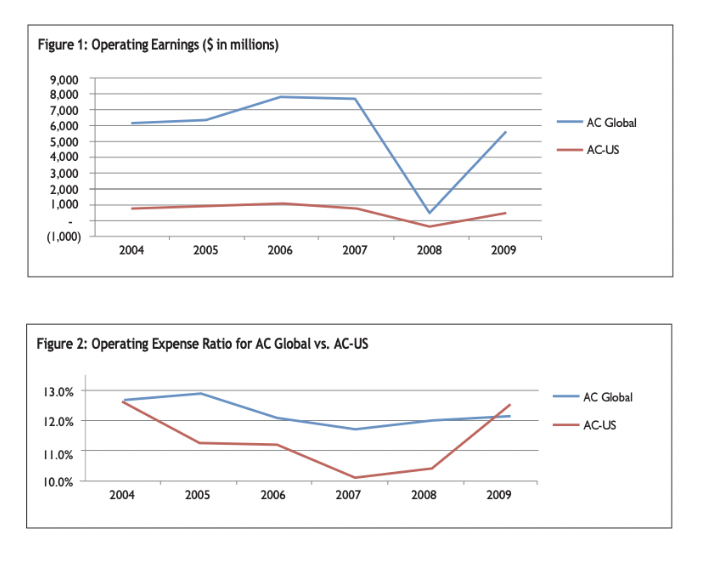

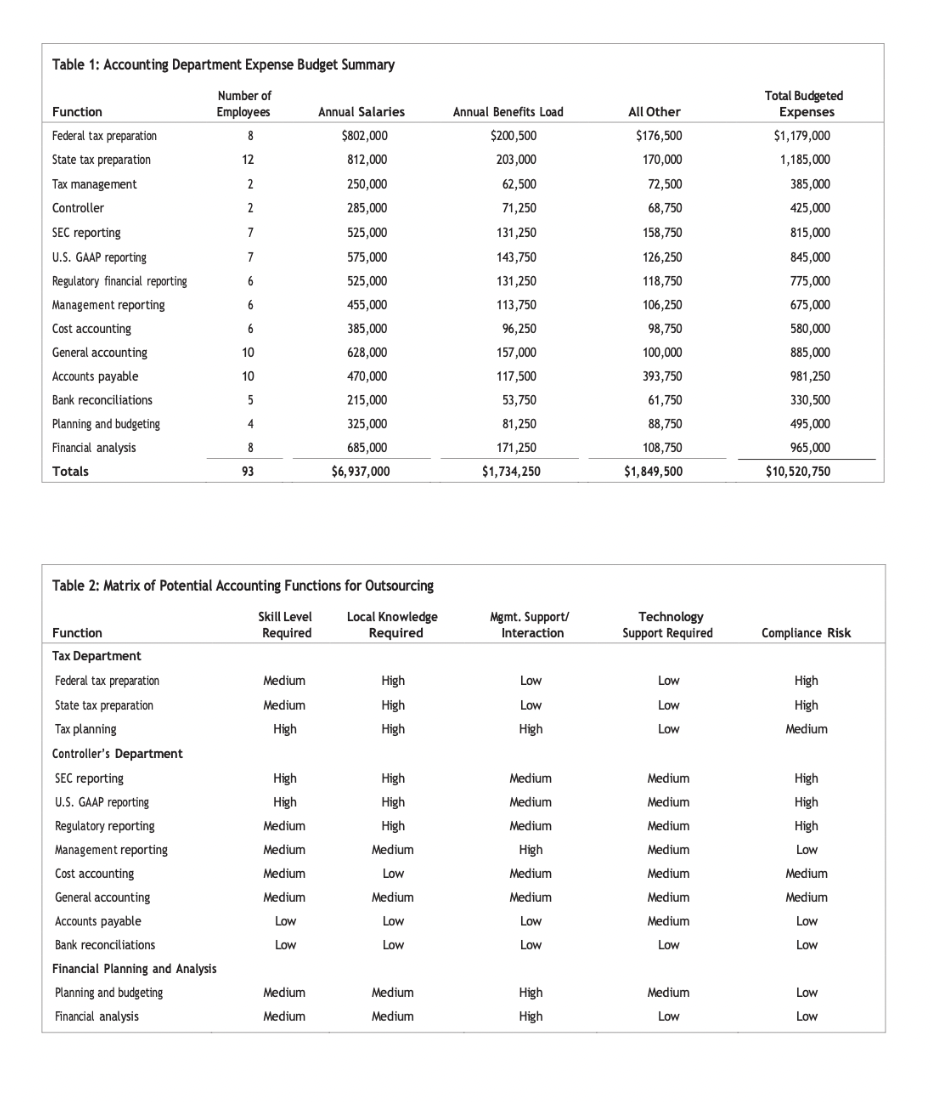

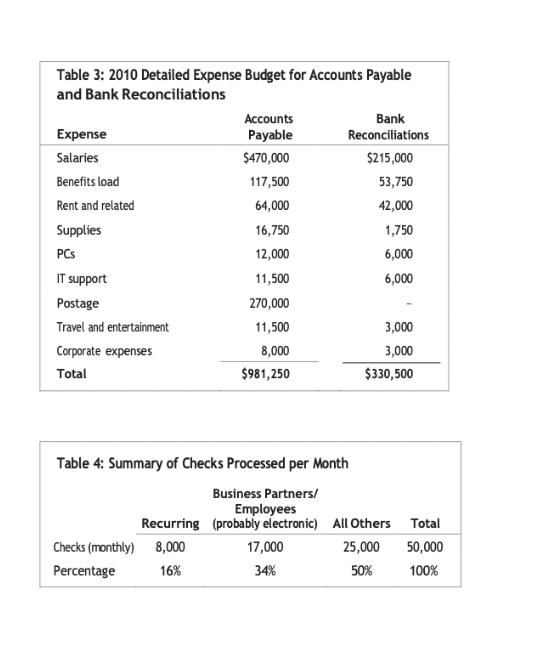

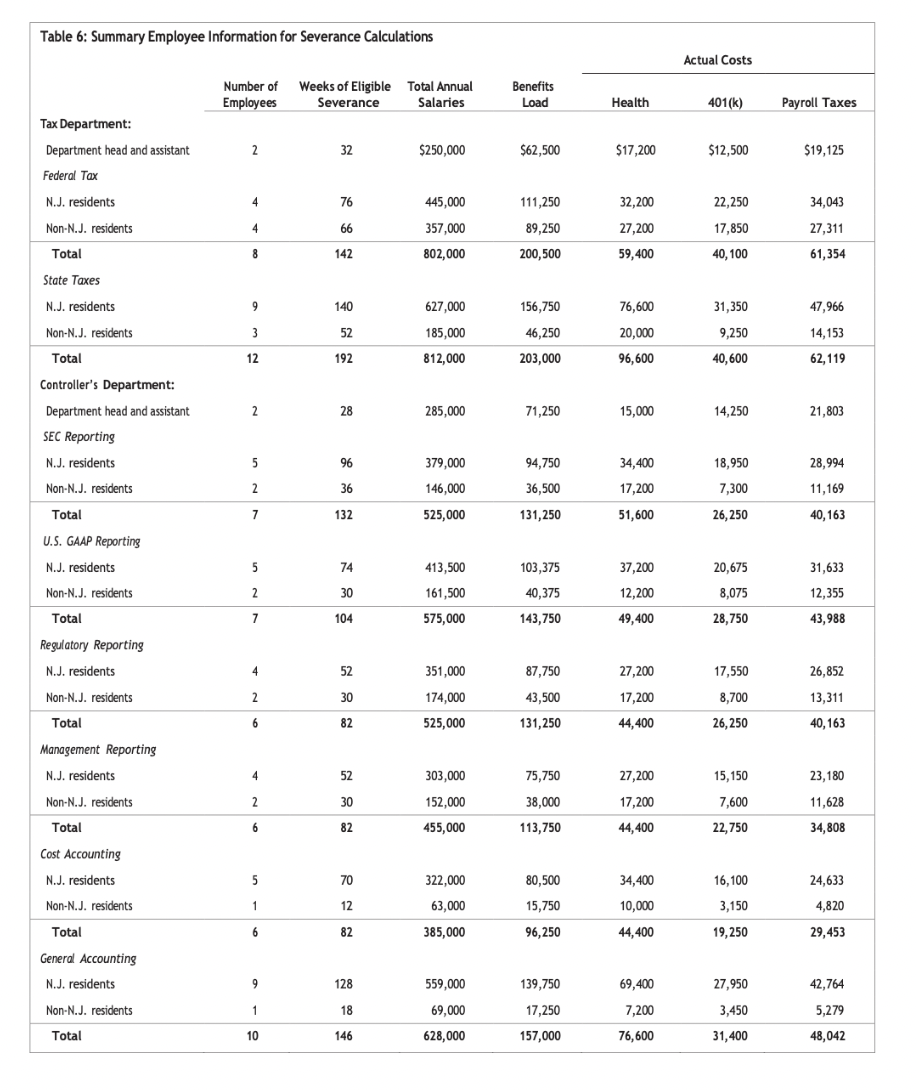

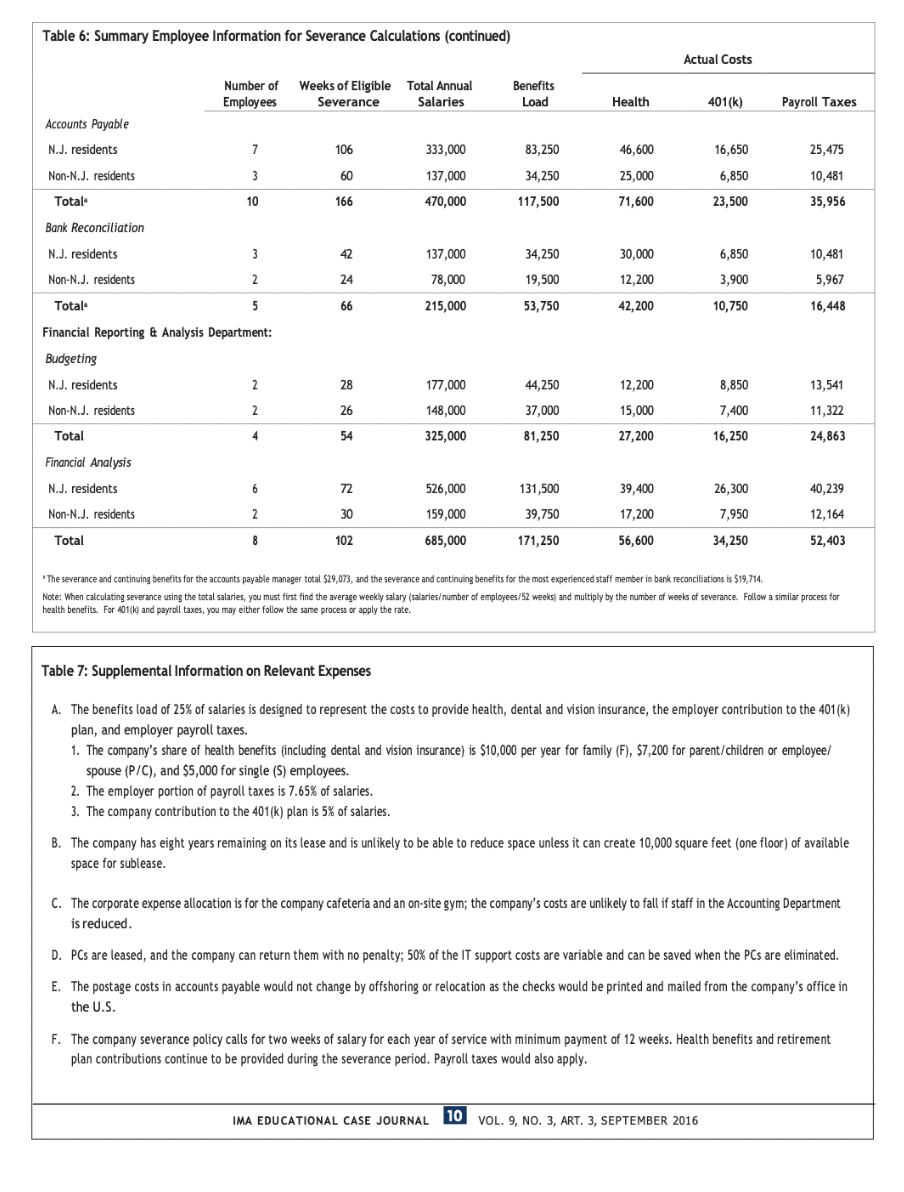

INTRODUCTION IMPACT ON SHORT-TERM PROFITS This case is based on a real-life project and takes place in 2010 at the New York City headquarters for the United States operations of AC Global, Inc. (The real name has been changed.) AC Global is a multinational insurance company with its headquarters in France and annual revenue ranking in the top 10 companies globally. The company has significant operations in the United States, Europe, Japan, and Australia, and the operations in each country are separate insurance companies and operate with a large degree of autonomy. Recently, AC Global established insurance operations and a servicing center in India. The servicing center in India primarily provides some information technology (IT) support for the insurance operations in the United Kingdom (U.K.), Belgium, and France. The ongoing global recession has significantly decreased the profitability of AC Global, increasing the importance of reducing costs. AC Global's operations in the U.S. (AC-US) sell life and annuity products and represent approximately 20% of the group's life and annuity revenues. AC-US has approximately 3,000 employees, with about 1,000 employees based in the New York City headquarters. The remaining employees are located at the company's service centers in New Jersey, Pennsylvania, and North Carolina. For an insurance company, there are four key line items on the income statement: premium revenue, investment income, benefits/claims expense, and operating expenses. Operating expenses provide the greatest opportunity for short-term improvement in earnings since the other line items are less controllable or the impacts of changes emerge over a long period of time. Investment income is primarily composed of interest and dividends on bonds and common stock investments and is not changed through operating actions. Premium revenue is composed of fees collected for providing insurance coverage and is only modestly impacted by current sales. Benefits and claims are paid to policyholders and their beneficiaries and are also difficult to impact in the short-term. The global economic downturn that began in late 2008 put intense pressure on the financial services industry. During 2009, U.S. sales of annuity products decreased by 30% while life insurance sales fell by 15%. Like the industry, AC Global has been negatively impacted by the economic downturn. AC-US premium revenue fell 8% cumulatively between 2007 and 2009. In 2010, the company's operations remained stable, but revenue was expected to be similar to 2009. AC Global's operating earnings decreased over 80% from 2007 to 2008, and AC-US suffered an operating loss in 2008. Although operating earnings recovered somewhat in 2009 (shown in Figure 1), the earnings for AC Global consolidated and AC-US are still 36% and 40%, respectively, below those in 2007. As a result, the company's stock price is down nearly 50% since the beginning of the crisis in 2008. AC-US measures operating efficiency based on the expense ratio, which is operating expenses divided by premium revenue. In 2004, AC-US went through a restructuring that reduced personnel overlap and inefficiency. Through the restructuring, AC-US reduced the workforce by 4%, reduced operating expenses by 5%, and improved the expense ratio from 12.7% in 2004 to 10.1% by 2007, 14% better than the expense ratio of 11.7% for AC Global. While operating expenses have grown modestly at 2% since 2007, the expense ratio for AC-US increased from 10.1% in 2007 to over 12.5% in 2009, worse than the 12.1% for AC Global. AC-US has underperformed AC Global in earnings and cost efficiency during 2009, which is concerning for the management of AC-US (see Figure 2). functions in the service center in India and gave George the contact information for Sanjay Delphi, the project manager for the company's India facility. George believes that in addition to outsourcing offshoring), increasing the use of electronic payments in accounts payable is another viable ways to reduce costs. George made notes on information regarding expenses relevant for the analysis, including the severance policy (see Table 7, section F). George also pulled up the organization chart to list all of the various accounting functions as well as their annual expense budgets (Table 1). He assembled information on the staff in each of the accounting functions, including their salaries, benefits, residence, and possible severance based on the years of service and prepared a summary by function (see Table 6). George meets with two of his team members, Samantha Charleston and Ryan Falkirk, to explain the project. OFFSHORING COST REDUCTION ANALYSIS PROJECT Peter George is a vice president responsible for financial planning and analysis (FP&A) at AC-US in New York. In his role, George and his team evaluate all significant projects with financial implications. George led the team that analyzed and recommended the restructuring six years ago that significantly improved the expense ratio. George met with Brian Thomas, the chief financial officer (CFO). Thomas had reviewed the first quarter preliminary revenue and earnings and told George that it is imperative for the company to find ways to reduce expenses to improve earnings. Before engaging the rest of the organization, the CFO would like the functions he manages to take a leadership position in the cost reductions-not just recommending cost- reduction actions but also providing examples to show they are effective. Thomas reviewed the accounting function first and decided he wants it to reduce expenses. Thomas asked George to evaluate potential cost-saving alternatives and provide him with a preliminary analysis within one week. Thomas then informed George that the company has recently began performing some accounting George reviews some general information on offshoring and finds that global offshoring has grown rapidly. He finds that accounting processes such as accounts payable, accounts receivable, sales ledger, general ledger, financial reporting, and bank processing are increasingly offshored.? George calls Delphi to discuss the services performed at the servicing center in India. Delphi informs George that the service center currently provides some IT support for the insurance operations in the U.K., Belgium, and France; performs some customer service functions; and also recently added a few accounting functions. Delphi emphasized that the service center is just beginning to add staff with accounting expertise and has minimal knowledge of U.S. generally accepted accounting principles (GAAP) state regulatory accounting requirements, and U.S. tax law (the U.S. Internal Revenue Code). George determines that the first step in his analysis is to identify which accounting functions would be the best candidates for offshoring and then analyze the financial and logistical feasibility of doing that. George prepares a matrix to assist him in analyzing which functions would be the most appropriate to offshore (see Table 2). His matrix takes Department. Josephine Young, of the IT Department, analyzes the requirements and informs George that they would need to improve connectivity and alter the time of the batch processing for accounts payable. She estimates there would be a one-time cost of $100,000 plus $2,500 per month for improved connectivity. The change in the batch processing time will also cause an increase in personnel costs of $2,500 per month. But there are no additional technology requirements for offshoring bank reconciliations. AUTOMATING ELECTRONIC PAYMENTS into account required skill levels, local knowledge of the U.S. Internal Revenue Code, for example), compliance risk, technological support, and the need for direct management oversight-which may be difficult due to distance and differences in time zones. He rates the functions on each of the criteria as high, medium, and low. George concludes that the functions that score low or medium on all of the criteria would be the best candidates for outsourcing. Based on the matrix, he believes that the accounts payable and bank reconciliation functions are the best candidates for initial consideration. The accounts payable function has a separate manager while the bank reconciliation function reports to the manager of general accounting. The Bank Reconciliation Department prepares 50 reconciliations per month (600 per year), and the Accounts Payable Department processes 50,000 checks per month (600,000 per year). George reviews the annual expense budgets (provided in Table 3). George sends Delphi an email and requests information on the accounts payable and bank reconciliation service functions. Delphi responds that the charges for outsourced services for accounts payable and bank reconciliation are a base monthly fee of $1,250 for each function ($15,000 per year) plus $0.65 per payment for processing accounts payable and $200 per bank reconciliation. Delphi also informs George that the U.S.-based operations would need to maintain staff to coordinate the transfer of information. Based on a similar project being undertaken by the company's U.K. operations, Delphi estimates that one staff member within the Accounting Department should be sufficient to support both accounts payable and bank reconciliations. Delphi and George discuss the necessary skills. George believes that retaining the accounts payable manager, who likely has the necessary skills, would be a good solution-and he uses that assumption for his analysis. The accounts payable manager's annual salary is $75,000. The allocated benefits charge is $18,750, but actual benefits and taxes are $19,488. George estimates that the cost for a personal computer, supplies, travel, and all other expenses (excluding postage) would total $15,500. He assumes that the salary, benefits and other expenses associated with the manager would be allocated 65% to accounts payable and 35% to bank reconciliations based upon the estimated time requirements to support each function. George does not include the allocation of rent, corporate expenses, or 50% of IT support in his cost-reduction estimate. Delphi also gives George the data transfer and connectivity specifications to discuss with the IT Charleston performs some background research on electronic payments. She finds that the use of electronic payments has increased substantially as the number of checks used in business-to-business transactions rose. The use of paper checks decreased by 5% from 2006 to 2009. The estimated savings from using electronic payment instead of paper checks ranged from 20% to 90%. Since the accounts payable function issues all of its payments as checks, Charleston believes that there may be significant savings if the company made greater use of electronic payments. Charleston contacts the company's corporate banking representative to inquire about electronic payments alternatives. She finds that the bank charges an average of $0.125 per electronic payment. The bank also provides Charleston with a contact at a company that recently adopted electronic payments (identified as Company XYZ). As a means to estimate the potential impacts, she contacts Company XYZ's treasurer to discuss how it impacted their staffing needs and costs and is informed that Company XYZ averaged 2 minutes in labor per manual check and only 1.5 minutes for each electronic payment. For recurring payments, Company XYZ experienced an 80% time savings annually. To support her analysis, Charleston requests and receives a report showing the number of the company's checks that are recurring to vendors as well as those to employees and business partners, which are good candidates for electronic payments (see Table 4). Based on her preliminary analysis, Charleston estimates that the company could process up to 50% of its current payments electronically. Using the results for Company XYZ as a proxy, she estimates that electronic payments would reduce processing time by 25% for each electronic payment. Since recurring payments require minimal work after initial set-up, the potential estimated time savings is 80%. Since 16% of payments are recurring, labor savings would be possible. Charleston estimates that electronic payment processing would reduce staff, with associated reductions in salaries and benefits as well as other associated costs. To estimate the impact on staff, she uses 10 employees processing 600,000 checks annually and assumes that 50% of the payments could become electronic. To calculate the potential savings in salaries and benefits, she assumes that the staff reductions would involve less-experienced staff and represent 15% of total salaries and benefits for accounts payable. She estimates also that there would be savings in personal computer (PC) costs, IT support, and other costs of $1,775 per employee. Additionally, there would be a reduction in postage costs in direct proportion to the reduction of the number of checks. These savings would be partially offset by an additional cost of $0.125 for each electronic payment that replaces a check. Further, she uses the information from Table 6 to estimate that severance costs would represent 15% of the maximum eligible severance for accounts payable. INTERACTION OF ALTERNATIVES If the company only outsources bank reconciliations, the team has assumed that the bank reconciliation department will need to retain the most experienced employee to support the process. The most experienced employee in the department has eight years of service, a salary of $48,000, health insurance costs of $10,000, 401(k) contributions at 5%, and payroll taxes of 7.65%. In addition to the savings in salaries and benefits for the positions eliminated in bank reconciliations, it is also estimated that there would be a savings of $8,000 in total for expenses other than salaries and benefits. The one time initial costs would consist of severance costs for the positions eliminated. 2. Considering the alternative of Electronic Processing of half checks AND offshoring bank reconciliation only: a. Using the information that Charleston gathered on electronic payment processing of 50% of the accounts payable checks, determine the number of potential accounting payable staff reduction. b. Based on the potential staff reduction, determine the annual cost savings from electronic processing of 50% of the accounts payable checks AND offshoring bank reconciliation. c. If AC-US outsources bank reconciliations and changes to electronic payment of 50% of the accounts payable checks, what would be the maximum combined savings over the next three years, including the one-time severance costs? ENDNOTES "Annual Report on the Insurance Industry, Federal Insurance Office of the U.S. Treasury, June 2013. 2Nora Palugod and Paul A. Palugod, "Global Trends in Offshoring and Outsourcing," Internal Journal of Business and Social Science, September 2011. 3"The 2010 Federal Reserve Payments Study: Noncash Payment Trends in the United States: 2006-2009,"updated April 5, 2011, Federal Reserve System. *Matthew Heller, "Electronic Payments 10 Times Cheaper Than Checks, CFO.com, October 12, 2015. Estimated staff reduction based on 600,000 checks supported by 10 full-time employees (FTES). Estimate 300,000 checks, or 50%, with similar level of FTE support per check. The necessary FTEs to support electronic payments (34% of payments) assume 25% time savings for electronic payments. The remaining 16% of payments are recurring electronic payments and estimate an 80% time savings. Figure 1: Operating Earnings ($ in millions) 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 AC Global - AC-US (1,000) 2004 2005 2006 2007 2008 2009 Figure 2: Operating Expense Ratio for AC Global vs. AC-US 13.0% AC Global - AC-US 12.0% 11.0% 10.0% 2004 2005 2006 2007 2008 2009 Table 1: Accounting Department Expense Budget Summary Number of Employees Annual Salaries $802,000 8 12 812,000 2 2 7 250,000 285,000 525,000 575,000 525.000 7 6 Function Federal tax preparation State tax preparation Tax management Controller SEC reporting U.S. GAAP reporting Regulatory financial reporting Management reporting Cost accounting General accounting Accounts payable Bank reconciliations Planning and budgeting Financial analysis Totals Annual Benefits Load $200,500 203,000 62,500 71,250 131,250 143,750 131,250 113,750 96,250 157,000 117,500 53,750 81,250 171,250 $1,734,250 All Other $176,500 170,000 72,500 68,750 158,750 126,250 118,750 106,250 98,750 100,000 393,750 61,750 88,750 108,750 $1,849,500 Total Budgeted Expenses $1,179,000 1,185,000 385,000 425,000 815,000 845,000 775,000 675,000 580,000 885,000 981,250 330,500 495,000 965,000 $10,520,750 6 455,000 385,000 6 10 10 5 628,000 470,000 215,000 325,000 685,000 $6,937,000 4 8 93 Table 2: Matrix of Potential Accounting Functions for Outsourcing Skill Level Required Local knowledge Required Mgmt. Support / Interaction Technology Support Required Compliance Risk Function Tax Department Federal tax preparation Medium High Low Low Medium Low Low High High High High Medium High High Low High Medium Medium Medium Medium High High Medium Medium High High Medium High High High Medium Medium Medium Low State tax preparation Tax planning Controller's Department SEC reporting U.S. GAAP reporting Regulatory reporting Management reporting Cost accounting General accounting Accounts payable Bank reconciliations Financial Planning and Analysis Planning and budgeting Financial analysis High Medium Medium Medium Medium Low Medium Medium Medium Low Medium Medium Low Low Low Low Medium Low Low Low Low Medium Medium Low Medium Medium High High Medium Low Low Table 3: 2010 Detailed Expense Budget for Accounts Payable and Bank Reconciliations Accounts Bank Expense Payable Reconciliations Salaries $470,000 $215,000 Benefits load 117,500 53,750 Rent and related 64,000 42,000 Supplies 16,750 1,750 PCS 12,000 6,000 IT support 11,500 6,000 Postage 270,000 Travel and entertainment 11,500 3,000 Corporate expenses 8,000 3,000 Total $981,250 $330,500 Table 4: Summary of Checks Processed per Month Business Partners/ Employees Recurring (probably electronic) All Others Total Checks (monthly) 8,000 17,000 25,000 50,000 Percentage 16% 34% 50% 100% Table 6: Summary Employee Information for Severance Calculations Actual Costs Number of weeks of Eligible Total Annual Employees Severance Salaries Benefits Load Health 401(k) Payroll Taxes Tax Department: Department head and assistant 2. 32 $250,000 $62,500 $ $17,200 $12,500 $19,125 Federal Tax N.J. residents 4 76 445,000 111,250 32,200 22,250 34,043 4 66 27,200 17,850 Non-N.J. residents -. Total 357,000 802,000 89,250 200,500 27,311 61,354 8 142 59,400 40, 100 State Taxes N.J. residents 9 140 156,750 76,600 20,000 Non-N.J. residents 627,000 185,000 812,000 47,966 14,153 3 52 192 46,250 31,350 9,250 40,600 Total 12 203,000 96,600 62,119 Controller's Department: 2 28 285,000 71,250 15,000 14,250 21,803 Department head and assistant SEC Reporting N.J. residents Non-N.J. residents - Total 5 96 94,750 34,400 18,950 28,994 379,000 146,000 2 36 36,500 17,200 7,300 11,169 7 132 525,000 131,250 51,600 26,250 40,163 U.S. GAAP Reporting N.J. residents 5 74 413,500 103,375 20,675 31,633 2 30 161,500 40,375 37,200 12,200 49,400 Non-N.J. residents . Total 8,075 12,355 43,988 7 104 575,000 143,750 28,750 Regulatory Reporting N.J. residents 4 52 87,750 27,200 17,550 26,852 351,000 174,000 2 30 17,200 13,311 Non-N.J. residents . Total 43,500 131,250 8,700 26,250 6 82 525,000 44,400 40,163 Management Reporting N.J. residents 4 52 75,750 27,200 23,180 2 30 303,000 152,000 455,000 38,000 Non-N.J. residents Total 17,200 15,150 7,600 22,750 11,628 34,808 6 82 113,750 44,400 Cost Accounting N.J. residents Non-N.J. residents 5 70 322,000 80,500 34,400 16,100 24,633 1 1 12 63,000 15,750 10,000 4,820 3,150 19,250 Total 6 82 385,000 96,250 44,400 29,453 General Accounting N.J. residents 9 128 559,000 139,750 69,400 27,950 42,764 Non-N.J. residents 1 18 69,000 7,200 3,450 5,279 17,250 157,000 Total 10 146 628,000 76,600 31,400 48,042 Table 6: Summary Employee Information for Severance Calculations (continued) Actual Costs Number of Weeks of Eligible Total Annual Employees Severance Salaries Benefits Load Health 401(k) Payroll Taxes Accounts Payable 7 106 83,250 46,600 16,650 N.J. residents Non-N.J. residents . Total 3 333,000 137,000 470,000 60 166 34,250 25,000 71,600 6,850 23,500 25,475 10,481 35,956 10 117,500 Bank Reconciliation N.J. residents 3 42 34,250 30,000 6,850 10,481 24 137,000 78,000 215,000 19,500 12,200 3,900 5,967 66 53,750 42,200 10,750 16,448 Non-N.J. residents . 2 Totale 5 Financial Reporting & Analysis Department: Budgeting N.J. residents 2 177,000 44,250 12,200 28 26 8,850 7,400 2 2 148,000 37,000 15,000 Non-N.J. residents . Total 13,541 11,322 24,863 4 4 54 325,000 81,250 27,200 16,250 Financial Analysis N.J. residents 6 72 526,000 131,500 39,400 26,300 40,239 Non-N.J. residents -. 2 30 159,000 39,750 17,200 7,950 12,164 Total 8 102 685,000 171,250 56,600 34,250 52,403 "The severance and continuing benefits for the accounts payable manager total $29,073, and the severance and continuing benefits for the most experienced staff member in bank reconciliations is $19,714. Note: When calculating severance using the total salaries, you must first find the average weekly salary (salariesumber of employees/52 weeks) and multiply by the number of weeks of severance. Follow a similar process for health benefits. For 401(k) and payroll taxes, you may either follow the same process or apply the rate. Table 7: Supplemental Information on Relevant Expenses A. The benefits load of 25% of salaries is designed to represent the costs to provide health, dental and vision insurance, the employer contribution to the 401(k) plan, and employer payroll taxes. 1. The company's share of health benefits (including dental and vision insurance) is $10,000 per year for family (F), $7,200 for parent/children or employee/ spouse (P/C), and $5,000 for single (5) employees. 2. The employer portion of payroll taxes is 7.65% of salaries. 3. The company contribution to the 401(k) plan is 5% of salaries. B. The company has eight years remaining on its lease and is unlikely to be able to reduce space unless it can create 10,000 square feet (one floor) of available space for sublease. C. The corporate expense allocation is for the company cafeteria and an on-site gym; the company's costs are unlikely to fall if staff in the Accounting Department is reduced. D. PCs are leased, and the company can return them with no penalty; 50% of the IT support costs are variable and can be saved when the PCs are eliminated. E. The postage costs in accounts payable would not change by offshoring or relocation as the checks would be printed and mailed from the company's office in the U.S. F. The company severance policy calls for two weeks of salary for each year of service with minimum payment of 12 weeks. Health benefits and retirement plan contributions continue to be provided during the severance period. Payroll taxes would also apply. IMA EDUCATIONAL CASE JOURNAL 10 VOL. 9, NO. 3, ART. 3, SEPTEMBER 2016 INTRODUCTION IMPACT ON SHORT-TERM PROFITS This case is based on a real-life project and takes place in 2010 at the New York City headquarters for the United States operations of AC Global, Inc. (The real name has been changed.) AC Global is a multinational insurance company with its headquarters in France and annual revenue ranking in the top 10 companies globally. The company has significant operations in the United States, Europe, Japan, and Australia, and the operations in each country are separate insurance companies and operate with a large degree of autonomy. Recently, AC Global established insurance operations and a servicing center in India. The servicing center in India primarily provides some information technology (IT) support for the insurance operations in the United Kingdom (U.K.), Belgium, and France. The ongoing global recession has significantly decreased the profitability of AC Global, increasing the importance of reducing costs. AC Global's operations in the U.S. (AC-US) sell life and annuity products and represent approximately 20% of the group's life and annuity revenues. AC-US has approximately 3,000 employees, with about 1,000 employees based in the New York City headquarters. The remaining employees are located at the company's service centers in New Jersey, Pennsylvania, and North Carolina. For an insurance company, there are four key line items on the income statement: premium revenue, investment income, benefits/claims expense, and operating expenses. Operating expenses provide the greatest opportunity for short-term improvement in earnings since the other line items are less controllable or the impacts of changes emerge over a long period of time. Investment income is primarily composed of interest and dividends on bonds and common stock investments and is not changed through operating actions. Premium revenue is composed of fees collected for providing insurance coverage and is only modestly impacted by current sales. Benefits and claims are paid to policyholders and their beneficiaries and are also difficult to impact in the short-term. The global economic downturn that began in late 2008 put intense pressure on the financial services industry. During 2009, U.S. sales of annuity products decreased by 30% while life insurance sales fell by 15%. Like the industry, AC Global has been negatively impacted by the economic downturn. AC-US premium revenue fell 8% cumulatively between 2007 and 2009. In 2010, the company's operations remained stable, but revenue was expected to be similar to 2009. AC Global's operating earnings decreased over 80% from 2007 to 2008, and AC-US suffered an operating loss in 2008. Although operating earnings recovered somewhat in 2009 (shown in Figure 1), the earnings for AC Global consolidated and AC-US are still 36% and 40%, respectively, below those in 2007. As a result, the company's stock price is down nearly 50% since the beginning of the crisis in 2008. AC-US measures operating efficiency based on the expense ratio, which is operating expenses divided by premium revenue. In 2004, AC-US went through a restructuring that reduced personnel overlap and inefficiency. Through the restructuring, AC-US reduced the workforce by 4%, reduced operating expenses by 5%, and improved the expense ratio from 12.7% in 2004 to 10.1% by 2007, 14% better than the expense ratio of 11.7% for AC Global. While operating expenses have grown modestly at 2% since 2007, the expense ratio for AC-US increased from 10.1% in 2007 to over 12.5% in 2009, worse than the 12.1% for AC Global. AC-US has underperformed AC Global in earnings and cost efficiency during 2009, which is concerning for the management of AC-US (see Figure 2). functions in the service center in India and gave George the contact information for Sanjay Delphi, the project manager for the company's India facility. George believes that in addition to outsourcing offshoring), increasing the use of electronic payments in accounts payable is another viable ways to reduce costs. George made notes on information regarding expenses relevant for the analysis, including the severance policy (see Table 7, section F). George also pulled up the organization chart to list all of the various accounting functions as well as their annual expense budgets (Table 1). He assembled information on the staff in each of the accounting functions, including their salaries, benefits, residence, and possible severance based on the years of service and prepared a summary by function (see Table 6). George meets with two of his team members, Samantha Charleston and Ryan Falkirk, to explain the project. OFFSHORING COST REDUCTION ANALYSIS PROJECT Peter George is a vice president responsible for financial planning and analysis (FP&A) at AC-US in New York. In his role, George and his team evaluate all significant projects with financial implications. George led the team that analyzed and recommended the restructuring six years ago that significantly improved the expense ratio. George met with Brian Thomas, the chief financial officer (CFO). Thomas had reviewed the first quarter preliminary revenue and earnings and told George that it is imperative for the company to find ways to reduce expenses to improve earnings. Before engaging the rest of the organization, the CFO would like the functions he manages to take a leadership position in the cost reductions-not just recommending cost- reduction actions but also providing examples to show they are effective. Thomas reviewed the accounting function first and decided he wants it to reduce expenses. Thomas asked George to evaluate potential cost-saving alternatives and provide him with a preliminary analysis within one week. Thomas then informed George that the company has recently began performing some accounting George reviews some general information on offshoring and finds that global offshoring has grown rapidly. He finds that accounting processes such as accounts payable, accounts receivable, sales ledger, general ledger, financial reporting, and bank processing are increasingly offshored.? George calls Delphi to discuss the services performed at the servicing center in India. Delphi informs George that the service center currently provides some IT support for the insurance operations in the U.K., Belgium, and France; performs some customer service functions; and also recently added a few accounting functions. Delphi emphasized that the service center is just beginning to add staff with accounting expertise and has minimal knowledge of U.S. generally accepted accounting principles (GAAP) state regulatory accounting requirements, and U.S. tax law (the U.S. Internal Revenue Code). George determines that the first step in his analysis is to identify which accounting functions would be the best candidates for offshoring and then analyze the financial and logistical feasibility of doing that. George prepares a matrix to assist him in analyzing which functions would be the most appropriate to offshore (see Table 2). His matrix takes Department. Josephine Young, of the IT Department, analyzes the requirements and informs George that they would need to improve connectivity and alter the time of the batch processing for accounts payable. She estimates there would be a one-time cost of $100,000 plus $2,500 per month for improved connectivity. The change in the batch processing time will also cause an increase in personnel costs of $2,500 per month. But there are no additional technology requirements for offshoring bank reconciliations. AUTOMATING ELECTRONIC PAYMENTS into account required skill levels, local knowledge of the U.S. Internal Revenue Code, for example), compliance risk, technological support, and the need for direct management oversight-which may be difficult due to distance and differences in time zones. He rates the functions on each of the criteria as high, medium, and low. George concludes that the functions that score low or medium on all of the criteria would be the best candidates for outsourcing. Based on the matrix, he believes that the accounts payable and bank reconciliation functions are the best candidates for initial consideration. The accounts payable function has a separate manager while the bank reconciliation function reports to the manager of general accounting. The Bank Reconciliation Department prepares 50 reconciliations per month (600 per year), and the Accounts Payable Department processes 50,000 checks per month (600,000 per year). George reviews the annual expense budgets (provided in Table 3). George sends Delphi an email and requests information on the accounts payable and bank reconciliation service functions. Delphi responds that the charges for outsourced services for accounts payable and bank reconciliation are a base monthly fee of $1,250 for each function ($15,000 per year) plus $0.65 per payment for processing accounts payable and $200 per bank reconciliation. Delphi also informs George that the U.S.-based operations would need to maintain staff to coordinate the transfer of information. Based on a similar project being undertaken by the company's U.K. operations, Delphi estimates that one staff member within the Accounting Department should be sufficient to support both accounts payable and bank reconciliations. Delphi and George discuss the necessary skills. George believes that retaining the accounts payable manager, who likely has the necessary skills, would be a good solution-and he uses that assumption for his analysis. The accounts payable manager's annual salary is $75,000. The allocated benefits charge is $18,750, but actual benefits and taxes are $19,488. George estimates that the cost for a personal computer, supplies, travel, and all other expenses (excluding postage) would total $15,500. He assumes that the salary, benefits and other expenses associated with the manager would be allocated 65% to accounts payable and 35% to bank reconciliations based upon the estimated time requirements to support each function. George does not include the allocation of rent, corporate expenses, or 50% of IT support in his cost-reduction estimate. Delphi also gives George the data transfer and connectivity specifications to discuss with the IT Charleston performs some background research on electronic payments. She finds that the use of electronic payments has increased substantially as the number of checks used in business-to-business transactions rose. The use of paper checks decreased by 5% from 2006 to 2009. The estimated savings from using electronic payment instead of paper checks ranged from 20% to 90%. Since the accounts payable function issues all of its payments as checks, Charleston believes that there may be significant savings if the company made greater use of electronic payments. Charleston contacts the company's corporate banking representative to inquire about electronic payments alternatives. She finds that the bank charges an average of $0.125 per electronic payment. The bank also provides Charleston with a contact at a company that recently adopted electronic payments (identified as Company XYZ). As a means to estimate the potential impacts, she contacts Company XYZ's treasurer to discuss how it impacted their staffing needs and costs and is informed that Company XYZ averaged 2 minutes in labor per manual check and only 1.5 minutes for each electronic payment. For recurring payments, Company XYZ experienced an 80% time savings annually. To support her analysis, Charleston requests and receives a report showing the number of the company's checks that are recurring to vendors as well as those to employees and business partners, which are good candidates for electronic payments (see Table 4). Based on her preliminary analysis, Charleston estimates that the company could process up to 50% of its current payments electronically. Using the results for Company XYZ as a proxy, she estimates that electronic payments would reduce processing time by 25% for each electronic payment. Since recurring payments require minimal work after initial set-up, the potential estimated time savings is 80%. Since 16% of payments are recurring, labor savings would be possible. Charleston estimates that electronic payment processing would reduce staff, with associated reductions in salaries and benefits as well as other associated costs. To estimate the impact on staff, she uses 10 employees processing 600,000 checks annually and assumes that 50% of the payments could become electronic. To calculate the potential savings in salaries and benefits, she assumes that the staff reductions would involve less-experienced staff and represent 15% of total salaries and benefits for accounts payable. She estimates also that there would be savings in personal computer (PC) costs, IT support, and other costs of $1,775 per employee. Additionally, there would be a reduction in postage costs in direct proportion to the reduction of the number of checks. These savings would be partially offset by an additional cost of $0.125 for each electronic payment that replaces a check. Further, she uses the information from Table 6 to estimate that severance costs would represent 15% of the maximum eligible severance for accounts payable. INTERACTION OF ALTERNATIVES If the company only outsources bank reconciliations, the team has assumed that the bank reconciliation department will need to retain the most experienced employee to support the process. The most experienced employee in the department has eight years of service, a salary of $48,000, health insurance costs of $10,000, 401(k) contributions at 5%, and payroll taxes of 7.65%. In addition to the savings in salaries and benefits for the positions eliminated in bank reconciliations, it is also estimated that there would be a savings of $8,000 in total for expenses other than salaries and benefits. The one time initial costs would consist of severance costs for the positions eliminated. 2. Considering the alternative of Electronic Processing of half checks AND offshoring bank reconciliation only: a. Using the information that Charleston gathered on electronic payment processing of 50% of the accounts payable checks, determine the number of potential accounting payable staff reduction. b. Based on the potential staff reduction, determine the annual cost savings from electronic processing of 50% of the accounts payable checks AND offshoring bank reconciliation. c. If AC-US outsources bank reconciliations and changes to electronic payment of 50% of the accounts payable checks, what would be the maximum combined savings over the next three years, including the one-time severance costs? ENDNOTES "Annual Report on the Insurance Industry, Federal Insurance Office of the U.S. Treasury, June 2013. 2Nora Palugod and Paul A. Palugod, "Global Trends in Offshoring and Outsourcing," Internal Journal of Business and Social Science, September 2011. 3"The 2010 Federal Reserve Payments Study: Noncash Payment Trends in the United States: 2006-2009,"updated April 5, 2011, Federal Reserve System. *Matthew Heller, "Electronic Payments 10 Times Cheaper Than Checks, CFO.com, October 12, 2015. Estimated staff reduction based on 600,000 checks supported by 10 full-time employees (FTES). Estimate 300,000 checks, or 50%, with similar level of FTE support per check. The necessary FTEs to support electronic payments (34% of payments) assume 25% time savings for electronic payments. The remaining 16% of payments are recurring electronic payments and estimate an 80% time savings. Figure 1: Operating Earnings ($ in millions) 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 AC Global - AC-US (1,000) 2004 2005 2006 2007 2008 2009 Figure 2: Operating Expense Ratio for AC Global vs. AC-US 13.0% AC Global - AC-US 12.0% 11.0% 10.0% 2004 2005 2006 2007 2008 2009 Table 1: Accounting Department Expense Budget Summary Number of Employees Annual Salaries $802,000 8 12 812,000 2 2 7 250,000 285,000 525,000 575,000 525.000 7 6 Function Federal tax preparation State tax preparation Tax management Controller SEC reporting U.S. GAAP reporting Regulatory financial reporting Management reporting Cost accounting General accounting Accounts payable Bank reconciliations Planning and budgeting Financial analysis Totals Annual Benefits Load $200,500 203,000 62,500 71,250 131,250 143,750 131,250 113,750 96,250 157,000 117,500 53,750 81,250 171,250 $1,734,250 All Other $176,500 170,000 72,500 68,750 158,750 126,250 118,750 106,250 98,750 100,000 393,750 61,750 88,750 108,750 $1,849,500 Total Budgeted Expenses $1,179,000 1,185,000 385,000 425,000 815,000 845,000 775,000 675,000 580,000 885,000 981,250 330,500 495,000 965,000 $10,520,750 6 455,000 385,000 6 10 10 5 628,000 470,000 215,000 325,000 685,000 $6,937,000 4 8 93 Table 2: Matrix of Potential Accounting Functions for Outsourcing Skill Level Required Local knowledge Required Mgmt. Support / Interaction Technology Support Required Compliance Risk Function Tax Department Federal tax preparation Medium High Low Low Medium Low Low High High High High Medium High High Low High Medium Medium Medium Medium High High Medium Medium High High Medium High High High Medium Medium Medium Low State tax preparation Tax planning Controller's Department SEC reporting U.S. GAAP reporting Regulatory reporting Management reporting Cost accounting General accounting Accounts payable Bank reconciliations Financial Planning and Analysis Planning and budgeting Financial analysis High Medium Medium Medium Medium Low Medium Medium Medium Low Medium Medium Low Low Low Low Medium Low Low Low Low Medium Medium Low Medium Medium High High Medium Low Low Table 3: 2010 Detailed Expense Budget for Accounts Payable and Bank Reconciliations Accounts Bank Expense Payable Reconciliations Salaries $470,000 $215,000 Benefits load 117,500 53,750 Rent and related 64,000 42,000 Supplies 16,750 1,750 PCS 12,000 6,000 IT support 11,500 6,000 Postage 270,000 Travel and entertainment 11,500 3,000 Corporate expenses 8,000 3,000 Total $981,250 $330,500 Table 4: Summary of Checks Processed per Month Business Partners/ Employees Recurring (probably electronic) All Others Total Checks (monthly) 8,000 17,000 25,000 50,000 Percentage 16% 34% 50% 100% Table 6: Summary Employee Information for Severance Calculations Actual Costs Number of weeks of Eligible Total Annual Employees Severance Salaries Benefits Load Health 401(k) Payroll Taxes Tax Department: Department head and assistant 2. 32 $250,000 $62,500 $ $17,200 $12,500 $19,125 Federal Tax N.J. residents 4 76 445,000 111,250 32,200 22,250 34,043 4 66 27,200 17,850 Non-N.J. residents -. Total 357,000 802,000 89,250 200,500 27,311 61,354 8 142 59,400 40, 100 State Taxes N.J. residents 9 140 156,750 76,600 20,000 Non-N.J. residents 627,000 185,000 812,000 47,966 14,153 3 52 192 46,250 31,350 9,250 40,600 Total 12 203,000 96,600 62,119 Controller's Department: 2 28 285,000 71,250 15,000 14,250 21,803 Department head and assistant SEC Reporting N.J. residents Non-N.J. residents - Total 5 96 94,750 34,400 18,950 28,994 379,000 146,000 2 36 36,500 17,200 7,300 11,169 7 132 525,000 131,250 51,600 26,250 40,163 U.S. GAAP Reporting N.J. residents 5 74 413,500 103,375 20,675 31,633 2 30 161,500 40,375 37,200 12,200 49,400 Non-N.J. residents . Total 8,075 12,355 43,988 7 104 575,000 143,750 28,750 Regulatory Reporting N.J. residents 4 52 87,750 27,200 17,550 26,852 351,000 174,000 2 30 17,200 13,311 Non-N.J. residents . Total 43,500 131,250 8,700 26,250 6 82 525,000 44,400 40,163 Management Reporting N.J. residents 4 52 75,750 27,200 23,180 2 30 303,000 152,000 455,000 38,000 Non-N.J. residents Total 17,200 15,150 7,600 22,750 11,628 34,808 6 82 113,750 44,400 Cost Accounting N.J. residents Non-N.J. residents 5 70 322,000 80,500 34,400 16,100 24,633 1 1 12 63,000 15,750 10,000 4,820 3,150 19,250 Total 6 82 385,000 96,250 44,400 29,453 General Accounting N.J. residents 9 128 559,000 139,750 69,400 27,950 42,764 Non-N.J. residents 1 18 69,000 7,200 3,450 5,279 17,250 157,000 Total 10 146 628,000 76,600 31,400 48,042 Table 6: Summary Employee Information for Severance Calculations (continued) Actual Costs Number of Weeks of Eligible Total Annual Employees Severance Salaries Benefits Load Health 401(k) Payroll Taxes Accounts Payable 7 106 83,250 46,600 16,650 N.J. residents Non-N.J. residents . Total 3 333,000 137,000 470,000 60 166 34,250 25,000 71,600 6,850 23,500 25,475 10,481 35,956 10 117,500 Bank Reconciliation N.J. residents 3 42 34,250 30,000 6,850 10,481 24 137,000 78,000 215,000 19,500 12,200 3,900 5,967 66 53,750 42,200 10,750 16,448 Non-N.J. residents . 2 Totale 5 Financial Reporting & Analysis Department: Budgeting N.J. residents 2 177,000 44,250 12,200 28 26 8,850 7,400 2 2 148,000 37,000 15,000 Non-N.J. residents . Total 13,541 11,322 24,863 4 4 54 325,000 81,250 27,200 16,250 Financial Analysis N.J. residents 6 72 526,000 131,500 39,400 26,300 40,239 Non-N.J. residents -. 2 30 159,000 39,750 17,200 7,950 12,164 Total 8 102 685,000 171,250 56,600 34,250 52,403 "The severance and continuing benefits for the accounts payable manager total $29,073, and the severance and continuing benefits for the most experienced staff member in bank reconciliations is $19,714. Note: When calculating severance using the total salaries, you must first find the average weekly salary (salariesumber of employees/52 weeks) and multiply by the number of weeks of severance. Follow a similar process for health benefits. For 401(k) and payroll taxes, you may either follow the same process or apply the rate. Table 7: Supplemental Information on Relevant Expenses A. The benefits load of 25% of salaries is designed to represent the costs to provide health, dental and vision insurance, the employer contribution to the 401(k) plan, and employer payroll taxes. 1. The company's share of health benefits (including dental and vision insurance) is $10,000 per year for family (F), $7,200 for parent/children or employee/ spouse (P/C), and $5,000 for single (5) employees. 2. The employer portion of payroll taxes is 7.65% of salaries. 3. The company contribution to the 401(k) plan is 5% of salaries. B. The company has eight years remaining on its lease and is unlikely to be able to reduce space unless it can create 10,000 square feet (one floor) of available space for sublease. C. The corporate expense allocation is for the company cafeteria and an on-site gym; the company's costs are unlikely to fall if staff in the Accounting Department is reduced. D. PCs are leased, and the company can return them with no penalty; 50% of the IT support costs are variable and can be saved when the PCs are eliminated. E. The postage costs in accounts payable would not change by offshoring or relocation as the checks would be printed and mailed from the company's office in the U.S. F. The company severance policy calls for two weeks of salary for each year of service with minimum payment of 12 weeks. Health benefits and retirement plan contributions continue to be provided during the severance period. Payroll taxes would also apply. IMA EDUCATIONAL CASE JOURNAL 10 VOL. 9, NO. 3, ART. 3, SEPTEMBER 2016