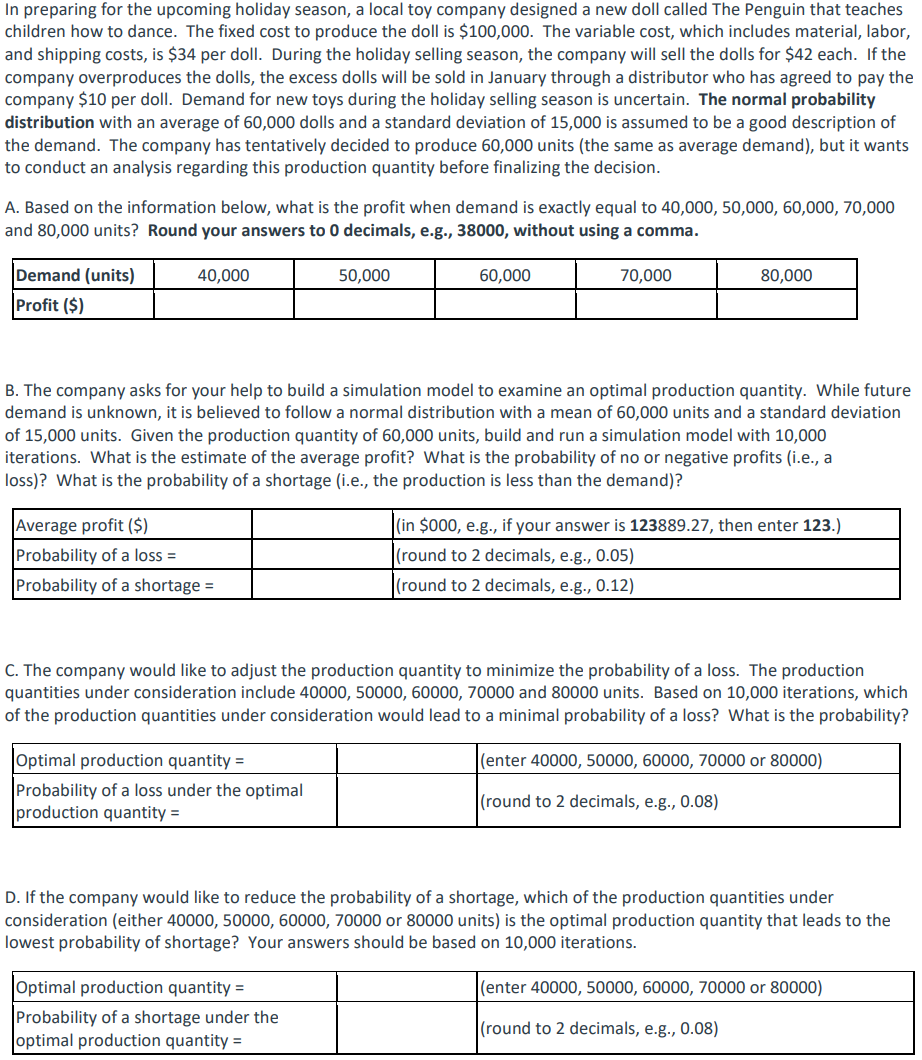

In preparing for the upcoming holiday season, a local toy company designed a new doll called The Penguin that teaches children how to dance. The fixed cost to produce the doll is $100,000. The variable cost, which includes material, labor, and shipping costs, is $34 per doll. During the holiday selling season, the company will sell the dolls for $42 each. If the company overproduces the dolls, the excess dolls will be sold in January through a distributor who has agreed to pay the company $10 per doll. Demand for new toys during the holiday selling season is uncertain. The normal probability distribution with an average of 60,000 dolls and a standard deviation of 15,000 is assumed to be a good description of the demand. The company has tentatively decided to produce 60,000 units (the same as average demand), but it wants to conduct an analysis regarding this production quantity before finalizing the decision. A. Based on the information below, what is the profit when demand is exactly equal to 40,000, 50,000, 60,000, 70,000 and 80,000 units? Round your answers to 0 decimals, e.g., 38000, without using a comma. 40,000 50,000 60,000 70,000 80,000 Demand (units) Profit ($) B. The company asks for your help to build a simulation model to examine an optimal production quantity. While future demand is unknown, it is believed to follow a normal distribution with a mean of 60,000 units and a standard deviation of 15,000 units. Given the production quantity of 60,000 units, build and run a simulation model with 10,000 iterations. What is the estimate of the average profit? What is the probability of no or negative profits (i.e., a loss)? What is the probability of a shortage (i.e., the production is less than the demand)? Average profit ($) Probability of a loss = Probability of a shortage = (in $000, e.g., if your answer is 123889.27, then enter 123.) (round to 2 decimals, e.g., 0.05) (round to 2 decimals, e.g., 0.12) C. The company would like to adjust the production quantity to minimize the probability of a loss. The production quantities under consideration include 40000, 50000, 60000, 70000 and 80000 units. Based on 10,000 iterations, which of the production quantities under consideration would lead to a minimal probability of a loss? What is the probability? (enter 40000, 50000, 60000, 70000 or 80000) Optimal production quantity = Probability of a loss under the optimal production quantity = (round to 2 decimals, e.g., 0.08) D. If the company would like to reduce the probability of a shortage, which of the production quantities under consideration (either 40000, 50000, 60000, 70000 or 80000 units) is the optimal production quantity that leads to the lowest probability of shortage? Your answers should be based on 10,000 iterations. (enter 40000, 50000, 60000, 70000 or 80000) Optimal production quantity = Probability of a shortage under the optimal production quantity = (round to 2 decimals, e.g., 0.08) In preparing for the upcoming holiday season, a local toy company designed a new doll called The Penguin that teaches children how to dance. The fixed cost to produce the doll is $100,000. The variable cost, which includes material, labor, and shipping costs, is $34 per doll. During the holiday selling season, the company will sell the dolls for $42 each. If the company overproduces the dolls, the excess dolls will be sold in January through a distributor who has agreed to pay the company $10 per doll. Demand for new toys during the holiday selling season is uncertain. The normal probability distribution with an average of 60,000 dolls and a standard deviation of 15,000 is assumed to be a good description of the demand. The company has tentatively decided to produce 60,000 units (the same as average demand), but it wants to conduct an analysis regarding this production quantity before finalizing the decision. A. Based on the information below, what is the profit when demand is exactly equal to 40,000, 50,000, 60,000, 70,000 and 80,000 units? Round your answers to 0 decimals, e.g., 38000, without using a comma. 40,000 50,000 60,000 70,000 80,000 Demand (units) Profit ($) B. The company asks for your help to build a simulation model to examine an optimal production quantity. While future demand is unknown, it is believed to follow a normal distribution with a mean of 60,000 units and a standard deviation of 15,000 units. Given the production quantity of 60,000 units, build and run a simulation model with 10,000 iterations. What is the estimate of the average profit? What is the probability of no or negative profits (i.e., a loss)? What is the probability of a shortage (i.e., the production is less than the demand)? Average profit ($) Probability of a loss = Probability of a shortage = (in $000, e.g., if your answer is 123889.27, then enter 123.) (round to 2 decimals, e.g., 0.05) (round to 2 decimals, e.g., 0.12) C. The company would like to adjust the production quantity to minimize the probability of a loss. The production quantities under consideration include 40000, 50000, 60000, 70000 and 80000 units. Based on 10,000 iterations, which of the production quantities under consideration would lead to a minimal probability of a loss? What is the probability? (enter 40000, 50000, 60000, 70000 or 80000) Optimal production quantity = Probability of a loss under the optimal production quantity = (round to 2 decimals, e.g., 0.08) D. If the company would like to reduce the probability of a shortage, which of the production quantities under consideration (either 40000, 50000, 60000, 70000 or 80000 units) is the optimal production quantity that leads to the lowest probability of shortage? Your answers should be based on 10,000 iterations. (enter 40000, 50000, 60000, 70000 or 80000) Optimal production quantity = Probability of a shortage under the optimal production quantity = (round to 2 decimals, e.g., 0.08)