Answered step by step

Verified Expert Solution

Question

1 Approved Answer

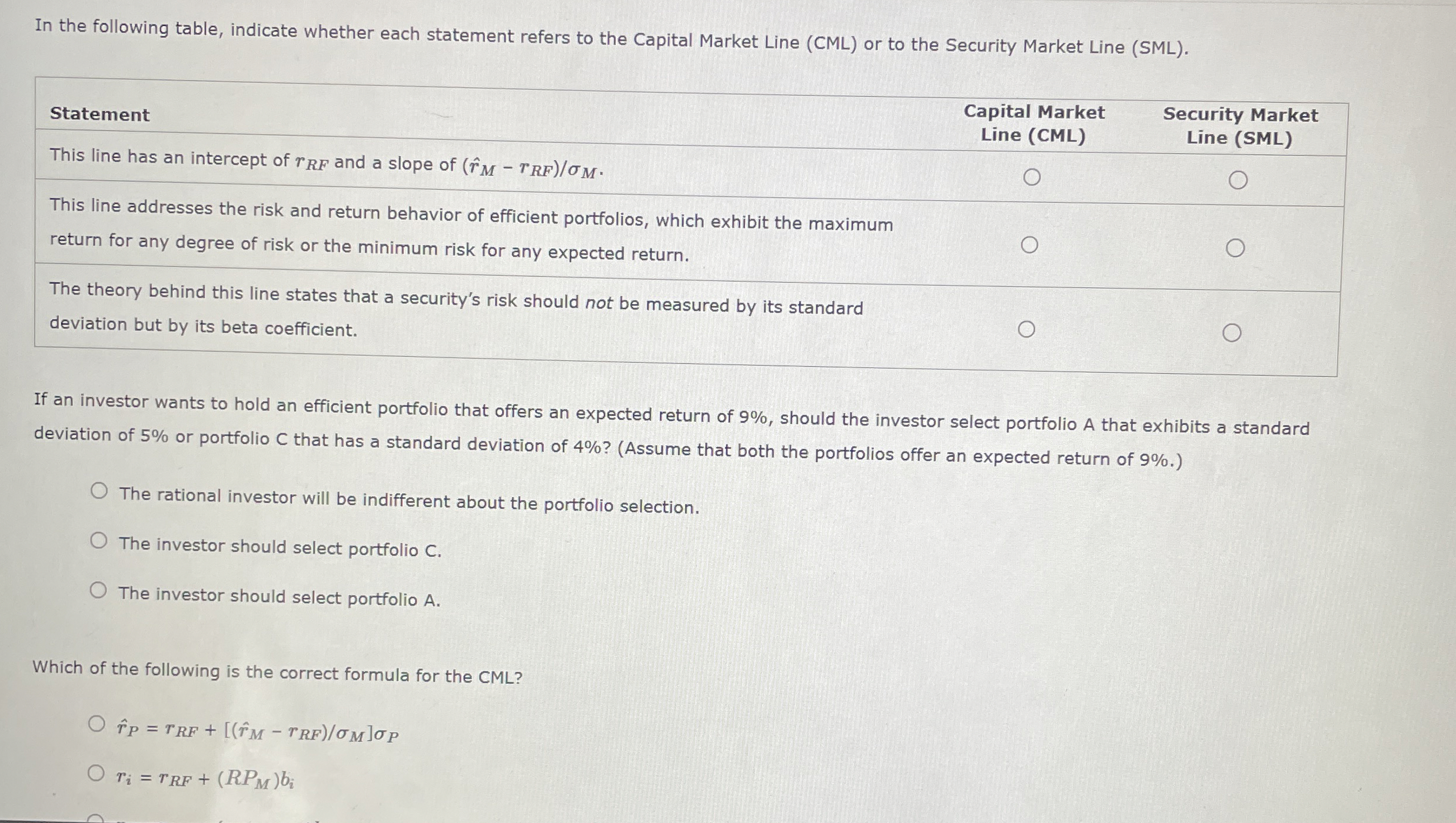

In the following table, indicate whether each statement refers to the Capital Market Line ( CML ) or to the Security Market Line ( SML

In the following table, indicate whether each statement refers to the Capital Market Line CML or to the Security Market Line SML

Statement

Capital Market

Security Market

Line CML

This line has an intercept of and a slope of

This line addresses the risk and return behavior of efficient portfolios, which exhibit the maximum

return for any degree of risk or the minimum risk for any expected return.

The theory behind this line states that a securitys risk should not be measured by its standard deviation but by its beta coefficient.

If an investor wants to hold an efficient portfolio that offers an expected return of should the investor select portfolio A that exhibits a standard deviation of or portfolio that has a standard deviation of Assume that both the portfolios offer an expected return of

The rational investor will be indifferent about the portfolio selection.

The investor should select portfolio C

The investor should select portfolio A

Which of the following is the correct formula for the CML

hat

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mein Ultimativer Weihnachts Planer

Authors: Zizo Nimane

1st Edition

B0CM2J8GTG