Question

Introduction You are a financial analyst for the firm - Seneca and Finch Inc.(S&F) The firm offers forensic accounting, litigation support, and business valuation services.

Introduction

You are a financial analyst for the firm - Seneca and Finch Inc.(S&F) The firm offers forensic accounting, litigation support, and business valuation services. As a FEA graduate, you have been hired to assist the managing director on a trip to Halifax Nova Scotia to assist in the valuation of the Halifax Mariners Hockey Club Limited (HMHCL).

As set out at the end, you are to provide preliminary valuation calculations (Excel Spreadsheet) as at May 31, 2012.

Background

Halifax is a city of 500,000 and is the largest urban area in Canada east of Quebec City.

The HMHCL is a team in the Eastern Canadian Hockey League. It plays 30 games in Halifax and 30 games in other cities. A semi-professional league is a training ground for the National Hockey League.

Please note that the HMHCL had 3, 4, and 5 additional home games with the playoffs in 2010, 2011 and 2012 respectively. The number of games depends on many factors but for this case does not adjust the revenues; assume the team will continue to be in the playoffs.

The team is 81% owned by John Dartmouth, a local businessperson. 10.0% of the team is owned by Louis Lafleur, who previously owned the Quebec City Flyers in the Eastern Canadian Hockey League. Mr. Tom Tango of Toronto owns 9.0% of the team.

The team rents the 10,000 seat Halifax Arena for its games and uses that facility for its games practices as well.

? The HMHCL receives its revenues from:

? Ticket sales ? Royalties on refreshments and souvenirs ? Television broadcast (media) rights ? Compensation for player contracts acquired from HMHCL

The revenue components include:

? Ticket sales are for subscriber and single admission tickets ? Royalties are 10% of the net revenues on refreshment and souvenir sales ? Television broadcast rights are from the Athletes Sports Network ? Compensation for player contracts is what is paid to the team (mainly by NHL professional teams) when HMHCL developing players are transferred to the NHL teams. Sometimes, HMHCL pays money to other teams to acquire players they want.

Signing fees and other up-front costs for players are considered intangible assets and are written off at 25% per year.

See the attached financial statements for the breakdown of revenues for the period 2010-2012. The fiscal year for HMHCL ends on May 31 of each year, just after the end of the hockey season.

The issue

Relations between the shareholders are tense, as Mr. Dartmouth controlled the team and did not want either Mr. Lafleur or Mr. Tango having any input into the decisions about the team, including pricing of tickets, souvenirs, and broadcast rights.

He agreed to buy out their minority interests, based on an independent valuation. Mr. Dartmouth hired Seneca and Finch to do an independent valuation to set the price he would pay and for the offer to Mr. Lafleur and Mr. Tango.

There were several issues that had to be addressed for the valuation, including:

- Ticket booking. All HMHCL tickets (season tickets or individual games) had to be booked through Mr. Dartmouth's booking agency, Hockey Unlimited, at a $0.50 per ticket charge to the HMHCL. Mr. Lafleur and Mr. Tango noted that other teams in the league were charged $0.30 per ticket for ticket booking. With a total of 240.000 paid admissions per regular season, excluding playoffs, the estimated lost revenue to HMHCL is estimated as $48,000 (240,000 tickets x $ 0.20 per ticket).

- Television broadcast rights. The HMHCL had entered into an agreement with Athletic Network to show the games from 2008-2013. The revenue to the HMHCL was $500,000 per hockey season. However, the television audiences were very large and other networks had approached the HMHCL about the period the 2014 fiscal years onward. As a result, the HMHCL signed the Athletes Network a new contract of $1,000,000 revenue per year starting in 2014 fiscal year until 2018.

This new contract was not disclosed to Seneca & Finch by Mr. Dartmouth. He told S&F to assume the same broadcast rights for 2014 to 2018 fiscal years.The information on the new contract came from finding a copy of the new 2014-2018 contract in the back of the file on ticket booking fees; it had been misfiled and was not intended for the valuation team to see. You subsequently contact the Athletic Network and determine that the revenue will increase to $1,000,000 per year in the year ending May 31, 2014.

You must address the question of whether you should provide the valuation based on the information officially provided by Mr. Dartmouth or on all the additional information discovered.

Lease for the arena. Mr. Dartmouth's own company, Halifax Arenas Limited (HAL), rented the arena to the HMHCL.The rent was $33,000 per game for 10,000 seats. There was a $50,000 annual charge for 2,000 square feet of office space for the team and the ticket office on the ground floor. Playoff games were at the same $33,000 rate. The average rental for the league was $22,000 per game for an average of 11,000 seats. Thus, the HMHCL was charging 50% more than the league average and the per-seat per-game rental cost was $3.30 per seat vs. $2.00 per seat with the league average. An outside arena specialist hired by S&F estimated that the fair market rental for the Halifax Arena would be $28,000 per game for 30 games, or $840,000 per season, being $150,000 less than beingpaid by HMHCL to Mr. Dartmouth's Halifax Arena Limited. The difference is $5,000 per game.

- Ice refinishing machine ("Zamboni"). There was a problem with the ice refinishing capacity of Halifax Arena Limited (HAL).The Halifax Arena had an old Zamboni ice-refinishing machine that was not reliable for resurfacing the ice between periods. Mr. Dartmouth required the HMHCL to lease its own Zamboni machine. The machine is a new Zamboni machine on a five-year operating term for HMHCL games for $30,000 per year. It was used by the HMHCL for 200 hours per year to prepare ice for practices and games.[1] However, the HMHCL Zamboni machine was also used for 200 hours in each of fiscal 2012 and 2011 by Halifax Arenas for its events. It was being used by HAL to clean the ice for figure skating shows, children's hockey, and when the arena was open for pleasure skating. The Halifax Arena's own Zamboni machine was not reliable and damaged the ice. No compensation was being paid to the HMHCL for this HAL use of the HMHCL ice-cleaning Zamboni. You are advised that in an arm's length situation, that HAL would normally reimburse the HMHCL, as its tenant, for Hal's 50% use of the annual operating use of the HMHCL's Zamboni machine.

Required

The managing director has asked you to prepare and provide excel calculations to support the following:

- Normalized earnings. Normalizing earnings by adjusting for discretionary or non-arm's length items (take an average of the three years to determine normalized earnings);

- Maintainable earnings. Maintainable earnings are determined by further adjusting the normalized earnings for significant foreseeable changes in a company's business, either changes that have occurred or will occur;

- Price earnings multiple. Select a Price Earnings Multiple that reflects the industry with an appropriate, say 15% adjustment downward for a private company and a further discount of 10% for the shares of Mr. Lafleur and Mr. Tango as they are minority shareholders.

Please assume that your research shows that other sports teams that are listed on stock exchanges sell for 20 x earnings

.

- Estimated value. Determine value on an earnings basis of the company by multiplying the normalized maintainable earnings by the selected price earnings multiple.

- Goodwill. Determine goodwill of the HMHCL by taking the Estimated Value (4) and subtracting the Net book Value of the company (being assets - liabilities).

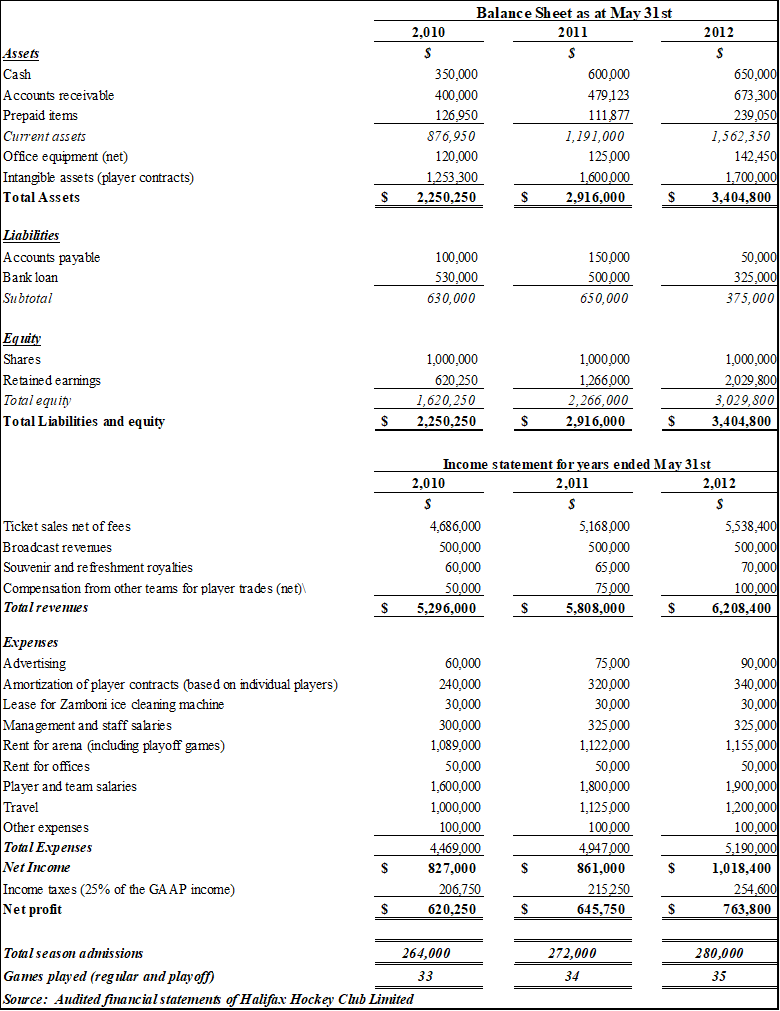

Assets Cash Accounts receivable Prepaid items Current assets Office equipment (net) Intangible assets (player contracts) Total Assets Liabilities Accounts payable Bank loan Subtotal Balance Sheet as at May 31st 2,010 2011 2012 $ S 350,000 600,000 650,000 400,000 479,123 673,300 126,950 111,877 239,050 876,950 1,191,000 1,562,350 120,000 125,000 142,450 1,253,300 1,600,000 1,700,000 $ 2,250,250 $ 2,916,000 $ 3,404,800 100,000 150,000 50,000 530,000 500,000 325,000 630,000 650,000 375,000 Equity Shares 1,000,000 1,000,000 1,000,000 Retained earnings 620,250 1,266,000 2,029,800 Total equity 1,620,250 Total Liabilities and equity $ 2,250,250 $ 2,266,000 2,916,000 3,029,800 $ 3,404,800 Income statement for years ended May 31st 2,010 2,011 S Ticket sales net of fees 4,686,000 5,168,000 Broadcast revenues 500,000 500,000 2,012 5,538,400 500,000 Souvenir and refreshment royalties 60,000 65,000 70,000 Compensation from other teams for player trades (net)\ 50,000 75,000 100,000 Total revenues $ 5,296,000 $ 5,808,000 $ 6,208,400 Expenses Advertising 60,000 75,000 90,000 Amortization of player contracts (based on individual players) 240,000 320,000 340,000 Lease for Zamboni ice cleaning machine 30,000 30,000 30,000 Management and staff salaries 300,000 325,000 325,000 Rent for arena (including playoff games) 1,089,000 1,122,000 1,155,000 Rent for offices Player and team salaries Travel 50,000 50,000 50,000 1,600,000 1,800,000 1,900,000 1,000,000 1,125,000 1,200,000 Other expenses 100,000 100,000 100,000 Total Expenses 4,469,000 4,947,000 5,190,000 Net Income $ 827,000 861,000 $ 1,018,400 Income taxes (25% of the GAAP income) Net profit 206,750 215250 254,600 $ 620,250 $ 645,750 $ 763,800 Total season admissions 264,000 Games played (regular and play off) 33 272,000 34 280,000 35 Source: Audited financial statements of Halifax Hockey Club Limited

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Practical financial management

Authors: William r. Lasher

5th Edition

0324422636, 978-0324422634