Answered step by step

Verified Expert Solution

Question

1 Approved Answer

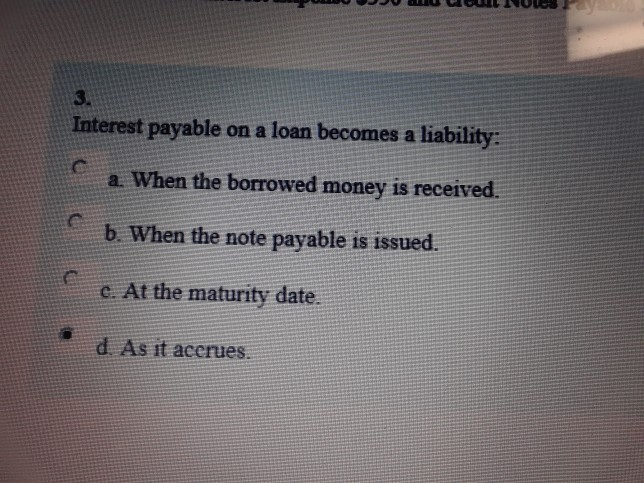

Interest payable on a loan becomes a liability: a. When the borrowed money is received. b. When the note payable is issued. c. At the

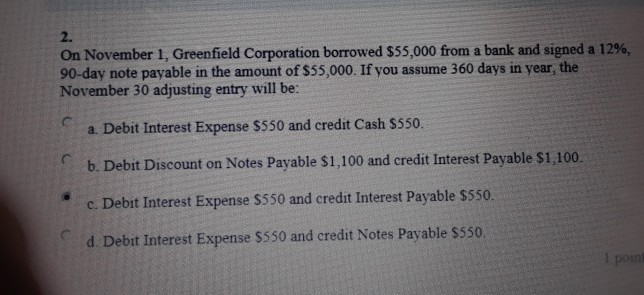

Interest payable on a loan becomes a liability: a. When the borrowed money is received. b. When the note payable is issued. c. At the maturity date. d. As it acerues. On November 1, Greenfield Corporation borrowed $55,000 from a bank and signed a 12% 90-day note payable in the amount of $55,000. If you assume 360 days in year, the November 30 adjusting entry will be: a. Debit Interest Expense $550 and credit Cash $550. b. Debit Discount on Notes Payable $1,100 and credit Interest Payable $1,100. c. Debit Interest Expense $550 and credit Interest Payable $550. d. Debit Interest Expense $550 and credit Notes Payable $550. 1 poum

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

GAO Financial Audit Manual Volume 3 June 2018

Authors: United States Government GAO

2018 Edition

979-8733166001