Incorrect answers provided

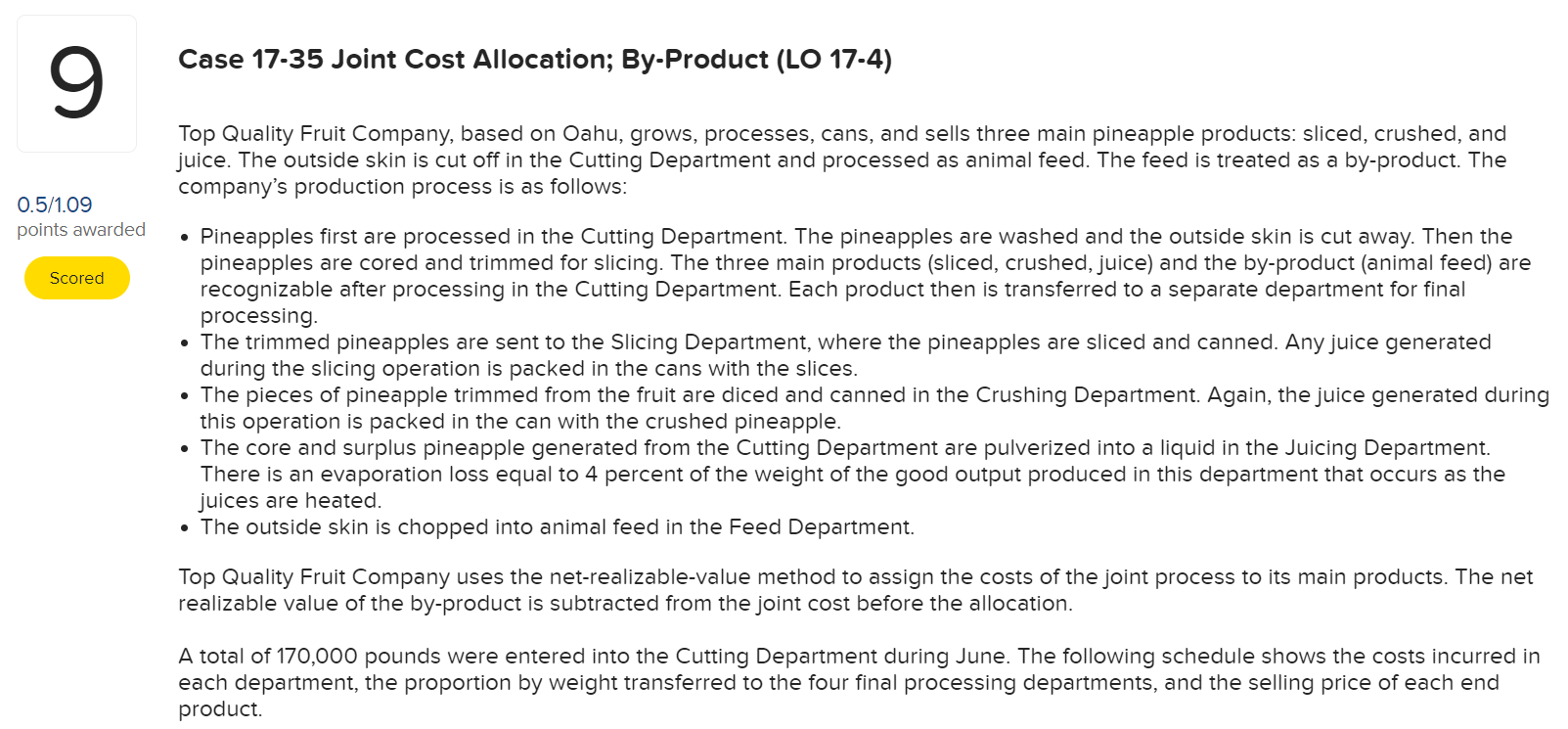

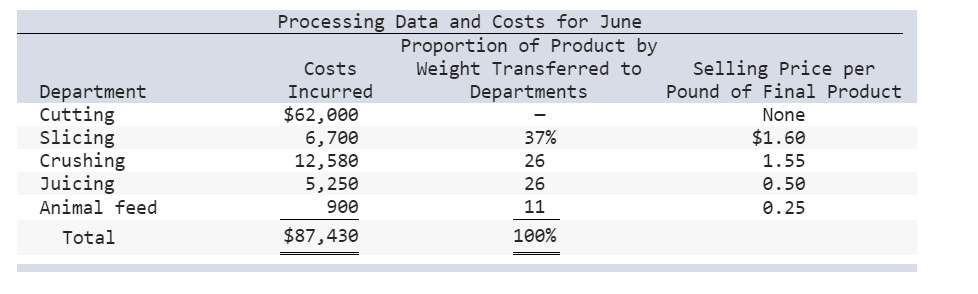

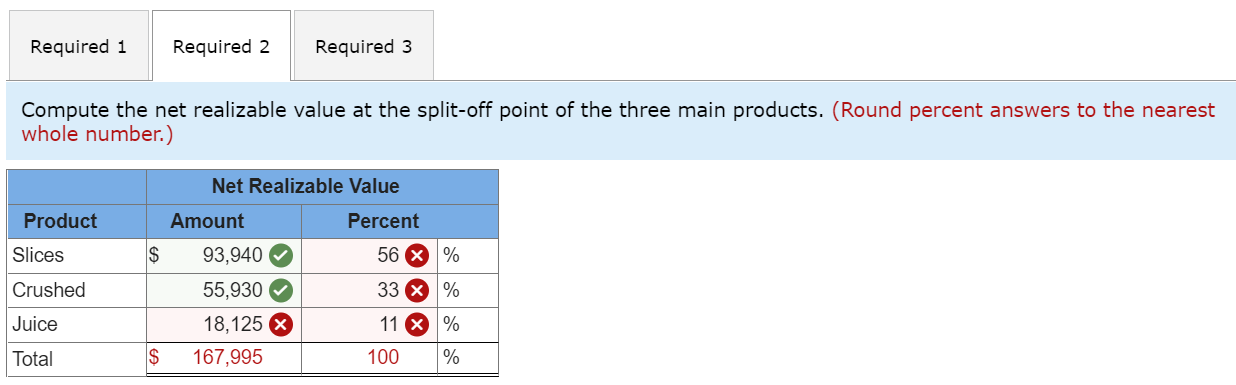

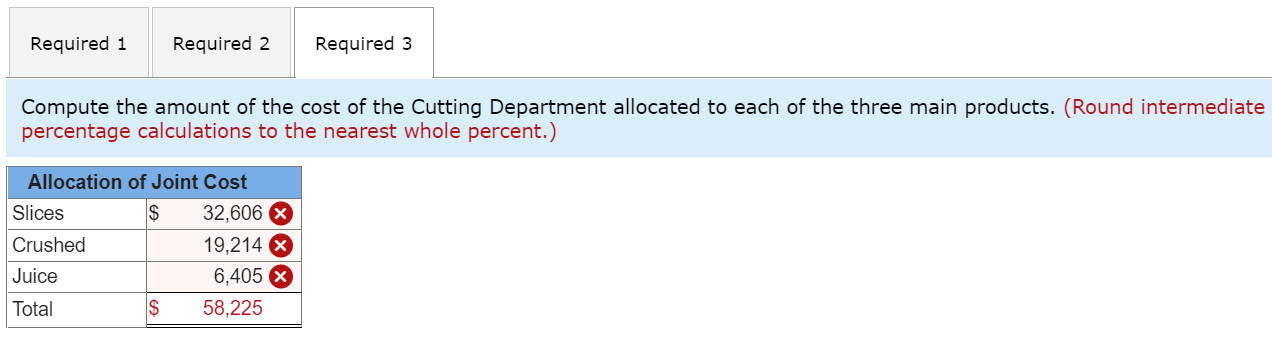

Case 17-35 Joint Cost Allocation; By-Product (LO 17-4) 9 Top Quality Fruit Company, based on Oahu, grows, processes, cans, and sells three main pineapple products: sliced, crushed, and juice. The outside skin is cut off in the Cutting Department and processed as animal feed. The feed is treated as a by-product. The company's production process is as follows: 0.5/1.09 points awarded . Scored Pineapples first are processed in the Cutting Department. The pineapples are washed and the outside skin is cut away. Then the pineapples are cored and trimmed for slicing. The three main products (sliced, crushed, juice) and the by-product (animal feed) are recognizable after processing in the Cutting Department. Each product then is transferred to a separate department for final processing. The trimmed pineapples are sent to the Slicing Department, where the pineapples are sliced and canned. Any juice generated during the slicing operation is packed in the cans with the slices. The pieces of pineapple trimmed from the fruit are diced and canned in the Crushing Department. Again, the juice generated during this operation is packed in the can with the crushed pineapple. The core and surplus pineapple generated from the Cutting Department are pulverized into a liquid in the Juicing Department. There is an evaporation loss equal to 4 percent of the weight of the good output produced in this department that occurs as the juices are heated. The outside skin is chopped into animal feed in the Feed Department. Top Quality Fruit Company uses the net-realizable-value method to assign the costs of the joint process to its main products. The net realizable value of the by-product is subtracted from the joint cost before the allocation. A total of 170,000 pounds were entered into the Cutting Department during June. The following schedule shows the costs incurred in each department, the proportion by weight transferred to the four final processing departments, and the selling price of each end product. Department Cutting Slicing Crushing Juicing Animal feed Total Processing Data and costs for June Proportion of Product by Costs Weight Transferred to Selling Price per Incurred Departments Pound of Final Product $62,000 None 6,700 37% $1.60 12,580 26 1.55 5,250 26 0.50 900 11 0.25 $87,430 100% Required 1 Required 2 Required 3 Compute the net realizable value at the split-off point of the three main products. (Round percent answers to the nearest whole number.) Net Realizable Value Product Amount Percent Slices $ 93,940 Crushed 56 X % 33 X % 11 X % 100 % 55,930 18,125 X 167,995 Juice Total $ Required 1 Required 2 Required 3 Compute the amount of the cost of the Cutting Department allocated to each of the three main products. (Round intermediate percentage calculations to the nearest whole percent.) Allocation of Joint Cost Slices $ 32,606 X Crushed 19,214 X Juice 6,405 X Total $ 58,225