Question

In this question, please assume that all bonds pay coupon annually, and the yield is on an annual basis. You are considering a callable corporate

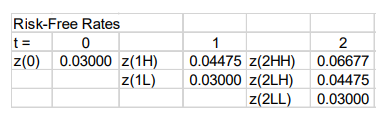

In this question, please assume that all bonds pay coupon annually, and the yield is on an annual basis. You are considering a callable corporate bond with 3 years to maturity and the coupon rate of 5.5% (paid annually), callable in one year at 100 (per 100 par). The bond currently trades at 101.5. The benchmark 3-year Treasury note trades at 3.7665% yield. Use the risk-free rate tree below to answer the following questions:

d. If the interest rates significantly decline, would the bonds price change more or less than that of the 3-year Treasury note? How about the bonds duration?

Risk-Free Rates t= 0 z(0) 0.03000 z(1H) z(1L) 0.04475 z(2HH) 0.03000 z(2LH) Z(2LL) 0.06677 0.04475 0.03000 Risk-Free Rates t= 0 z(0) 0.03000 z(1H) z(1L) 0.04475 z(2HH) 0.03000 z(2LH) Z(2LL) 0.06677 0.04475 0.03000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles And Applications

Authors: Dr. S. Kr. Paul, Prof. Chandrani Paul

1st Edition

1647251664, 9781647251666