Answered step by step

Verified Expert Solution

Question

1 Approved Answer

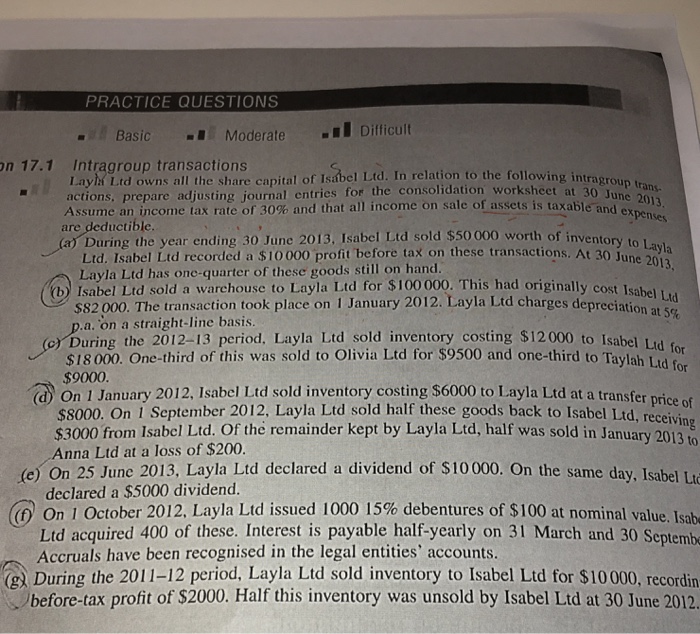

Intragroup transactions Layla Ltd owns all the share capital of Isabel Ltd. In relation to the following intragroup transactions, prepare adjusting journal entries for the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Practitioners Guide To Business Impact Analysis Internal Audit And IT Audit

Authors: Priti Sikdar

1st Edition

036756792X, 978-0367567927