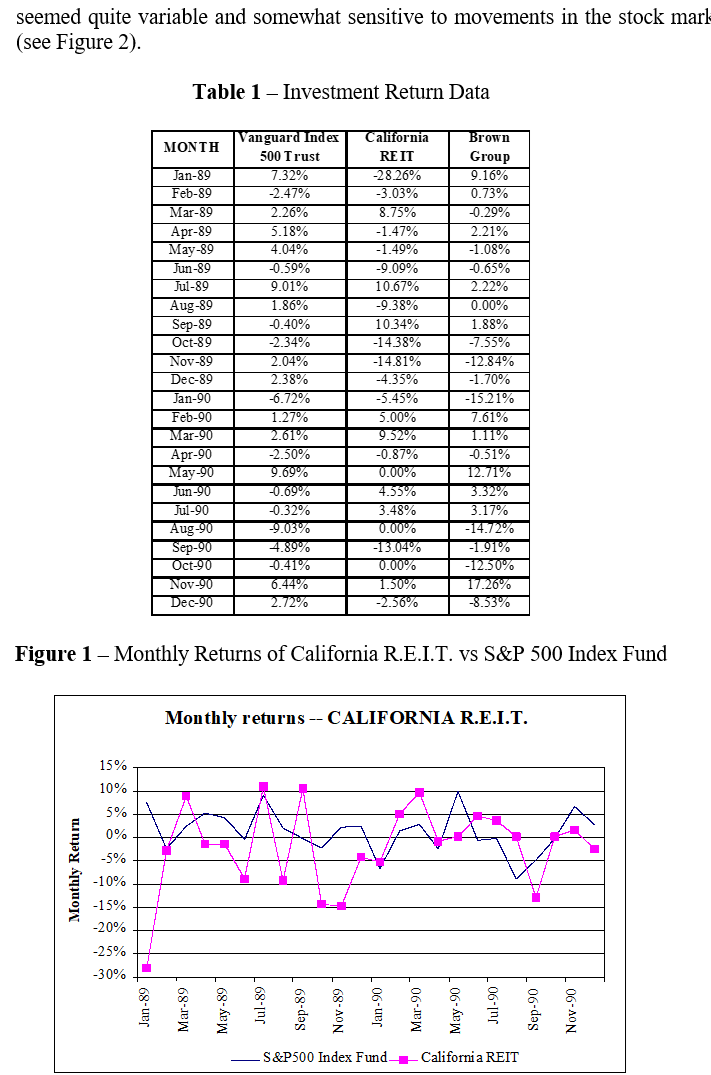

The report in front of her showed that as of January 4, 1991, Beta Management had 79.2% of its $25 million invested in the Vanguard fund. As a first step toward the goal stated above, Ms. Wolfe was considering immediately increasing her equity exposure to 80% with the purchase of one of two stocks recommended by her newly hired analyst:

- California R.E.I.T. was a real estate investment trust that made equity and mortgage investments in income-producing properties in Arizona, California, and Washington. Its investments and stock price had been badly damaged by the "World Series" earthquake of 1989 and the downturn in California real estate values (see Table 1), but Ms. Wolfe viewed it as a good value, but noticed that it was an extremely volatile stock (see Figure 1).

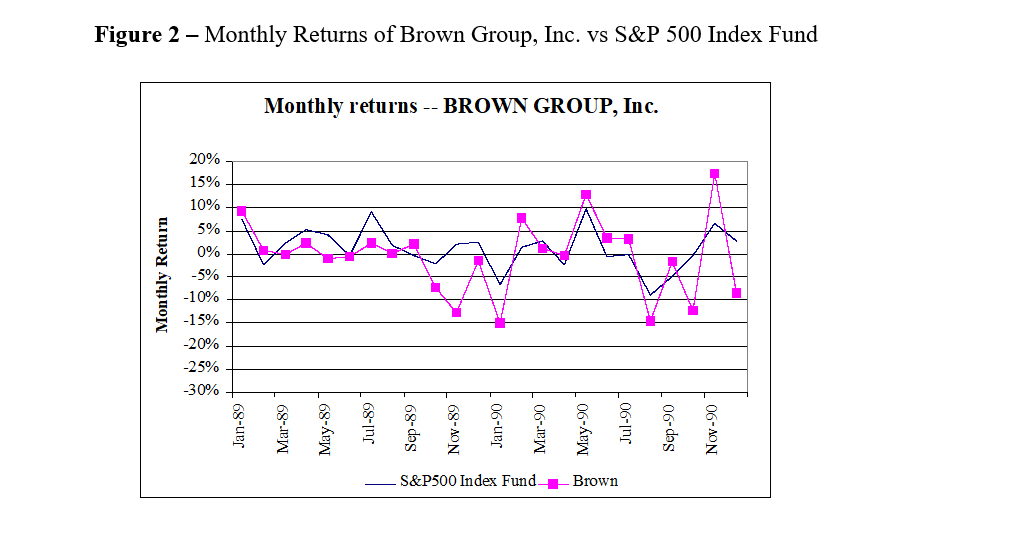

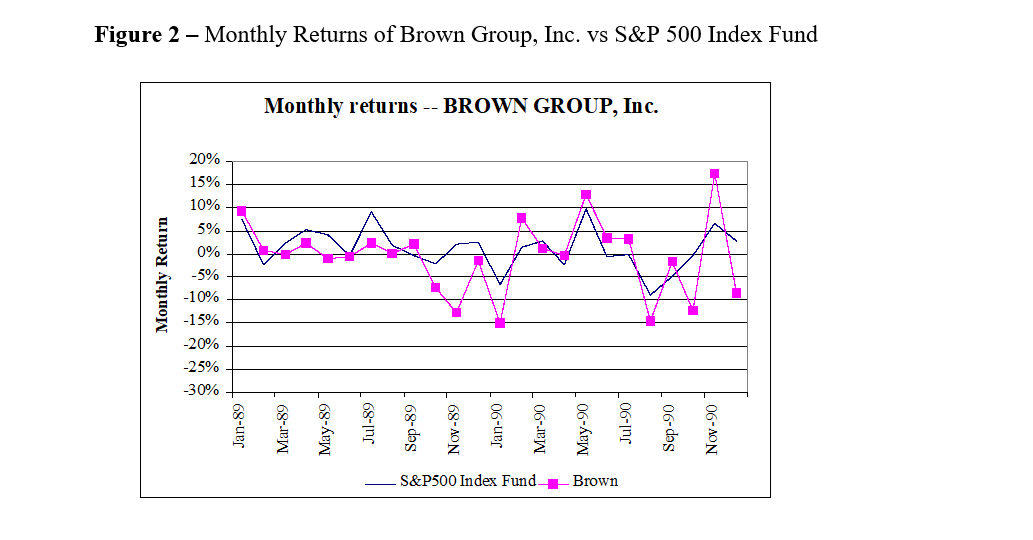

- Brown Group, Inc. was one of the largest manufacturers and retailers of branded footwear, and had been undergoing a major restructuring program since 1989. Earnings dropped in 1989 but had stayed positive and steady; the stock price had dropped substantially in late 1989 and late 1990 (see Table 1). Ms. Wolfe liked Brown's steady cash flow and earnings. She noted, though, that Brown's stock price seemed quite variable and somewhat sensitive to movements in the stock market (see Figure 2).

Ms. Wolfe felt that now was the right time to begin her program of adding individual stock investments and increasing her equity position. A $200,000 purchase of one of these stocks would increase her total equity exposure to $20 million. Still, she had doubts. She was quite worried about the variability in individual stocks in general, and these stocks in particular. After all, she had always promised her clients reasonable returns with a focus on keeping their exposure to risk under control.

Questions:

I would like you to help Ms. Wolfe elucidate her doubts, by answering the following questions:

1.Calculate the volatility of the stock returns of California REIT and Brown Group during the past 2 years. How variable are they compared with Vanguard Index 500 Trust? Which stock appears to be the riskiest? Which investment do you think needs to provide the highest return to make investors interested in buying it?

2.Suppose Beta's position had been 99% of equity funds invested in the index fund, and 1% in the individual stocks. Calculate the volatility of this portfolio using each stock at a time (one which is 1% in California REIT and 99% in equity fund, other which is 1% in Brown Group and 99% in equity fund). What does each stock do to the overall risk of this portfolio, and which stock is the riskiest?[Hint: think about contribution to systematic risk of the portfolio.] Explain how this makes sense in view of your answer to Question #1 above?

3.Perform a regression of each stock's monthly returns on the Index returns to compute the "beta" for each stock. How does this relate to the situation described in Question #2 above?

4..How might the expected return for each stock relate to its riskiness? How much will Ms. Wolfe (a diversified investor) require/expect to earn on each stock (given its riskiness) in order to hold it?

Begin by considering a portfolio that is 99% invested in equity funds and 1% invested in cash.What is its standard deviation?If Ms. Wolfe invests the 1% in California REIT, what would the return on California REIT have to be (relative to the risk-free rate) to maintain the same reward-to-risk trade off?And for Brown Group?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Partial Differential Equations For Scientists And Engineers

Authors: Stanley J Farlow

1st Edition

0486134733, 9780486134734