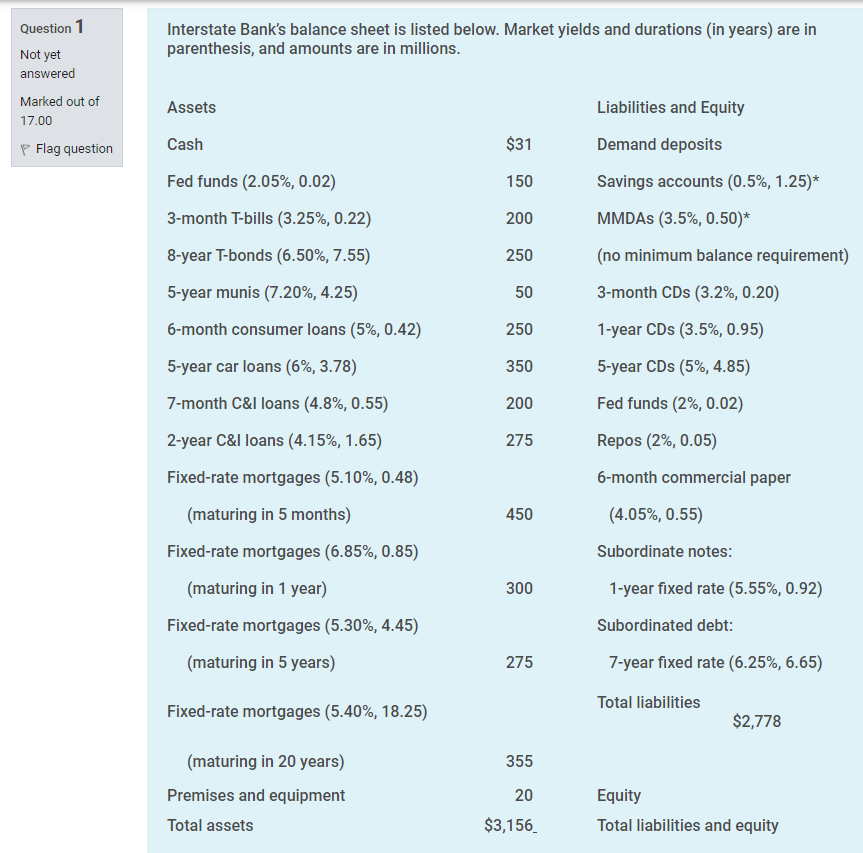

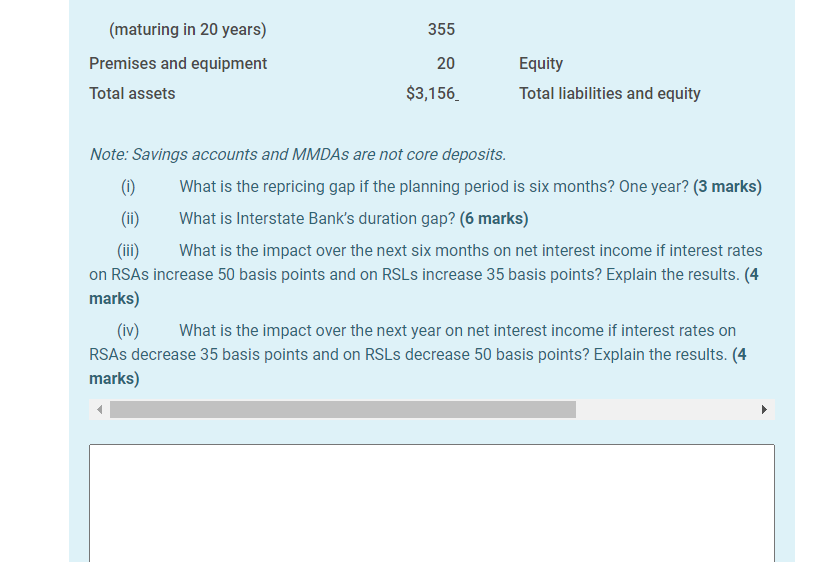

- Interstate Banks balance sheet is listed below. Market yields and durations (in years) are in parenthesis, and amounts are in millions.

Question 1 Not yet answered Interstate Bank's balance sheet is listed below. Market yields and durations (in years) are in parenthesis, and amounts are in millions. Assets Marked out of 17.00 Flag question $31 Cash Fed funds (2.05%, 0.02) Liabilities and Equity Demand deposits Savings accounts (0.5%, 1.25)* 150 200 MMDAs (3.5%, 0.50)* 250 3-month T-bills (3.25%, 0.22) 8-year T-bonds (6.50%, 7.55) 5-year munis (7.20%, 4.25) 6-month consumer loans (5%, 0.42) 5-year car loans (6%, 3.78) (no minimum balance requirement) 3-month CDs (3.2%, 0.20) 50 250 1-year CDs (3.5%, 0.95) 350 5-year CDs (5%, 4.85) 7-month C&l loans (4.8%, 0.55) 200 Fed funds (2%, 0.02) 2-year C&I loans (4.15%, 1.65) 275 Repos (2%, 0.05) Fixed-rate mortgages (5.10%, 0.48) 6-month commercial paper (maturing in 5 months) 450 (4.05%, 0.55) Subordinate notes: 1-year fixed rate (5.55%, 0.92) 300 Fixed-rate mortgages (6.85%, 0.85) (maturing in 1 year) Fixed-rate mortgages (5.30%, 4.45) (maturing in 5 years) Subordinated debt: 275 7-year fixed rate (6.25%, 6.65) Total liabilities Fixed-rate mortgages (5.40%, 18.25) $2,778 355 (maturing in 20 years) Premises and equipment Total assets 20 Equity Total liabilities and equity $3,156 355 (maturing in 20 years) Premises and equipment Total assets 20 $3,156 Equity Total liabilities and equity Note: Savings accounts and MMDAs are not core deposits. (0) What is the repricing gap if the planning period is six months? One year? (3 marks) (ii) What is Interstate Bank's duration gap? (6 marks) (iii) What is the impact over the next six months on net interest income if interest rates on RSAs increase 50 basis points and on RSLs increase 35 basis points? Explain the results. (4 marks) (iv) What is the impact over the next year on net interest income if interest rates on RSAs decrease 35 basis points and on RSLs decrease 50 basis points? Explain the results. (4 marks) Question 1 Not yet answered Interstate Bank's balance sheet is listed below. Market yields and durations (in years) are in parenthesis, and amounts are in millions. Assets Marked out of 17.00 Flag question $31 Cash Fed funds (2.05%, 0.02) Liabilities and Equity Demand deposits Savings accounts (0.5%, 1.25)* 150 200 MMDAs (3.5%, 0.50)* 250 3-month T-bills (3.25%, 0.22) 8-year T-bonds (6.50%, 7.55) 5-year munis (7.20%, 4.25) 6-month consumer loans (5%, 0.42) 5-year car loans (6%, 3.78) (no minimum balance requirement) 3-month CDs (3.2%, 0.20) 50 250 1-year CDs (3.5%, 0.95) 350 5-year CDs (5%, 4.85) 7-month C&l loans (4.8%, 0.55) 200 Fed funds (2%, 0.02) 2-year C&I loans (4.15%, 1.65) 275 Repos (2%, 0.05) Fixed-rate mortgages (5.10%, 0.48) 6-month commercial paper (maturing in 5 months) 450 (4.05%, 0.55) Subordinate notes: 1-year fixed rate (5.55%, 0.92) 300 Fixed-rate mortgages (6.85%, 0.85) (maturing in 1 year) Fixed-rate mortgages (5.30%, 4.45) (maturing in 5 years) Subordinated debt: 275 7-year fixed rate (6.25%, 6.65) Total liabilities Fixed-rate mortgages (5.40%, 18.25) $2,778 355 (maturing in 20 years) Premises and equipment Total assets 20 Equity Total liabilities and equity $3,156 355 (maturing in 20 years) Premises and equipment Total assets 20 $3,156 Equity Total liabilities and equity Note: Savings accounts and MMDAs are not core deposits. (0) What is the repricing gap if the planning period is six months? One year? (3 marks) (ii) What is Interstate Bank's duration gap? (6 marks) (iii) What is the impact over the next six months on net interest income if interest rates on RSAs increase 50 basis points and on RSLs increase 35 basis points? Explain the results. (4 marks) (iv) What is the impact over the next year on net interest income if interest rates on RSAs decrease 35 basis points and on RSLs decrease 50 basis points? Explain the results. (4 marks)