Answered step by step

Verified Expert Solution

Question

1 Approved Answer

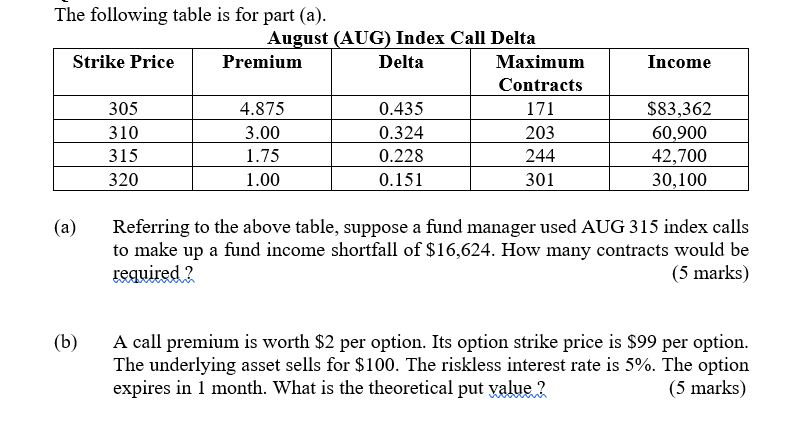

Income The following table is for part (a). August (AUG) Index Call Delta Strike Price Premium Delta Maximum Contracts 305 4.875 0.435 171 310 3.00

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

EPA Should Improve Timeliness For Resolving Audits Under Appeal

Authors: U.S. Environmental Protection Agency

1st Edition

1500105783, 978-1500105785