Answered step by step

Verified Expert Solution

Question

1 Approved Answer

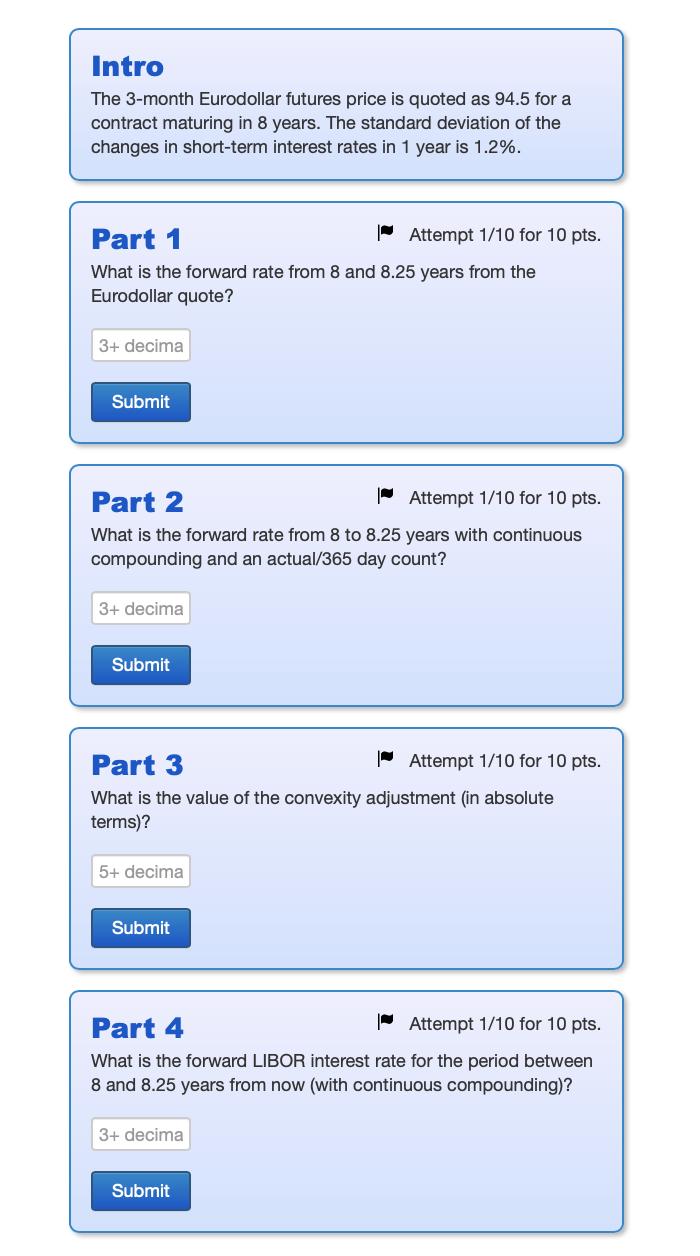

Intro The 3-month Eurodollar futures price is quoted as 94.5 for a contract maturing in 8 years. The standard deviation of the changes in

Intro The 3-month Eurodollar futures price is quoted as 94.5 for a contract maturing in 8 years. The standard deviation of the changes in short-term interest rates in 1 year is 1.2%. Part 1 Attempt 1/10 for 10 pts. What is the forward rate from 8 and 8.25 years from the Eurodollar quote? 3+ decima Submit Part 2 Attempt 1/10 for 10 pts. What is the forward rate from 8 to 8.25 years with continuous compounding and an actual/365 day count? 3+ decima Submit Part 3 Attempt 1/10 for 10 pts. What is the value of the convexity adjustment (in absolute terms)? 5+ decima Submit Part 4 Attempt 1/10 for 10 pts. What is the forward LIBOR interest rate for the period between 8 and 8.25 years from now (with continuous compounding)? 3+ decima Submit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Eurodollar Futures Analysis Heres an analysis of the Eurodollar futures contract information provide...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial management theory and practice

Authors: Eugene F. Brigham and Michael C. Ehrhardt

12th Edition

978-0030243998, 30243998, 324422695, 978-0324422696