Instructions: Analyze and explain the Case Study. In the explanation you will be providing different concepts between the two variable that being compared. The idea about Relevant Costs Decision Making must be part of the things need to consider and thoughts to be justified. It'll be better to highlight those concepts.

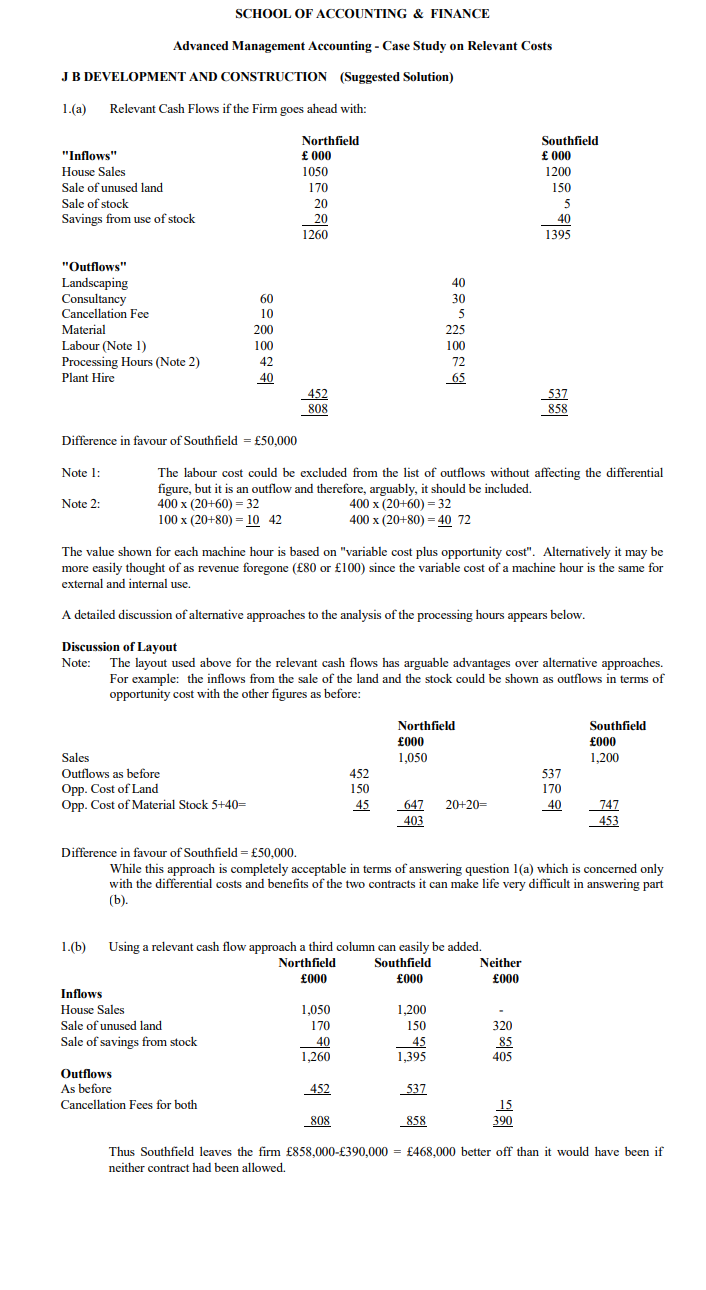

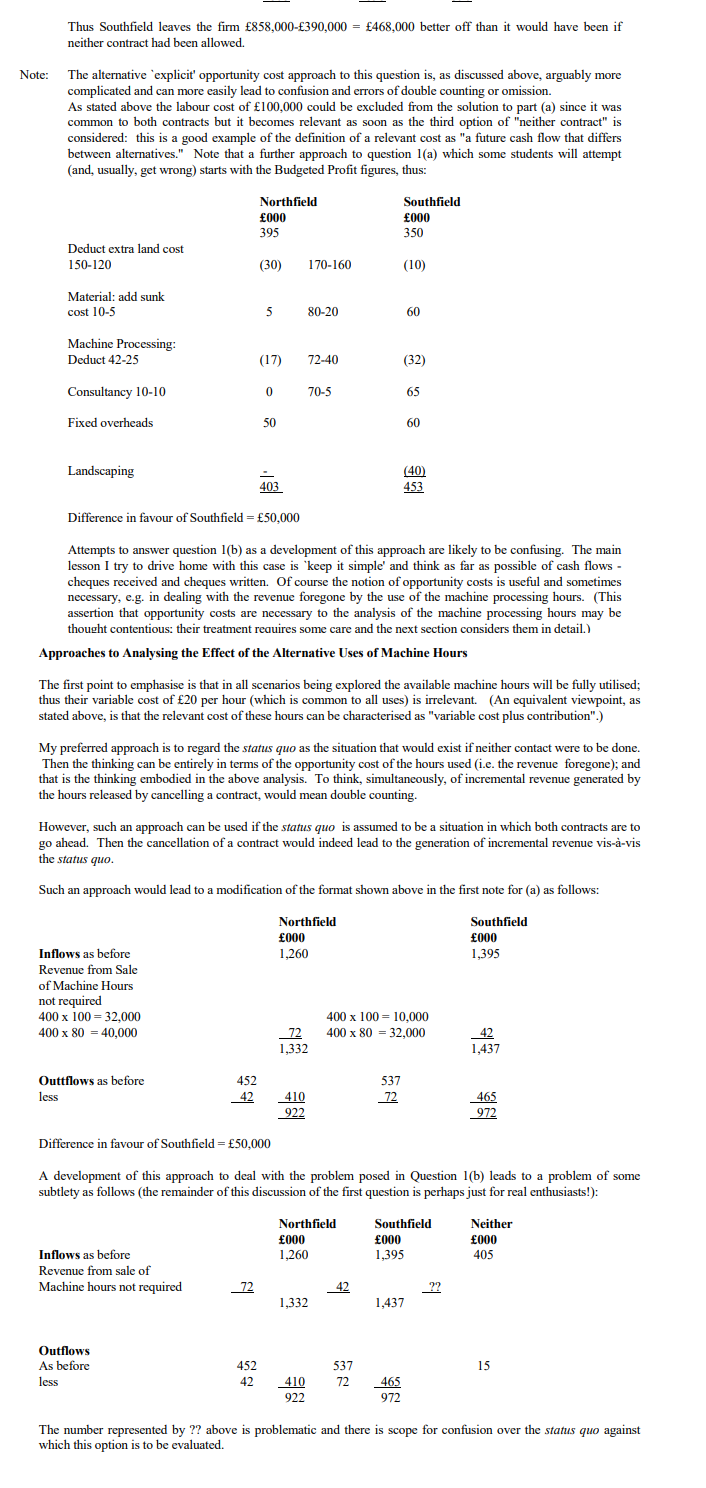

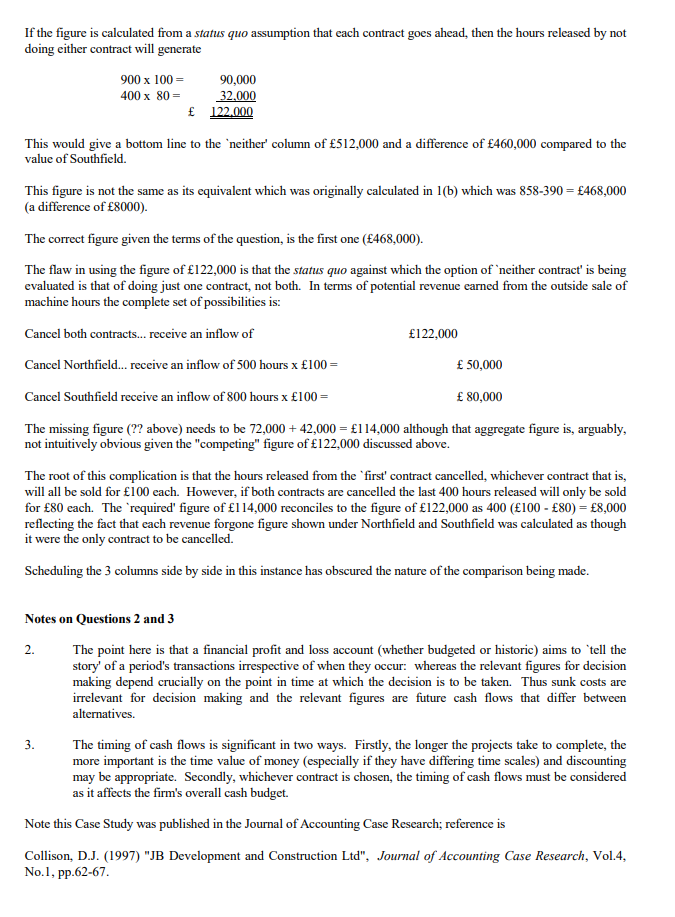

SCHOOL OF ACCOUNTING & FINANCE Advanced Management Accounting - Case Study on Relevant Costs JB DEVELOPMENT AND CONSTRUCTION (Suggested Solution) 1.(a) Relevant Cash Flows if the Firm goes ahead with: "Inflows" House Sales Sale of unused land Sale of stock Savings from use of stock Northfield 000 1050 170 20 20 1260 Southfield 000 1200 150 5 40 1395 . "Outflows" Landscaping Consultancy Cancellation Fee Material Labour (Note 1) Processing Hours (Note 2) Plant Hire 60 10 200 100 42 40 40 30 5 225 100 72 65 452 808 537 858 Difference in favour of Southfield = 50,000 Note 1: The labour cost could be excluded from the list of outflows without affecting the differential figure, but it is an outflow and therefore, arguably, it should be included. 400 x (20+60) = 32 400 x (20+60) = 32 100 x (20+80) = 10 42 400 x (20+80) = 40 72 Note 2: The value shown for each machine hour is based on "variable cost plus opportunity cost". Alternatively it may be more easily thought of as revenue foregone (80 or 100) since the variable cost of a machine hour is the same for external and internal use. A detailed discussion of alternative approaches to the analysis of the processing hours appears below. Discussion of Layout Note: The layout used above for the relevant cash flows has arguable advantages over alternative approaches. For example: the inflows from the sale of the land and the stock could be shown as outflows in terms of opportunity cost with the other figures as before: Northfield 000 1,050 Southfield 000 1.200 Sales Outflows as before Opp. Cost of Land Opp. Cost of Material Stock 5+40= 452 150 45 537 170 40 20+20= 647 403 747 453 Difference in favour of Southfield = 50,000. While this approach is completely acceptable in terms of answering question 1(a) which is concerned only with the differential costs and benefits of the two contracts it can make life very difficult in answering part (b) 1.(b) Using a relevant cash flow approach a third column can easily be added. Northfield Southfield Neither 000 000 000 Inflows House Sales 1,050 1,200 Sale of unused land 170 150 320 Sale of savings from stock 40 45 85 1.260 1,395 405 Outflows As before 452 537 Cancellation Fees for both 15 808 858 390 Thus Southfield leaves the firm 858,000-390,000 = 468,000 better off than it would have been if neither contract had been allowed. Thus Southfield leaves the firm 858,000-390,000 = 468,000 better off than it would have been if neither contract had been allowed. Note: The alternative 'explicit' opportunity cost approach to this question is, as discussed above, arguably more complicated and can more easily lead to confusion and errors of double counting or omission. As stated above the labour cost of 100,000 could be excluded from the solution to part (a) since it was to both contracts but it becomes relevant as soon as the third option of "neither contract" is considered: this is a good example of the definition of a relevant cost as "a future cash flow that differs between alternatives." Note that a further approach to question 1(a) which some students will attempt (and, usually, get wrong) starts with the Budgeted Profit figures, thus: common Northfield 000 395 Southfield 000 350 Deduct extra land cost 150-120 (30) 170-160 (10) Material: add sunk cost 10-5 5 80-20 60 Machine Processing: Deduct 42-25 (17) 72-40 (32) Consultancy 10-10 0 70-5 65 Fixed overheads 50 60 Landscaping (40) 453 403 Difference in favour of Southfield = 50,000 Attempts to answer question 1(b) as a development of this approach are likely to be confusing. The main lesson I try to drive home with this case is keep it simple and think as far as possible of cash flows - cheques received and cheques written. Of course the notion of opportunity costs is useful and sometimes necessary, e.g. in dealing with the revenue foregone by the use of the machine processing hours. (This assertion that opportunity costs are necessary to the analysis of the machine processing hours may be thought contentious: their treatment requires some care and the next section considers them in detail.) Approaches to Analysing the Effect of the Alternative Uses of Machine Hours The first point to emphasise is that in all scenarios being explored the available machine hours will be fully utilised; thus their variable cost of 20 per hour (which is common to all uses) is irrelevant. (An equivalent viewpoint, as stated above, is that the relevant cost of these hours can be characterised as "variable cost plus contribution".) My preferred approach is to regard the status quo as the situation that would exist if neither contact were to be done. Then the thinking can be entirely in terms of the opportunity cost of the hours used (i.e. the revenue foregone); and that is the thinking embodied in the above analysis. To think, simultaneously, of incremental revenue generated by the hours released by cancelling a contract, would mean double counting. However, such an approach can be used if the status quo is assumed to be a situation in which both contracts are to go ahead. Then the cancellation of a contract would indeed lead to the generation of incremental revenue vis--vis the status quo. Such an approach would lead to a modification of the format shown above in the first note for (a) as follows: Northfield 000 Southfield 000 1,395 1,260 Inflows as before Revenue from Sale of Machine Hours not required 400 x 100 = 32,000 400 x 80 = 40,000 400 x 100 = 10,000 400 x 80 = 32,000 _72 1,332 42 1,437 Outtflows as before less 452 42 410 922 537 72 465 972 Difference in favour of Southfield = 50,000 A development of this approach to deal with the problem posed in Question 1(b) leads to a problem of some subtlety as follows (the remainder of this discussion of the first question is perhaps just for real enthusiasts!): Northfield 000 Southfield 000 1,395 Neither 000 405 1,260 Inflows as before Revenue from sale of Machine hours not required 72 42 42 ?? 1,332 1,437 Outflows As before less 15 452 42 537 72 410 922 465 972 The number represented by ?? above is problematic and there is scope for confusion over the status quo against which this option is to be evaluated. If the figure is calculated from a status quo assumption that each contract goes ahead, then the hours released by not doing either contract will generate 900 x 100 = 90,000 400 x 80 = 32.000 122.000 This would give a bottom line to the 'neither' column of 512,000 and a difference of 460,000 compared to the value of Southfield. This figure is not the same as its equivalent which was originally calculated in 1(b) which was 858-390 = 468,000 (a difference of 8000). The correct figure given the terms of the question, is the first one (468,000). The flaw in using the figure of 122,000 is that the status quo against which the option of 'neither contract' is being evaluated is that of doing just one contract, not both. In terms of potential revenue earned from the outside sale of machine hours the complete set of possibilities is: Cancel both contracts... receive an inflow of 122,000 Cancel Northfield... receive an inflow of 500 hours x 100= 50,000 Cancel Southfield receive an inflow of 800 hours x 100 = 80,000 The missing figure (?? above) needs to be 72,000 + 42,000 = 114,000 although that aggregate figure is, arguably, not intuitively obvious given the "competing" figure of 122,000 discussed above. The root of this complication is that the hours released from the first contract cancelled, whichever contract that is, will all be sold for 100 each. However, if both contracts are cancelled the last 400 hours released will only be sold for 80 each. The required' figure of 114,000 reconciles to the figure of 122,000 as 400 (100 - 80) = 8,000 reflecting the fact that each revenue forgone figure shown under Northfield and Southfield was calculated as though it were the only contract to be cancelled. Scheduling the 3 columns side by side in this instance has obscured the nature of the comparison being made. Notes on Questions 2 and 3 2. The point here is that a financial profit and loss account (whether budgeted or historic) aims to tell the story' of a period's transactions irrespective of when they occur: whereas the relevant figures for decision making depend crucially on the point in time at which the decision is to be taken. Thus sunk costs are irrelevant for decision making and the relevant figures are future cash flows that differ between alternatives. The timing of cash flows is significant in two ways. Firstly, the longer the projects take to complete, the more important is the time value of money (especially if they have differing time scales) and discounting may be appropriate. Secondly, whichever contract is chosen, the timing of cash flows must be considered as it affects the firm's overall cash budget. Note this Case Study was published in the Journal of Accounting Case Research; reference is 3. Collison, D.J. (1997) "JB Development and Construction Ltd", Journal of Accounting Case Research, Vol.4, No.1, pp.62-67 SCHOOL OF ACCOUNTING & FINANCE Advanced Management Accounting - Case Study on Relevant Costs JB DEVELOPMENT AND CONSTRUCTION (Suggested Solution) 1.(a) Relevant Cash Flows if the Firm goes ahead with: "Inflows" House Sales Sale of unused land Sale of stock Savings from use of stock Northfield 000 1050 170 20 20 1260 Southfield 000 1200 150 5 40 1395 . "Outflows" Landscaping Consultancy Cancellation Fee Material Labour (Note 1) Processing Hours (Note 2) Plant Hire 60 10 200 100 42 40 40 30 5 225 100 72 65 452 808 537 858 Difference in favour of Southfield = 50,000 Note 1: The labour cost could be excluded from the list of outflows without affecting the differential figure, but it is an outflow and therefore, arguably, it should be included. 400 x (20+60) = 32 400 x (20+60) = 32 100 x (20+80) = 10 42 400 x (20+80) = 40 72 Note 2: The value shown for each machine hour is based on "variable cost plus opportunity cost". Alternatively it may be more easily thought of as revenue foregone (80 or 100) since the variable cost of a machine hour is the same for external and internal use. A detailed discussion of alternative approaches to the analysis of the processing hours appears below. Discussion of Layout Note: The layout used above for the relevant cash flows has arguable advantages over alternative approaches. For example: the inflows from the sale of the land and the stock could be shown as outflows in terms of opportunity cost with the other figures as before: Northfield 000 1,050 Southfield 000 1.200 Sales Outflows as before Opp. Cost of Land Opp. Cost of Material Stock 5+40= 452 150 45 537 170 40 20+20= 647 403 747 453 Difference in favour of Southfield = 50,000. While this approach is completely acceptable in terms of answering question 1(a) which is concerned only with the differential costs and benefits of the two contracts it can make life very difficult in answering part (b) 1.(b) Using a relevant cash flow approach a third column can easily be added. Northfield Southfield Neither 000 000 000 Inflows House Sales 1,050 1,200 Sale of unused land 170 150 320 Sale of savings from stock 40 45 85 1.260 1,395 405 Outflows As before 452 537 Cancellation Fees for both 15 808 858 390 Thus Southfield leaves the firm 858,000-390,000 = 468,000 better off than it would have been if neither contract had been allowed. Thus Southfield leaves the firm 858,000-390,000 = 468,000 better off than it would have been if neither contract had been allowed. Note: The alternative 'explicit' opportunity cost approach to this question is, as discussed above, arguably more complicated and can more easily lead to confusion and errors of double counting or omission. As stated above the labour cost of 100,000 could be excluded from the solution to part (a) since it was to both contracts but it becomes relevant as soon as the third option of "neither contract" is considered: this is a good example of the definition of a relevant cost as "a future cash flow that differs between alternatives." Note that a further approach to question 1(a) which some students will attempt (and, usually, get wrong) starts with the Budgeted Profit figures, thus: common Northfield 000 395 Southfield 000 350 Deduct extra land cost 150-120 (30) 170-160 (10) Material: add sunk cost 10-5 5 80-20 60 Machine Processing: Deduct 42-25 (17) 72-40 (32) Consultancy 10-10 0 70-5 65 Fixed overheads 50 60 Landscaping (40) 453 403 Difference in favour of Southfield = 50,000 Attempts to answer question 1(b) as a development of this approach are likely to be confusing. The main lesson I try to drive home with this case is keep it simple and think as far as possible of cash flows - cheques received and cheques written. Of course the notion of opportunity costs is useful and sometimes necessary, e.g. in dealing with the revenue foregone by the use of the machine processing hours. (This assertion that opportunity costs are necessary to the analysis of the machine processing hours may be thought contentious: their treatment requires some care and the next section considers them in detail.) Approaches to Analysing the Effect of the Alternative Uses of Machine Hours The first point to emphasise is that in all scenarios being explored the available machine hours will be fully utilised; thus their variable cost of 20 per hour (which is common to all uses) is irrelevant. (An equivalent viewpoint, as stated above, is that the relevant cost of these hours can be characterised as "variable cost plus contribution".) My preferred approach is to regard the status quo as the situation that would exist if neither contact were to be done. Then the thinking can be entirely in terms of the opportunity cost of the hours used (i.e. the revenue foregone); and that is the thinking embodied in the above analysis. To think, simultaneously, of incremental revenue generated by the hours released by cancelling a contract, would mean double counting. However, such an approach can be used if the status quo is assumed to be a situation in which both contracts are to go ahead. Then the cancellation of a contract would indeed lead to the generation of incremental revenue vis--vis the status quo. Such an approach would lead to a modification of the format shown above in the first note for (a) as follows: Northfield 000 Southfield 000 1,395 1,260 Inflows as before Revenue from Sale of Machine Hours not required 400 x 100 = 32,000 400 x 80 = 40,000 400 x 100 = 10,000 400 x 80 = 32,000 _72 1,332 42 1,437 Outtflows as before less 452 42 410 922 537 72 465 972 Difference in favour of Southfield = 50,000 A development of this approach to deal with the problem posed in Question 1(b) leads to a problem of some subtlety as follows (the remainder of this discussion of the first question is perhaps just for real enthusiasts!): Northfield 000 Southfield 000 1,395 Neither 000 405 1,260 Inflows as before Revenue from sale of Machine hours not required 72 42 42 ?? 1,332 1,437 Outflows As before less 15 452 42 537 72 410 922 465 972 The number represented by ?? above is problematic and there is scope for confusion over the status quo against which this option is to be evaluated. If the figure is calculated from a status quo assumption that each contract goes ahead, then the hours released by not doing either contract will generate 900 x 100 = 90,000 400 x 80 = 32.000 122.000 This would give a bottom line to the 'neither' column of 512,000 and a difference of 460,000 compared to the value of Southfield. This figure is not the same as its equivalent which was originally calculated in 1(b) which was 858-390 = 468,000 (a difference of 8000). The correct figure given the terms of the question, is the first one (468,000). The flaw in using the figure of 122,000 is that the status quo against which the option of 'neither contract' is being evaluated is that of doing just one contract, not both. In terms of potential revenue earned from the outside sale of machine hours the complete set of possibilities is: Cancel both contracts... receive an inflow of 122,000 Cancel Northfield... receive an inflow of 500 hours x 100= 50,000 Cancel Southfield receive an inflow of 800 hours x 100 = 80,000 The missing figure (?? above) needs to be 72,000 + 42,000 = 114,000 although that aggregate figure is, arguably, not intuitively obvious given the "competing" figure of 122,000 discussed above. The root of this complication is that the hours released from the first contract cancelled, whichever contract that is, will all be sold for 100 each. However, if both contracts are cancelled the last 400 hours released will only be sold for 80 each. The required' figure of 114,000 reconciles to the figure of 122,000 as 400 (100 - 80) = 8,000 reflecting the fact that each revenue forgone figure shown under Northfield and Southfield was calculated as though it were the only contract to be cancelled. Scheduling the 3 columns side by side in this instance has obscured the nature of the comparison being made. Notes on Questions 2 and 3 2. The point here is that a financial profit and loss account (whether budgeted or historic) aims to tell the story' of a period's transactions irrespective of when they occur: whereas the relevant figures for decision making depend crucially on the point in time at which the decision is to be taken. Thus sunk costs are irrelevant for decision making and the relevant figures are future cash flows that differ between alternatives. The timing of cash flows is significant in two ways. Firstly, the longer the projects take to complete, the more important is the time value of money (especially if they have differing time scales) and discounting may be appropriate. Secondly, whichever contract is chosen, the timing of cash flows must be considered as it affects the firm's overall cash budget. Note this Case Study was published in the Journal of Accounting Case Research; reference is 3. Collison, D.J. (1997) "JB Development and Construction Ltd", Journal of Accounting Case Research, Vol.4, No.1, pp.62-67