Answered step by step

Verified Expert Solution

Question

1 Approved Answer

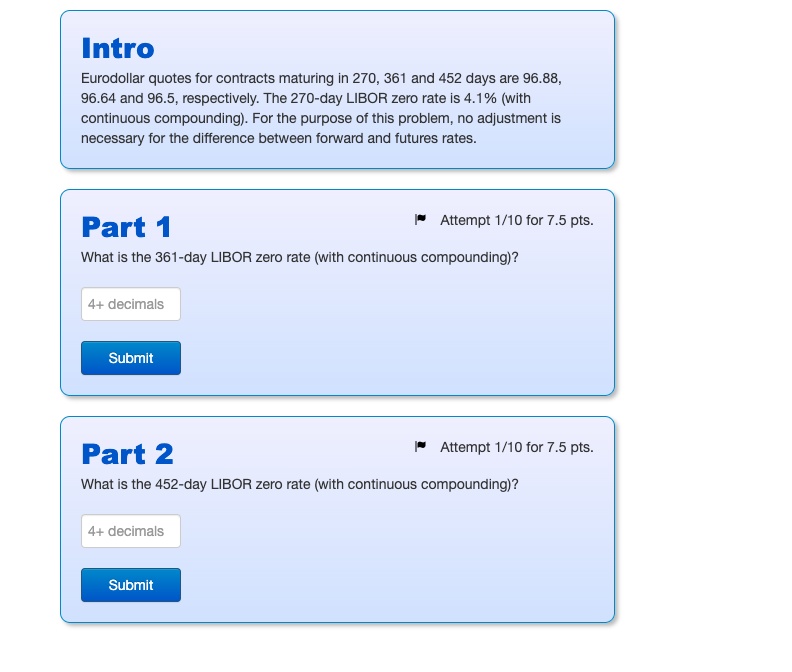

Intro Eurodollar quotes for contracts maturing in 270, 361 and 452 days are 96.88, 96.64 and 96.5, respectively. The 270-day LIBOR zero rate is 4.1%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trading For Beginners 25 Secrets To Trade For A Living

Authors: Mark Bresett

1st Edition

1521327742, 978-1521327746