Answered step by step

Verified Expert Solution

Question

1 Approved Answer

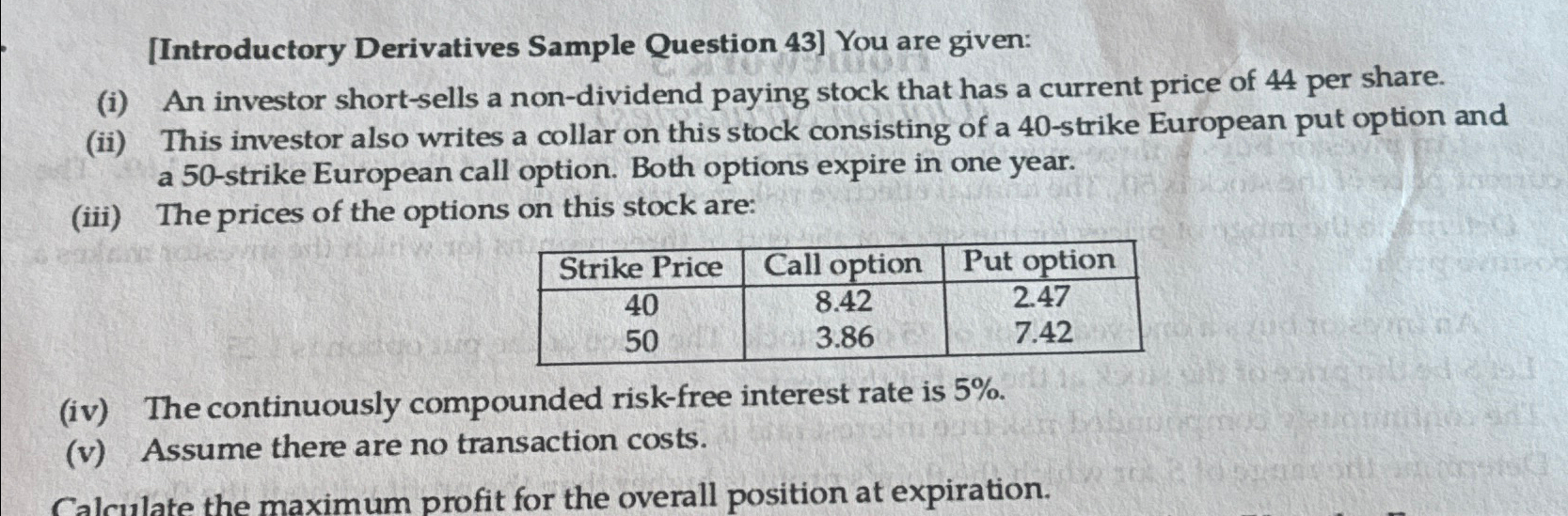

[ Introductory Derivatives Sample Question 4 3 ] You are given: ( i ) An investor short - sells a non - dividend paying stock

Introductory Derivatives Sample Question You are given:

i An investor shortsells a nondividend paying stock that has a current price of per share.

ii This investor also writes a collar on this stock consisting of a strike European put option and a strike European call option. Both options expire in one year.

iii The prices of the options on this stock are:

tableStrike Price,Call option,Put option

iv The continuously compounded riskfree interest rate is

v Assume there are no transaction costs.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Routledge Handbook Of FinTech

Authors: K. Thomas Liaw

1st Edition

0367263599, 978-0367263591