Question

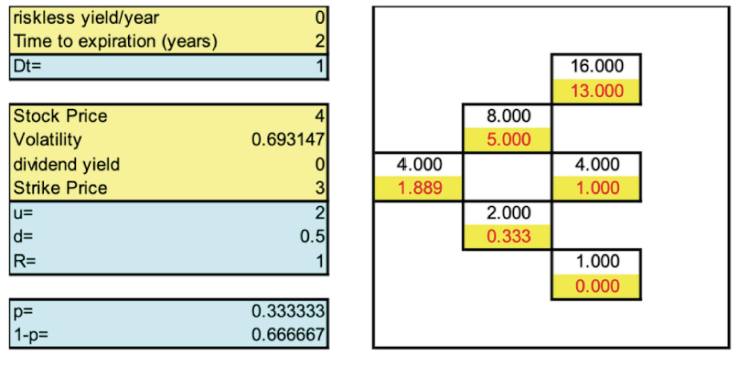

Interest rates are 0. A stock is priced at $4. In each period the stock can double or half inprice. Consider a two-period call option

Interest rates are 0. A stock is priced at $4. In each period the stock can double or half inprice. Consider a two-period call option with strike of $3.

Below is the lattice of stock prices and European option prices in red.

1. Use the above lattice of option prices to price a one-period compound option, that allows the holder to buy the call option for $1.00 in period one.

2. Compute the price of a claim that at date 0 pays out the stock price squared after 1 period.

riskless yield/year Time to expiration (years) Dt= 0 2 1 16.000 13.000 8.000 5.000 Stock Price Volatility dividend yield Strike Price u= d= R= 4.000 1.889 0.693147 30 2 0.5 1 4.000 1.000 2.000 0.333 1.000 0.000 p= 1-p= 0.333333) 0.666667 riskless yield/year Time to expiration (years) Dt= 0 2 1 16.000 13.000 8.000 5.000 Stock Price Volatility dividend yield Strike Price u= d= R= 4.000 1.889 0.693147 30 2 0.5 1 4.000 1.000 2.000 0.333 1.000 0.000 p= 1-p= 0.333333) 0.666667

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mastering Islamic Finance

Authors: Faizal Karbani

1st Edition

1292001445, 978-1292001449