Answered step by step

Verified Expert Solution

Question

1 Approved Answer

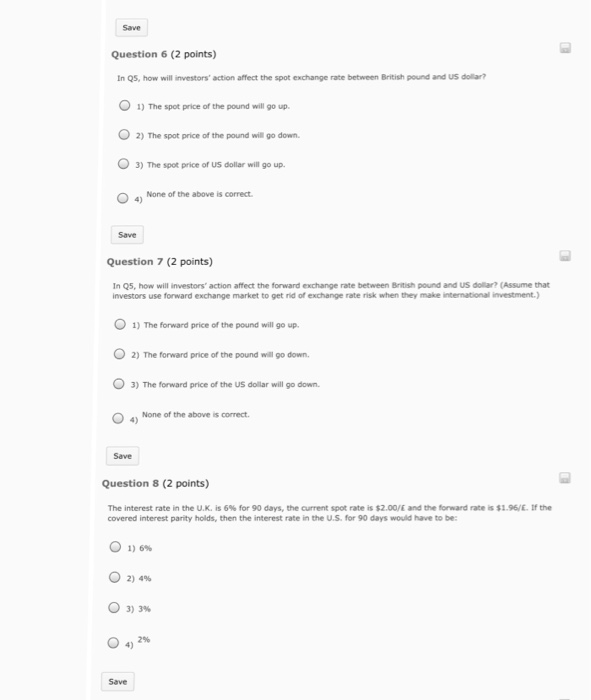

In Q5, how will investors' action affect the spot exchange rate between British pound and US dollar? The spot price of the pound will go

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Social Media Handbook For Financial Advisors

Authors: Matthew Halloran

1st Edition

1118208013, 978-1118208014