Answered step by step

Verified Expert Solution

Question

1 Approved Answer

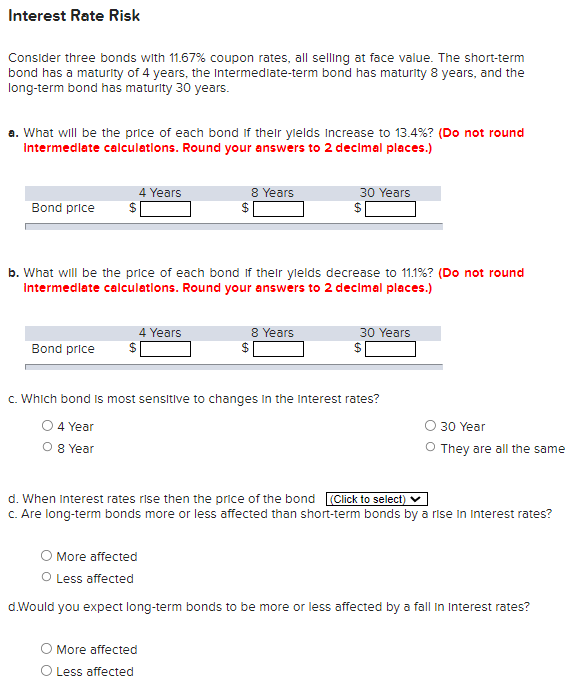

Interest Rate Risk Consider three bonds with 11.67% coupon rates, all selling at face value. The short-term bond has a maturity of 4 years, the

Interest Rate Risk Consider three bonds with 11.67% coupon rates, all selling at face value. The short-term bond has a maturity of 4 years, the Intermedlate-term bond has maturity 8 years, and the long-term bond has maturity 30 years. a. What will be the price of each bond If thelr ylelds increase to 13.4% ? (Do not round Intermedlate calculations. Round your answers to 2 decimal places.) b. What will be the price of each bond If thelr ylelds decrease to 11.1% ? (Do not round Intermedlate calculations. Round your answers to 2 decimal places.) c. Which bond Is most sensitive to changes in the Interest rates? 4Year8Year30YearTheyareallthesame d. When Interest rates rise then the price of the bond c. Are long-term bonds more or less affected than short-term bonds by a rise In Interest rates? More affected Less affected d.Would you expect long-term bonds to be more or less affected by a fall in Interest rates? More affected Less affected

Interest Rate Risk Consider three bonds with 11.67% coupon rates, all selling at face value. The short-term bond has a maturity of 4 years, the Intermedlate-term bond has maturity 8 years, and the long-term bond has maturity 30 years. a. What will be the price of each bond If thelr ylelds increase to 13.4% ? (Do not round Intermedlate calculations. Round your answers to 2 decimal places.) b. What will be the price of each bond If thelr ylelds decrease to 11.1% ? (Do not round Intermedlate calculations. Round your answers to 2 decimal places.) c. Which bond Is most sensitive to changes in the Interest rates? 4Year8Year30YearTheyareallthesame d. When Interest rates rise then the price of the bond c. Are long-term bonds more or less affected than short-term bonds by a rise In Interest rates? More affected Less affected d.Would you expect long-term bonds to be more or less affected by a fall in Interest rates? More affected Less affected Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Laymans Guide To Managing Your Investments

Authors: Thomas Dunleavy

1st Edition

979-8763592214