Question: Instructions are highlighted Issues in Accounting Education Vol. 15, No. 2 May 2000 Budgeting and Performance Evaluation at the Berkshire Toy Company Dean Crawford and

Instructions are highlighted

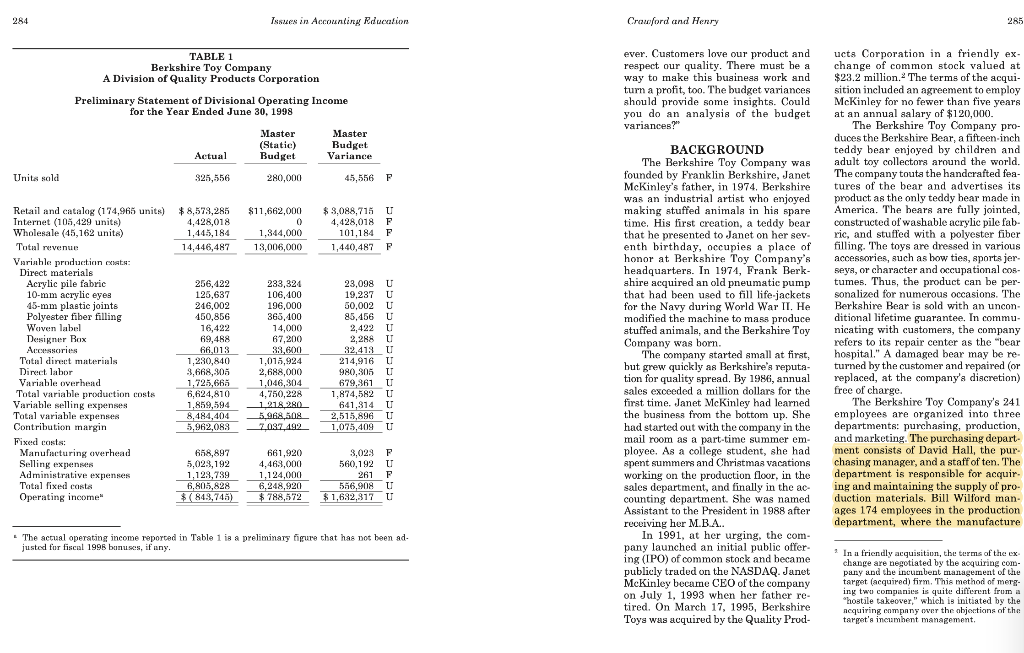

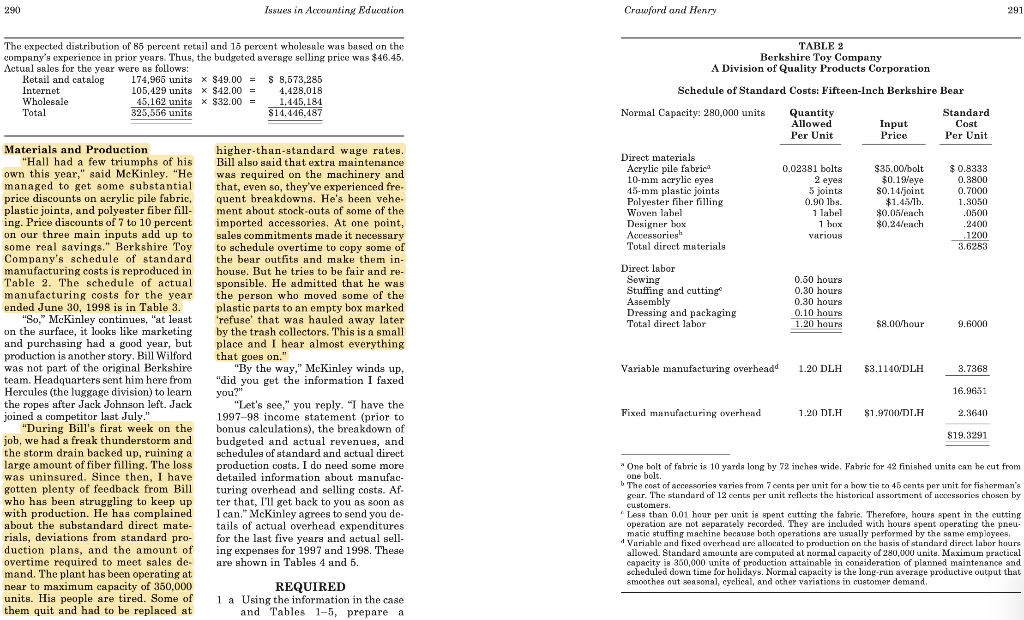

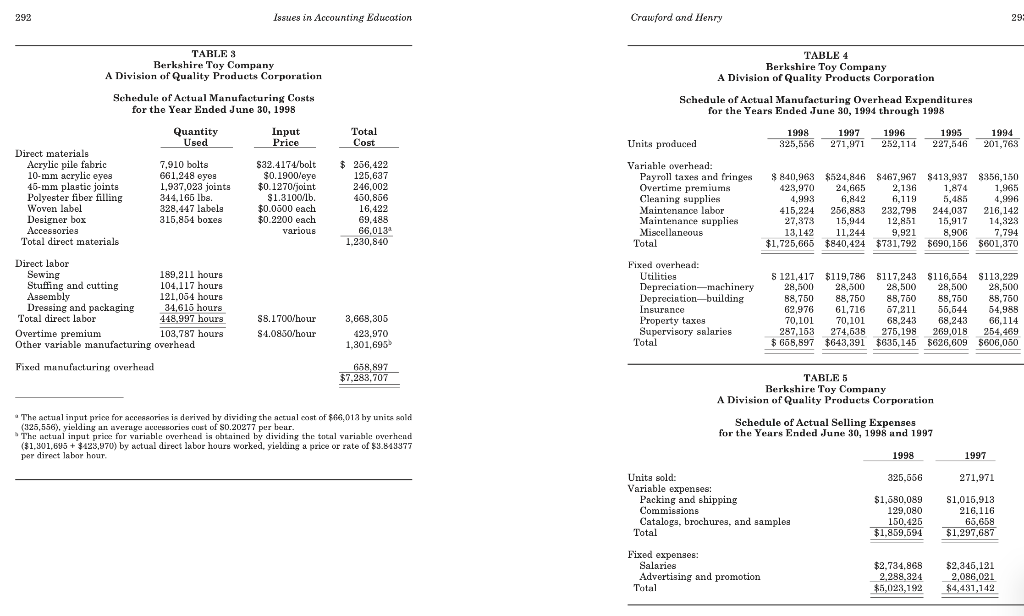

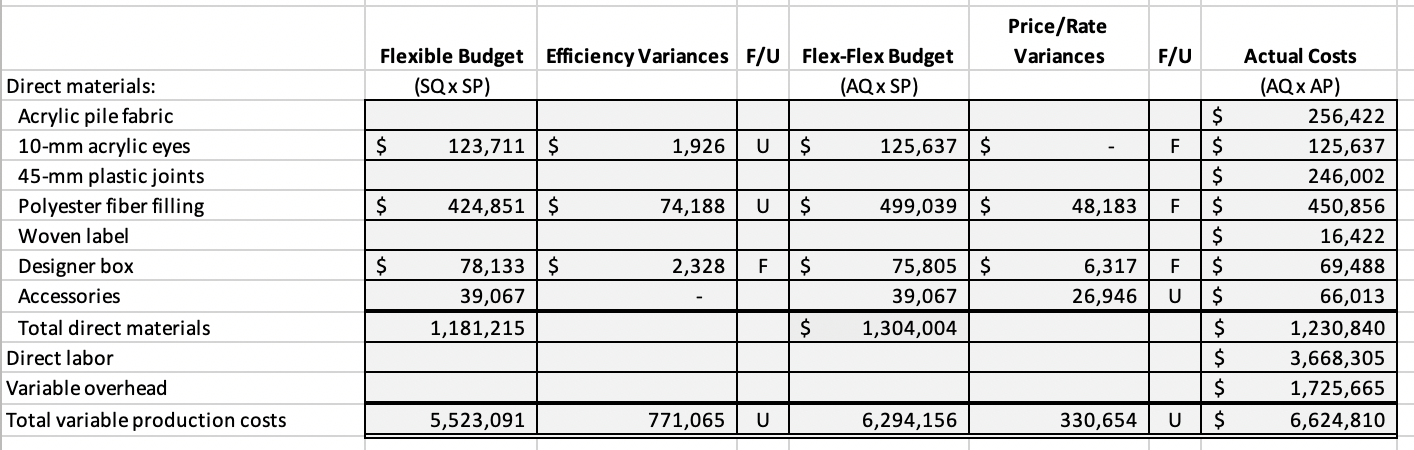

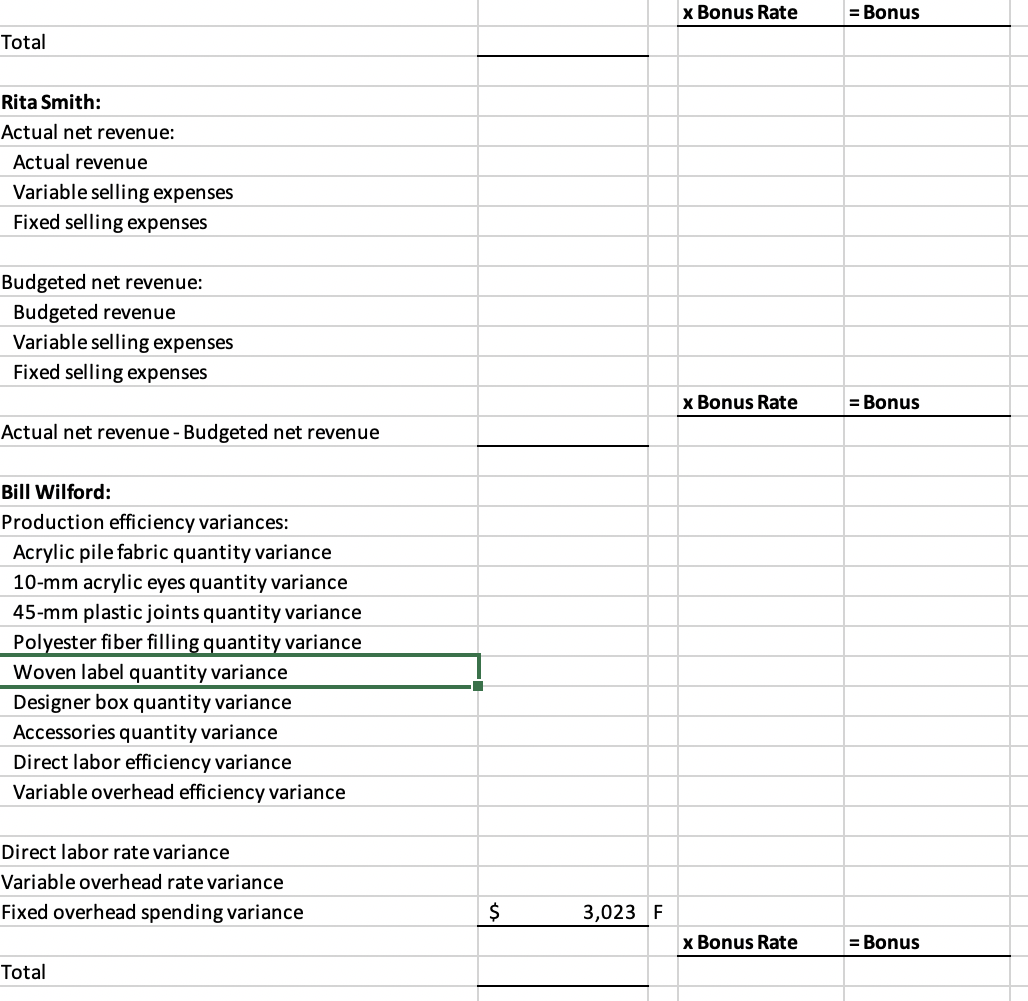

Issues in Accounting Education Vol. 15, No. 2 May 2000 Budgeting and Performance Evaluation at the Berkshire Toy Company Dean Crawford and Eleanor G. Henry ABSTRACT: This case provides an opportunity to study budgets, budget vari- ances, and performance evaluation at several levels. As a purely mechanical problem, the case asks for calculations of various price, efficiency, spending, and volume variances from a set of budgets and actual results. The case is also an interpretive exercise. After the variances have been computed, the next step is to develop plausible conjectures about their likely causes. Finally, it is a case about performance evaluation and responsibility accounting. The company has an incentive plan, based on the budget variances, that needs to be analyzed and critiqued. INTRODUCTION and now she has called you for advice. anet McKinley is employed by the "I know the bottom line looks pretty Quality Products Corporation, a bad," she says. But we made great strides this year. Sales are higher than The manufactures and sells many different kinds of products, 1 This case is based on field research at an ex. including music synthesizers, isting toy company. The essential facts relat- breakfast cereals, peanut butter, and ing to production and sales have been re- children's toys. McKinley is Vice Presi- tained. However, all names, dates, actual events, and identifying details have been con- dent in charge of the Berkshire Toy cealed to protect the privacy and identity of Company, a division of Quality the company. Thus, if any names used in this Products. case are those of actual firms or individuals, then it is purely coincidental. It is late July 1998 and McKinley has just received the preliminary in- come statement for her division for the Dean Crawford and Eleanor G. Henry year ended June 30, Table are both Associate Professors at SUNY 1). The master (static) budget and mas at Oswego. ter budget variances for the same pe- riod are included for comparison pur The valuable comments and suggestions on poses. McKinley looks at the bottom earlier versions of this case from Professors line, a loss approaching a a million dol. Jeffery Abarbanell, James Noel, Nicholas lars, then picks up the phone to call you. Schroeder, the editor, David E. Stout, and You are an accountant in the associate editor, Jeffrey Cohen, two anony- controller's office at the headquarters mous reviewers, and the students of the of Quality Products Graduate School of Business Administration You Corporation. at the University of Michigan and the Col- worked with McKinley when her com- lege of Business Administration at the Uni- pany was acquired by Quality Products, versity of Toledo are gratefully acknowledged. corporation luggage, 1998 (see 254 Issues in Accounting Education Crawford and Henry 285 TABLE 1 Berkshire Toy Company A Division of Quality Products Corporation ever. Customers love our product and respect our quality. There must be a way to make this business work and turn a profit, too. The budget variances should provide some insights. Could you do an analysis of the budget variances?" Preliminary Statement of Divisional Operating Income for the Year Ended June 30, 1998 Master Master (Static) Budget Actual Budget Variance Units sold 325,556 280,000 45,556 F $ 8,573,285 4,428,018 1,445,184 14,446,487 $11,662,000 0 1,344,000 13,006,000 $ 3.088,711 U 4,428,018 F 101,184 F 1,440,487 F Retail and catalog (174,965 units) Internet (105,429 units) Wholesale (45,162 unita) Total revenue Variable production costs Direct materials Acrylic pile fabric 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Waven label Designer Box Accessories Tatal direct materials Direct labor Variable overhead Total variable production costs Variable selling expenses Total variable expenses Contribution margin Fixed costs: : Manufacturing overhead Selling expenses Administrative expenses Tatal fixed costa Operating income 256,422 126,637 216,002 450,856 16,422 69,488 66,013 1,230,840 3,668,905 1.725,668 6,624,810 1,859,594 8,484,404 5,962,082 233,324 106,100 196,000 365,100 14,000 67,200 33,600 1,017,924 2,688,000 1,046,304 4,750,228 1 218,280 5.968,508 2087,492 23,098 U 19,237 U 50,002 U 85,156 U 2,422 U 2,288 U 32,413 U 214,916 U 980,305 U 679,361 U 1,474,582 U 641,314 U 2,515,896 1,075,409 U BACKGROUND The Berkshire Toy Company was founded by Franklin Berkshire, Janet McKinley's father, in 1974, Berkshire was an industrial artist who enjoyed making stuffed animals in his spare time. His first creation, a teddy bear that he presented to Janet on her sev- enth birthday, occupies a place of honor at Berkshire Toy Company's headquarters. In 1974, Frank Berk- ahire acquired an old pneumatic pump that had been used to fill life jackets for the Navy during World War II. He modified the machine to mass produce atuffed animals, and the Berkahire Toy Company was born. The company started small at first, but grew quickly as Berkshire's reputa- tion for quality spread. By 1986, annual sales exceeded a million dollars for the first time. Janet McKinley had learned the business from the bottom up. She had started out with the company in the mail room as a part-time summer em ployee. As a college student, she had spent summers and Christmas vacations working on the production floor, in the sales department, and finally in the ac counting department. She was named Assistant to the President in 1988 after receiving her M.BA In 1991, at her urging, the com- pany launched an initial public offer- ing (IPO) of common stock and became publicly traded on the NASDAQ. Janet McKinley became CEO of the company on July 1, 1993 when her father re- tired. On March 17, 1995, Berkshire Toys was acquired by the Quality Prod- ucta Corporation in a friendly ex- change of common stock valued at $23.2 million. The terms of the acqui- sition included an agreement to employ McKinley for no fewer than five years at an annual salary of $120,000 The Berkshire Toy Company pro- duces the Berkshire Bear, a fifteen-inch teddy bear enjoyed by children and adult toy collectors around the world. The company touta the handcrafted fea- tures of the bear and advertises its product as the only teddy bear made in America. The bears are fully jointed, constructed of washable acrylic pile fab- ric, and stuffed with a polyester fiber filling. The toys are dressed in various accessories, such as how ties, sports jer. seya, or character and occupational cos- tumes. Thus, the product can be per- sonalized for numerous occasions. The Berkshire Bear is sold with an uncon ditional lifetime guarantee. In commu- nicating with customers, the company refers to its repair center as the "bear hospital." A damaged bear may be re- turned by the customer and repaired (or replaced, at the company's discretion) free of charge. The Berkshire Toy Company's 241 employees are organized into three departments: purchasing, production, and marketing. The purchasing depart- ment consists of David Hall, the pur- chasing manager, and a staff of ten. The department is responsible for acquir. ing and maintaining the supply of pro- duction materials. Bill Wilford man- ages 174 employees in the production department, where the manufacture 658,897 5,029,192 1,123,739 6,805,828 $(849,745) 661,920 4,463,000 1,124,000 6,248,920 $ 788,572 F 560,192 U 261 F 556,908 U U $1,682,817 U The actual operating income reported in Table 1 is a preliminary figure that has not been ad- justed for fiscal 1995 bonuses, if any, ? In a friendly acquisition, the terms of the ex change are negotiated by the acquiring com- pany and the incumbent management of the target (acquired) firm. This method of merg- ing two companies is quite different from a "hostile takeover," which is initiated by the ncquiring company over the objections of the target's incumbent management. 288 Issues in Accounting Education Crawford and Henry 269 factory store, have been closed in pre- vious years. adjacent to the factory. Retail Internet sales are a new addition to the overall marketing effort. The company also sells wholesale to de. partment stores, toy boutiques, and other specialty retailers. The product can be delivered by two-to-five-day ground service, next-day air, or holi- day express. The customer pays the insurance and delivery charges. Berkshire promises same or next day shipment. Most orders are shipped the same day as received When the company receives a customer's order, an employee takes a bear of the requested color and dresses it according to the customer's wishes. Then the bour is packaged with a pro- tective air bag and complimentary piece of chocolate candy, and shipped in a designer box. The designer box contributes to the product image. It is reminiscent of the packaging used for a famoua-name cologne and intended to lend an air of status and exclusivity to the product. The box is also impor- tant to toy collectors who expect to pay or receive a price premium in the sec. ondary market for items that are in "mint-in-box"condition, Producing the box is a custom job involving a box manufacturer and a printing company. The unit cost of the box decreases with the size of the order that the company places with the manufacturer. Rush orders are more costly than normal orders. In July 1997, the purchasing manager placed an order for enough boxes to cover budgeted sales in the coming year. Berkshire's policy on sales commis. siona has remained stable over the past several years. Commissions of 3 percent are paid on retail store sales and sales to wholesale buyers. No commissione are puid on catalog sales. The company. owned retail outlets have proved un- profitable, so all of them, except for the The Accounting Problem "I think I know what some of the problems are, but I would like a de- tailed analysis that provides confirma- tion from our accounting data, McKinley continues. "Did inventory change much?" you ask "It's pretty negligible. Our peak sell- ing time is from Christmas to Mother's Day, so we don't have much on hand at the June 30 year-end. We started last year with almost nothing and it was all we could do to keep up with demand, ao we ended up with almost nothing as well." You jot down a note to ignore changes in raw materials and finished goods inventories and to assume that production volume equals sales volume. "Didn't you put a new incentive compensation plan in place this year?" "Aa a matter of fact, we did. Per- hapa it was a factor in what happened this year." The new incentive compensation plan was adopted effective July 1, 1997. Under this plan, each of the three de. partment heads is rewarded based on the performance of his or her responsi. bility center. Performance is measured against the company'a master budget and its standard coat wystum. The plan was the result of aeveral meetings with McKinley and hur managers who ar- gued and bargained for a plan that re- warded the managers fairly for indi. vidual contributions and achievements. McKinley's plan was intended to pro mote participation and teamwork and the managers accepted the new pro- gram enthusiastically. The plan pro- vides for the following: David Hall, the purchasing man- ager, will receive a bonus equal to 20 percent of the net materials price variance, assuming the net and an opportunity for customers to variance is favorable. Otherwise, order online. As an additional incen- the bonus is zero. tive to attract Internet customers, Rita Rita Smith, the marketing man. Smith proposed that Berkshire offer a ager, will receive a bonus equal to substantial discount to customers who 10 percent of the excess, if any, of ordered over the Internet. Because the actual net revenues (revenues mi discounted Internet price ($42.00) was nua both variable and fixed selling still greater than the price that Berk- expenses) over master budget net shire was charging its wholesale cus- revenues. tomers ($32.00), McKinley approved Bill Wilford, the production man the price change. ager, will receive a bonus equal to To boost its Internet sales, the com 3 percent of the net of several vari pany held special holiday sales. The ancea: the efficiency (usage or Christmas and Valentine's Day sales quantity) variances for materials, featured the Berkshire Bear in special labor, and variable overhead; the seasonal costumes. Both events were labor rate variance; and the vari. immediate auccesses not only with able and fixed overhead spending Internet customers, but also with re- variances. Wilford receives no bo. tail and wholesale customers who paid nus if his net variance is the customary prices. The greatest suc- unfavorable. cess was the Mother's Day campaign. For this event, the web site displayed Internet Sales Program an image of "Mama's Boy," a bear "It seems that the incentive plan sporting sunglasses, jeans and T-shirt, produced results,"continuea McKinley. and an appliqud tattoo on its upper "Smith had a terrific year this year. arm that said "Mom." Unit sales were more than 16 percent The 15-inch bears produced by above budget (Table 1). She says one the Berkshire Toy Company are iden- of the principal factors was the new tical except for their color and their Internet sales policy she instituted and accessories. Although the bears may the advertising campaign to support it. be purchased with differing accesso We've never had that kind of year in ries, the unit cost of the accessories salen before." per bear has been relatively stable The Berkshire Toy Company began over time. The average historical cost selling over the Internet in November of accessories hus buon a very small 1997. At the same time, the company part of the total cost of the bear, and launched a nationwide radio advertis the standard cost of accessories is ing campaign. All radio advertise. computed as an average. The price ments are tagged with a reference to differences in the product reflect the the web site that, in turn, provides vi company's discounting practices and sual support for the radio advertising not differences in accessories The master (static) budget for the year ended June 30, 1998 was prepared before the Internet program and price change were adopted. It called for the sale of 280,000 units, allocated as follows: Retail and mail order 238,000 units x $49.00 = Wholesale 42,000 units X $32.00 = Total 280,000 units $11,662,000 1,344,000 $13,006,000 290 Issues in Accounting Education Crawford and Henry 291 The expected distribution of 85 percent retail and 15 percent wholesale was based on the company's experience in prior years. Thus, the budgeted average selling price was $46.45. Actual sales for the year were as follows: Retail and catalog 174,965 units * $49.00 = S 8,573,285 Internet 105,429 units X $42.00 = 4.428,018 Wholesale 45,162 units X $32.00 = 1.445,184 Total 325,556 units $14,146,187 TABLE 2 Berkshire Toy Company A Division of Quality Products Corporation Schedule of Standard Costs: Fifteen-Inch Berkshire Bear Normal Capacity: 280,000 units Quantity Allowed Per Unit Input Price Standard Cost Per Unit Direct materials Acrylic pile fabrica 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Woven label Designer box Accessories Total direct materials 0.02381 bolts 2 eyes 5 joints 0.90 lbs. 1 label i box various $35.00/bolt $0.19/eye SO.14hjoint $1.45/1b. $0.05/each $0.24/each $ 0.8333 0.3800 0.7000 1.8050 .0500 .2400 .1200 3.6283 higher-than-standard wage rates. Bill also said that extra maintenance was required on the machinery and that, even so, they've experienced fre- quent breakdowns. He's been vehe. ment about stock-outs of some of the imported accessories. At one point, sales commitments made it necessary to schedule overtime to copy some of the bear outfits and make them in- house. But he tries to be fair and re- sponsible. He admitted that he was the person who moved some of the plastic parts to an empty box marked refuse that was hauled away later by the trash collectors. This is a small place and I hear almost everything that goes on." "By the way," McKinley winds up, "did you get the information I faxed Direct labor Sewing Stufting and cutting Assembly Dressing and packaging Total direct labor 0.50 hours 0.30 hours 0.30 hours 0.10 hours 1.20 hours $8.00hour 9.6000 Variable manufacturing overheadd 1.20 DLH $3.1140/DLH Materials and Production "Hall had a few triumphs of his own this year," said McKinley. "He managed to get some substantial price discounts on acrylic pile fabric, plastic joints, and polyester fiber fill- ing. Price discounts of 7 to 10 percent on our three main inputs add up to some real savings." Berkshire Toy Company's schedule of standard manufacturing costs is reproduced in Table 2. The schedule of actual manufacturing costs for the year ended June 30, 1998 is in Table 3. "So," McKinley continues, "at least on the surface, it looks like marketing and purchasing had a good year, but production is another story, Bill Wilford was not part of the original Berkshire team. Headquarters sent him here from Hercules (the luggage division) to learn the ropes after Jack Johnson left. Jack joined a competitor last July." "During Bill's first week on the job, we had a freak thunderstorm and the storm drain backed up, ruining a large amount of fiber filling. The loss was uninsured. Since then, I have gotten plenty of feedback from Bill who has been struggling to keep up with production. He has complained about the substandard direct mate- rials, deviations from standard pro- duction plans, and the amount of overtime required to meet sales de- mand. The plant has been operating at near to maximum capacity of 350.000 units. His people are tired. Some of them quit and had to be replaced at 3.7368 you? 16.9651 Fixed manufacturing overhead 1.20 DLH 81.9700/DLH 2.3640 $19.3291 "Let's see," you reply. "I have the 1997-98 income statement (prior to bonus calculations), the breakdown of budgeted and actual revenues, and schedules of standard and actual direct production costs. I do need some more detailed information about manufac- turing overhead and selling costs. Af ter that, I'll get back to you as soon as I can." McKinley agrees to send you de tails of actual overhead expenditures for the last five years and actual sell- ing expenses for 1997 and 1998. These are shown in Tables 4 and 5. * One bolt of fabric is 10 yarda long hy 72 inches wide. Fabric for 42 finished units can be cut from one bolt. The cost of accessories varies from 7 centa per unit for a how tie tn 45 cents per unit for fisherman's gear. The stundard of 12 cents per unit reflects the historical assortment of excesories chosen by customers. Less than 0.01 hour per unit is spent cutting the fabric. Therefore, hours spent in the cutting operation are not separately recorded. They are included with hours spent operating the pneu- matic stuffing machine because both operations are usually performed by the same employees. "Variable and fixed averhead are allocated to production on the basis of standard direct labor hours allowed. Standard amounts are computed at normal capacity of 280,000 units. Maximum practical capacity is 360,000 units of production attainable in consideration of planned maintenance and scheduled down time for holidays. Normal capacity is the long-run average productive output that smoothes out Beasonal, cyclical, and other variations in customer demand. REQUIRED 1 a Using the information in the case and Tables 1-5, prepare a 292 Issues in Accounting Education Crawford and Ilenty 29 TABLE 3 Berkshire Toy Company A Division of Quality Products Corporation Schedule of Actual Manufacturing Costs for the Year Ended June 30, 1998 Quantity Used Input Price Total Cost Direct materials Acrylic pile fabric 10-mom acrylic eyes 46-mm plastic joints Polyester fiber filling Woven label Designer box Accessories Total direct materials 7,910 bolts 661,248 eyes 1,937,023 joints 344,166 lbs. 328,447 labels 315.854 boxes $32.4174/bolt $0.1900/eye $0.1270/joint $1.3100/1b. $0.0500 each $0.2200 each various $ 256,422 125,637 246,002 450,856 16.422 69,488 66,013 1.230,840 TABLE 4 Berkshire Toy Company A Division of Quality Products Corporation Schedule of Actual Manufacturing Overhead Expenditures for the Years Ended June 30, 1994 through 1998 1998 1997 1996 1995 1994 Units produced 825,556 271,971 252,114 227,546 201,763 Variable overhead: Payroll taxes and fringes $840.963 $524,846 S467,967 $413,937 8356,150 Overtime premiums 423,970 24,665 2,136 1,874 1,965 Cleaning supplies 4,993 6,842 6,119 5,485 4,996 Maintenance labor 415,224 256,883 232,798 244,037 216.142 Maintenance supplies 27,379 15,944 12,851 15,917 14,323 Miscellaneous 13,142 11,244 9,921 8,906 7,794 Total $1,725,665 $840,424 $731,792 $690.156 $601,370 $ Fixed overhead: Utilities S 121,417 $119,786 $117,243 $116,554 $113,229 Depreciation-machinery 28,500 28,500 28,500 28,500 28,500 Depreciation building 88.750 88,750 88,750 88,750 88,750 Insurance 62,976 61,716 57,211 56,544 54,988 Property taxes 70.101 70.101 68,243 68,243 66,114 Supervisory salarios 287,163 274,638 275,198 269,018 254,469 Total $ 668,897 $643,391 $635,145 $626,609 $606,050 Direct labor Sewing 189.211 hours Stuffing and cutting 104,117 hours Assembly 121.054 hours Dressing and packaging 34,610 hours Total direct labor 448,997 hours Overtime premium 103,787 hours Other variable manufacturing overhead S8.1700/hour $4.0850/hour 3.668,805 423,970 1,301,695 Fixed manufacturing overhead 658,897 $7,283,707 TABLE 5 Berkshire Toy Company A Division of Quality Products Corporation The actual input price for accessories is derived by dividing the actual cost of $66,012 by units sold (325,556), yielding an average accessories cuest of S0.20277 per beur. The actual input price for variable overhead is obtained by dividing the total variable overhend ($1,901,695 + $423,970) by actual direct labor houre worked, yielding a price or rate of $8.813377 per direct labor hour Schedule of Actual Selling Expenses for the Years Ended June 30, 1998 and 1997 1998 1997 325.556 271,971 Units sold: Variable expenses: Packing and shipping Commissions Catalogs, brochures, and samples Total $1,680,089 129,080 150.425 $1.859.694 $ S1,015,913 216.116 65,658 $1,297,687 Fixed expenses: Salaries Advertising and promotion Total $2.734,868 2,288.324 $5,023,192 $2,345,121 2,086,021 $4,431,142 294 Issues in Accounting Education 3. flexible budget for the Berkshire Toy Company for the year ended June 30, 1998. Analyze the company's total master (static) budget variance for the year. Compare the flexible and master (static) budgets and prepare a schedule showing the sales vol- ume variance. C Compare the ac- tual results and the flexible bud- get, and prepare a schedule showing the flexible budget vari- ance. Subdivide the flexible bud- get variances into the appropriate price (rate or spending) and effi- ciency (usage or quantity) vari- ances for materials, labor, and variable overhead. modifications to the incentive plan would you recommend? Why? (Optional) Suppose that Berk- shire Toy Company adopts a balanced scorecard (BSC) to mea- sure its performance. What per- formance dimensions are typi- cally included in a BSC? What specific performance measures (indicators) might be included in the scorecard? For useful baske ground information on BSCs, see Forsythe et al. (1999, 1318). b. Compute the bonuses earned in fiscal 1998, if any, by David Hall of the purchasing department, Rita Smith of the marketing de- partment, and Bill Wilford of the production department. 2. a. You will be assisting in the inves- tigation of certain variances. Us- ing the information provided, for- mulate some likely explanations for the observed variances. b. Comment on the advantages and disadvantages of the incentive compensation plan as it applies to department heads. What is the appropriate role of the budget in performance evaluation? What 8 For the sales revenue categories shown in Table 1, prepare a flexible budget based on actual units sold multiplied by the master (static) budget prices. For Internet sales, use a "revised" budget price of $42. To analyze sales volume effects, also prepare a second flexible budget for the sales revenue catego- ries based on the total of 325,556 units sold, multiplied by the budgeted mix (85 percent for retail, 0 percent for Internet, and 15 percent for wholesale). Multiply these quantities by the respective budgeted sales prices. The dif- ference between the two flexible budget amounts is generally termed a sales mix vari- ance," which quantifies the effect on income that results because the actual mix of distri- bution channels deviates from the budgeted mix. A comparison between the master (static) budget and the flexible budget prepared on the basis of the budgeted mix is the sales volume variance." This variance measures the effect on operating income of selling more or fewer units than planned. The net of the sales mix variance and the sales volume variance equals the sales activity variance." Price/Rate Variances F/U Flexible Budget Efficiency Variances F/U Flex-Flex Budget (SQxSP) (AQ x SP) $ 123,711 $ 1,926 U $ 125,637 $ F $ 424,851 $ 74,188 U $ 499,039 $ 48,183 F Direct materials: Acrylic pile fabric 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Woven label Designer box Accessories Total direct materials Direct labor Variable overhead Total variable production costs Actual Costs (AQ x AP) 256,422 125,637 246,002 450,856 16,422 69,488 66,013 1,230,840 3,668,305 1,725,665 6,624,810 $ 2,328 F $ F 78,133 $ 39,067 1,181,215 75,805 $ 39,067 1,304,004 $ $ $ $ $ $ $ $ $ $ $ 6,317 26,946 U $ 5,523,091 771,065 U 6,294,156 330,654 U x Bonus Rate = Bonus Total Rita Smith: Actual net revenue: Actual revenue Variable selling expenses Fixed selling expenses Budgeted net revenue: Budgeted revenue Variable selling expenses Fixed selling expenses x Bonus Rate = Bonus Actual net revenue - Budgeted net revenue Bill Wilford: Production efficiency variances: Acrylic pile fabric quantity variance 10-mm acrylic eyes quantity variance 45-mm plastic joints quantity variance Polyester fiber filling quantity variance Woven label quantity variance Designer box quantity variance Accessories quantity variance Direct labor efficiency variance Variable overhead efficiency variance Direct labor rate variance Variable overhead rate variance Fixed overhead spending variance $ 3,023 F x Bonus Rate = Bonus Total 1. Based on the information provided in the case, provide likely explanations for at least one direct materials quantity variance, one direct materials price variance, the direct labor efficiency variance, and the direct labor rate variance. (Note: These explanations should be based on specific information provided in the case, not "the direct labor efficiency variance is unfavorable becaue the actual labor hours were more than the standard labor hours allowed.") 2. Comment on the advantages and disadvantages of the incentive compensation plan as it applies to department heads. 3. What changes to the incentive plan would you recommend? Why? Issues in Accounting Education Vol. 15, No. 2 May 2000 Budgeting and Performance Evaluation at the Berkshire Toy Company Dean Crawford and Eleanor G. Henry ABSTRACT: This case provides an opportunity to study budgets, budget vari- ances, and performance evaluation at several levels. As a purely mechanical problem, the case asks for calculations of various price, efficiency, spending, and volume variances from a set of budgets and actual results. The case is also an interpretive exercise. After the variances have been computed, the next step is to develop plausible conjectures about their likely causes. Finally, it is a case about performance evaluation and responsibility accounting. The company has an incentive plan, based on the budget variances, that needs to be analyzed and critiqued. INTRODUCTION and now she has called you for advice. anet McKinley is employed by the "I know the bottom line looks pretty Quality Products Corporation, a bad," she says. But we made great strides this year. Sales are higher than The manufactures and sells many different kinds of products, 1 This case is based on field research at an ex. including music synthesizers, isting toy company. The essential facts relat- breakfast cereals, peanut butter, and ing to production and sales have been re- children's toys. McKinley is Vice Presi- tained. However, all names, dates, actual events, and identifying details have been con- dent in charge of the Berkshire Toy cealed to protect the privacy and identity of Company, a division of Quality the company. Thus, if any names used in this Products. case are those of actual firms or individuals, then it is purely coincidental. It is late July 1998 and McKinley has just received the preliminary in- come statement for her division for the Dean Crawford and Eleanor G. Henry year ended June 30, Table are both Associate Professors at SUNY 1). The master (static) budget and mas at Oswego. ter budget variances for the same pe- riod are included for comparison pur The valuable comments and suggestions on poses. McKinley looks at the bottom earlier versions of this case from Professors line, a loss approaching a a million dol. Jeffery Abarbanell, James Noel, Nicholas lars, then picks up the phone to call you. Schroeder, the editor, David E. Stout, and You are an accountant in the associate editor, Jeffrey Cohen, two anony- controller's office at the headquarters mous reviewers, and the students of the of Quality Products Graduate School of Business Administration You Corporation. at the University of Michigan and the Col- worked with McKinley when her com- lege of Business Administration at the Uni- pany was acquired by Quality Products, versity of Toledo are gratefully acknowledged. corporation luggage, 1998 (see 254 Issues in Accounting Education Crawford and Henry 285 TABLE 1 Berkshire Toy Company A Division of Quality Products Corporation ever. Customers love our product and respect our quality. There must be a way to make this business work and turn a profit, too. The budget variances should provide some insights. Could you do an analysis of the budget variances?" Preliminary Statement of Divisional Operating Income for the Year Ended June 30, 1998 Master Master (Static) Budget Actual Budget Variance Units sold 325,556 280,000 45,556 F $ 8,573,285 4,428,018 1,445,184 14,446,487 $11,662,000 0 1,344,000 13,006,000 $ 3.088,711 U 4,428,018 F 101,184 F 1,440,487 F Retail and catalog (174,965 units) Internet (105,429 units) Wholesale (45,162 unita) Total revenue Variable production costs Direct materials Acrylic pile fabric 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Waven label Designer Box Accessories Tatal direct materials Direct labor Variable overhead Total variable production costs Variable selling expenses Total variable expenses Contribution margin Fixed costs: : Manufacturing overhead Selling expenses Administrative expenses Tatal fixed costa Operating income 256,422 126,637 216,002 450,856 16,422 69,488 66,013 1,230,840 3,668,905 1.725,668 6,624,810 1,859,594 8,484,404 5,962,082 233,324 106,100 196,000 365,100 14,000 67,200 33,600 1,017,924 2,688,000 1,046,304 4,750,228 1 218,280 5.968,508 2087,492 23,098 U 19,237 U 50,002 U 85,156 U 2,422 U 2,288 U 32,413 U 214,916 U 980,305 U 679,361 U 1,474,582 U 641,314 U 2,515,896 1,075,409 U BACKGROUND The Berkshire Toy Company was founded by Franklin Berkshire, Janet McKinley's father, in 1974, Berkshire was an industrial artist who enjoyed making stuffed animals in his spare time. His first creation, a teddy bear that he presented to Janet on her sev- enth birthday, occupies a place of honor at Berkshire Toy Company's headquarters. In 1974, Frank Berk- ahire acquired an old pneumatic pump that had been used to fill life jackets for the Navy during World War II. He modified the machine to mass produce atuffed animals, and the Berkahire Toy Company was born. The company started small at first, but grew quickly as Berkshire's reputa- tion for quality spread. By 1986, annual sales exceeded a million dollars for the first time. Janet McKinley had learned the business from the bottom up. She had started out with the company in the mail room as a part-time summer em ployee. As a college student, she had spent summers and Christmas vacations working on the production floor, in the sales department, and finally in the ac counting department. She was named Assistant to the President in 1988 after receiving her M.BA In 1991, at her urging, the com- pany launched an initial public offer- ing (IPO) of common stock and became publicly traded on the NASDAQ. Janet McKinley became CEO of the company on July 1, 1993 when her father re- tired. On March 17, 1995, Berkshire Toys was acquired by the Quality Prod- ucta Corporation in a friendly ex- change of common stock valued at $23.2 million. The terms of the acqui- sition included an agreement to employ McKinley for no fewer than five years at an annual salary of $120,000 The Berkshire Toy Company pro- duces the Berkshire Bear, a fifteen-inch teddy bear enjoyed by children and adult toy collectors around the world. The company touta the handcrafted fea- tures of the bear and advertises its product as the only teddy bear made in America. The bears are fully jointed, constructed of washable acrylic pile fab- ric, and stuffed with a polyester fiber filling. The toys are dressed in various accessories, such as how ties, sports jer. seya, or character and occupational cos- tumes. Thus, the product can be per- sonalized for numerous occasions. The Berkshire Bear is sold with an uncon ditional lifetime guarantee. In commu- nicating with customers, the company refers to its repair center as the "bear hospital." A damaged bear may be re- turned by the customer and repaired (or replaced, at the company's discretion) free of charge. The Berkshire Toy Company's 241 employees are organized into three departments: purchasing, production, and marketing. The purchasing depart- ment consists of David Hall, the pur- chasing manager, and a staff of ten. The department is responsible for acquir. ing and maintaining the supply of pro- duction materials. Bill Wilford man- ages 174 employees in the production department, where the manufacture 658,897 5,029,192 1,123,739 6,805,828 $(849,745) 661,920 4,463,000 1,124,000 6,248,920 $ 788,572 F 560,192 U 261 F 556,908 U U $1,682,817 U The actual operating income reported in Table 1 is a preliminary figure that has not been ad- justed for fiscal 1995 bonuses, if any, ? In a friendly acquisition, the terms of the ex change are negotiated by the acquiring com- pany and the incumbent management of the target (acquired) firm. This method of merg- ing two companies is quite different from a "hostile takeover," which is initiated by the ncquiring company over the objections of the target's incumbent management. 288 Issues in Accounting Education Crawford and Henry 269 factory store, have been closed in pre- vious years. adjacent to the factory. Retail Internet sales are a new addition to the overall marketing effort. The company also sells wholesale to de. partment stores, toy boutiques, and other specialty retailers. The product can be delivered by two-to-five-day ground service, next-day air, or holi- day express. The customer pays the insurance and delivery charges. Berkshire promises same or next day shipment. Most orders are shipped the same day as received When the company receives a customer's order, an employee takes a bear of the requested color and dresses it according to the customer's wishes. Then the bour is packaged with a pro- tective air bag and complimentary piece of chocolate candy, and shipped in a designer box. The designer box contributes to the product image. It is reminiscent of the packaging used for a famoua-name cologne and intended to lend an air of status and exclusivity to the product. The box is also impor- tant to toy collectors who expect to pay or receive a price premium in the sec. ondary market for items that are in "mint-in-box"condition, Producing the box is a custom job involving a box manufacturer and a printing company. The unit cost of the box decreases with the size of the order that the company places with the manufacturer. Rush orders are more costly than normal orders. In July 1997, the purchasing manager placed an order for enough boxes to cover budgeted sales in the coming year. Berkshire's policy on sales commis. siona has remained stable over the past several years. Commissions of 3 percent are paid on retail store sales and sales to wholesale buyers. No commissione are puid on catalog sales. The company. owned retail outlets have proved un- profitable, so all of them, except for the The Accounting Problem "I think I know what some of the problems are, but I would like a de- tailed analysis that provides confirma- tion from our accounting data, McKinley continues. "Did inventory change much?" you ask "It's pretty negligible. Our peak sell- ing time is from Christmas to Mother's Day, so we don't have much on hand at the June 30 year-end. We started last year with almost nothing and it was all we could do to keep up with demand, ao we ended up with almost nothing as well." You jot down a note to ignore changes in raw materials and finished goods inventories and to assume that production volume equals sales volume. "Didn't you put a new incentive compensation plan in place this year?" "Aa a matter of fact, we did. Per- hapa it was a factor in what happened this year." The new incentive compensation plan was adopted effective July 1, 1997. Under this plan, each of the three de. partment heads is rewarded based on the performance of his or her responsi. bility center. Performance is measured against the company'a master budget and its standard coat wystum. The plan was the result of aeveral meetings with McKinley and hur managers who ar- gued and bargained for a plan that re- warded the managers fairly for indi. vidual contributions and achievements. McKinley's plan was intended to pro mote participation and teamwork and the managers accepted the new pro- gram enthusiastically. The plan pro- vides for the following: David Hall, the purchasing man- ager, will receive a bonus equal to 20 percent of the net materials price variance, assuming the net and an opportunity for customers to variance is favorable. Otherwise, order online. As an additional incen- the bonus is zero. tive to attract Internet customers, Rita Rita Smith, the marketing man. Smith proposed that Berkshire offer a ager, will receive a bonus equal to substantial discount to customers who 10 percent of the excess, if any, of ordered over the Internet. Because the actual net revenues (revenues mi discounted Internet price ($42.00) was nua both variable and fixed selling still greater than the price that Berk- expenses) over master budget net shire was charging its wholesale cus- revenues. tomers ($32.00), McKinley approved Bill Wilford, the production man the price change. ager, will receive a bonus equal to To boost its Internet sales, the com 3 percent of the net of several vari pany held special holiday sales. The ancea: the efficiency (usage or Christmas and Valentine's Day sales quantity) variances for materials, featured the Berkshire Bear in special labor, and variable overhead; the seasonal costumes. Both events were labor rate variance; and the vari. immediate auccesses not only with able and fixed overhead spending Internet customers, but also with re- variances. Wilford receives no bo. tail and wholesale customers who paid nus if his net variance is the customary prices. The greatest suc- unfavorable. cess was the Mother's Day campaign. For this event, the web site displayed Internet Sales Program an image of "Mama's Boy," a bear "It seems that the incentive plan sporting sunglasses, jeans and T-shirt, produced results,"continuea McKinley. and an appliqud tattoo on its upper "Smith had a terrific year this year. arm that said "Mom." Unit sales were more than 16 percent The 15-inch bears produced by above budget (Table 1). She says one the Berkshire Toy Company are iden- of the principal factors was the new tical except for their color and their Internet sales policy she instituted and accessories. Although the bears may the advertising campaign to support it. be purchased with differing accesso We've never had that kind of year in ries, the unit cost of the accessories salen before." per bear has been relatively stable The Berkshire Toy Company began over time. The average historical cost selling over the Internet in November of accessories hus buon a very small 1997. At the same time, the company part of the total cost of the bear, and launched a nationwide radio advertis the standard cost of accessories is ing campaign. All radio advertise. computed as an average. The price ments are tagged with a reference to differences in the product reflect the the web site that, in turn, provides vi company's discounting practices and sual support for the radio advertising not differences in accessories The master (static) budget for the year ended June 30, 1998 was prepared before the Internet program and price change were adopted. It called for the sale of 280,000 units, allocated as follows: Retail and mail order 238,000 units x $49.00 = Wholesale 42,000 units X $32.00 = Total 280,000 units $11,662,000 1,344,000 $13,006,000 290 Issues in Accounting Education Crawford and Henry 291 The expected distribution of 85 percent retail and 15 percent wholesale was based on the company's experience in prior years. Thus, the budgeted average selling price was $46.45. Actual sales for the year were as follows: Retail and catalog 174,965 units * $49.00 = S 8,573,285 Internet 105,429 units X $42.00 = 4.428,018 Wholesale 45,162 units X $32.00 = 1.445,184 Total 325,556 units $14,146,187 TABLE 2 Berkshire Toy Company A Division of Quality Products Corporation Schedule of Standard Costs: Fifteen-Inch Berkshire Bear Normal Capacity: 280,000 units Quantity Allowed Per Unit Input Price Standard Cost Per Unit Direct materials Acrylic pile fabrica 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Woven label Designer box Accessories Total direct materials 0.02381 bolts 2 eyes 5 joints 0.90 lbs. 1 label i box various $35.00/bolt $0.19/eye SO.14hjoint $1.45/1b. $0.05/each $0.24/each $ 0.8333 0.3800 0.7000 1.8050 .0500 .2400 .1200 3.6283 higher-than-standard wage rates. Bill also said that extra maintenance was required on the machinery and that, even so, they've experienced fre- quent breakdowns. He's been vehe. ment about stock-outs of some of the imported accessories. At one point, sales commitments made it necessary to schedule overtime to copy some of the bear outfits and make them in- house. But he tries to be fair and re- sponsible. He admitted that he was the person who moved some of the plastic parts to an empty box marked refuse that was hauled away later by the trash collectors. This is a small place and I hear almost everything that goes on." "By the way," McKinley winds up, "did you get the information I faxed Direct labor Sewing Stufting and cutting Assembly Dressing and packaging Total direct labor 0.50 hours 0.30 hours 0.30 hours 0.10 hours 1.20 hours $8.00hour 9.6000 Variable manufacturing overheadd 1.20 DLH $3.1140/DLH Materials and Production "Hall had a few triumphs of his own this year," said McKinley. "He managed to get some substantial price discounts on acrylic pile fabric, plastic joints, and polyester fiber fill- ing. Price discounts of 7 to 10 percent on our three main inputs add up to some real savings." Berkshire Toy Company's schedule of standard manufacturing costs is reproduced in Table 2. The schedule of actual manufacturing costs for the year ended June 30, 1998 is in Table 3. "So," McKinley continues, "at least on the surface, it looks like marketing and purchasing had a good year, but production is another story, Bill Wilford was not part of the original Berkshire team. Headquarters sent him here from Hercules (the luggage division) to learn the ropes after Jack Johnson left. Jack joined a competitor last July." "During Bill's first week on the job, we had a freak thunderstorm and the storm drain backed up, ruining a large amount of fiber filling. The loss was uninsured. Since then, I have gotten plenty of feedback from Bill who has been struggling to keep up with production. He has complained about the substandard direct mate- rials, deviations from standard pro- duction plans, and the amount of overtime required to meet sales de- mand. The plant has been operating at near to maximum capacity of 350.000 units. His people are tired. Some of them quit and had to be replaced at 3.7368 you? 16.9651 Fixed manufacturing overhead 1.20 DLH 81.9700/DLH 2.3640 $19.3291 "Let's see," you reply. "I have the 1997-98 income statement (prior to bonus calculations), the breakdown of budgeted and actual revenues, and schedules of standard and actual direct production costs. I do need some more detailed information about manufac- turing overhead and selling costs. Af ter that, I'll get back to you as soon as I can." McKinley agrees to send you de tails of actual overhead expenditures for the last five years and actual sell- ing expenses for 1997 and 1998. These are shown in Tables 4 and 5. * One bolt of fabric is 10 yarda long hy 72 inches wide. Fabric for 42 finished units can be cut from one bolt. The cost of accessories varies from 7 centa per unit for a how tie tn 45 cents per unit for fisherman's gear. The stundard of 12 cents per unit reflects the historical assortment of excesories chosen by customers. Less than 0.01 hour per unit is spent cutting the fabric. Therefore, hours spent in the cutting operation are not separately recorded. They are included with hours spent operating the pneu- matic stuffing machine because both operations are usually performed by the same employees. "Variable and fixed averhead are allocated to production on the basis of standard direct labor hours allowed. Standard amounts are computed at normal capacity of 280,000 units. Maximum practical capacity is 360,000 units of production attainable in consideration of planned maintenance and scheduled down time for holidays. Normal capacity is the long-run average productive output that smoothes out Beasonal, cyclical, and other variations in customer demand. REQUIRED 1 a Using the information in the case and Tables 1-5, prepare a 292 Issues in Accounting Education Crawford and Ilenty 29 TABLE 3 Berkshire Toy Company A Division of Quality Products Corporation Schedule of Actual Manufacturing Costs for the Year Ended June 30, 1998 Quantity Used Input Price Total Cost Direct materials Acrylic pile fabric 10-mom acrylic eyes 46-mm plastic joints Polyester fiber filling Woven label Designer box Accessories Total direct materials 7,910 bolts 661,248 eyes 1,937,023 joints 344,166 lbs. 328,447 labels 315.854 boxes $32.4174/bolt $0.1900/eye $0.1270/joint $1.3100/1b. $0.0500 each $0.2200 each various $ 256,422 125,637 246,002 450,856 16.422 69,488 66,013 1.230,840 TABLE 4 Berkshire Toy Company A Division of Quality Products Corporation Schedule of Actual Manufacturing Overhead Expenditures for the Years Ended June 30, 1994 through 1998 1998 1997 1996 1995 1994 Units produced 825,556 271,971 252,114 227,546 201,763 Variable overhead: Payroll taxes and fringes $840.963 $524,846 S467,967 $413,937 8356,150 Overtime premiums 423,970 24,665 2,136 1,874 1,965 Cleaning supplies 4,993 6,842 6,119 5,485 4,996 Maintenance labor 415,224 256,883 232,798 244,037 216.142 Maintenance supplies 27,379 15,944 12,851 15,917 14,323 Miscellaneous 13,142 11,244 9,921 8,906 7,794 Total $1,725,665 $840,424 $731,792 $690.156 $601,370 $ Fixed overhead: Utilities S 121,417 $119,786 $117,243 $116,554 $113,229 Depreciation-machinery 28,500 28,500 28,500 28,500 28,500 Depreciation building 88.750 88,750 88,750 88,750 88,750 Insurance 62,976 61,716 57,211 56,544 54,988 Property taxes 70.101 70.101 68,243 68,243 66,114 Supervisory salarios 287,163 274,638 275,198 269,018 254,469 Total $ 668,897 $643,391 $635,145 $626,609 $606,050 Direct labor Sewing 189.211 hours Stuffing and cutting 104,117 hours Assembly 121.054 hours Dressing and packaging 34,610 hours Total direct labor 448,997 hours Overtime premium 103,787 hours Other variable manufacturing overhead S8.1700/hour $4.0850/hour 3.668,805 423,970 1,301,695 Fixed manufacturing overhead 658,897 $7,283,707 TABLE 5 Berkshire Toy Company A Division of Quality Products Corporation The actual input price for accessories is derived by dividing the actual cost of $66,012 by units sold (325,556), yielding an average accessories cuest of S0.20277 per beur. The actual input price for variable overhead is obtained by dividing the total variable overhend ($1,901,695 + $423,970) by actual direct labor houre worked, yielding a price or rate of $8.813377 per direct labor hour Schedule of Actual Selling Expenses for the Years Ended June 30, 1998 and 1997 1998 1997 325.556 271,971 Units sold: Variable expenses: Packing and shipping Commissions Catalogs, brochures, and samples Total $1,680,089 129,080 150.425 $1.859.694 $ S1,015,913 216.116 65,658 $1,297,687 Fixed expenses: Salaries Advertising and promotion Total $2.734,868 2,288.324 $5,023,192 $2,345,121 2,086,021 $4,431,142 294 Issues in Accounting Education 3. flexible budget for the Berkshire Toy Company for the year ended June 30, 1998. Analyze the company's total master (static) budget variance for the year. Compare the flexible and master (static) budgets and prepare a schedule showing the sales vol- ume variance. C Compare the ac- tual results and the flexible bud- get, and prepare a schedule showing the flexible budget vari- ance. Subdivide the flexible bud- get variances into the appropriate price (rate or spending) and effi- ciency (usage or quantity) vari- ances for materials, labor, and variable overhead. modifications to the incentive plan would you recommend? Why? (Optional) Suppose that Berk- shire Toy Company adopts a balanced scorecard (BSC) to mea- sure its performance. What per- formance dimensions are typi- cally included in a BSC? What specific performance measures (indicators) might be included in the scorecard? For useful baske ground information on BSCs, see Forsythe et al. (1999, 1318). b. Compute the bonuses earned in fiscal 1998, if any, by David Hall of the purchasing department, Rita Smith of the marketing de- partment, and Bill Wilford of the production department. 2. a. You will be assisting in the inves- tigation of certain variances. Us- ing the information provided, for- mulate some likely explanations for the observed variances. b. Comment on the advantages and disadvantages of the incentive compensation plan as it applies to department heads. What is the appropriate role of the budget in performance evaluation? What 8 For the sales revenue categories shown in Table 1, prepare a flexible budget based on actual units sold multiplied by the master (static) budget prices. For Internet sales, use a "revised" budget price of $42. To analyze sales volume effects, also prepare a second flexible budget for the sales revenue catego- ries based on the total of 325,556 units sold, multiplied by the budgeted mix (85 percent for retail, 0 percent for Internet, and 15 percent for wholesale). Multiply these quantities by the respective budgeted sales prices. The dif- ference between the two flexible budget amounts is generally termed a sales mix vari- ance," which quantifies the effect on income that results because the actual mix of distri- bution channels deviates from the budgeted mix. A comparison between the master (static) budget and the flexible budget prepared on the basis of the budgeted mix is the sales volume variance." This variance measures the effect on operating income of selling more or fewer units than planned. The net of the sales mix variance and the sales volume variance equals the sales activity variance." Price/Rate Variances F/U Flexible Budget Efficiency Variances F/U Flex-Flex Budget (SQxSP) (AQ x SP) $ 123,711 $ 1,926 U $ 125,637 $ F $ 424,851 $ 74,188 U $ 499,039 $ 48,183 F Direct materials: Acrylic pile fabric 10-mm acrylic eyes 45-mm plastic joints Polyester fiber filling Woven label Designer box Accessories Total direct materials Direct labor Variable overhead Total variable production costs Actual Costs (AQ x AP) 256,422 125,637 246,002 450,856 16,422 69,488 66,013 1,230,840 3,668,305 1,725,665 6,624,810 $ 2,328 F $ F 78,133 $ 39,067 1,181,215 75,805 $ 39,067 1,304,004 $ $ $ $ $ $ $ $ $ $ $ 6,317 26,946 U $ 5,523,091 771,065 U 6,294,156 330,654 U x Bonus Rate = Bonus Total Rita Smith: Actual net revenue: Actual revenue Variable selling expenses Fixed selling expenses Budgeted net revenue: Budgeted revenue Variable selling expenses Fixed selling expenses x Bonus Rate = Bonus Actual net revenue - Budgeted net revenue Bill Wilford: Production efficiency variances: Acrylic pile fabric quantity variance 10-mm acrylic eyes quantity variance 45-mm plastic joints quantity variance Polyester fiber filling quantity variance Woven label quantity variance Designer box quantity variance Accessories quantity variance Direct labor efficiency variance Variable overhead efficiency variance Direct labor rate variance Variable overhead rate variance Fixed overhead spending variance $ 3,023 F x Bonus Rate = Bonus Total 1. Based on the information provided in the case, provide likely explanations for at least one direct materials quantity variance, one direct materials price variance, the direct labor efficiency variance, and the direct labor rate variance. (Note: These explanations should be based on specific information provided in the case, not "the direct labor efficiency variance is unfavorable becaue the actual labor hours were more than the standard labor hours allowed.") 2. Comment on the advantages and disadvantages of the incentive compensation plan as it applies to department heads. 3. What changes to the incentive plan would you recommend? Why

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts