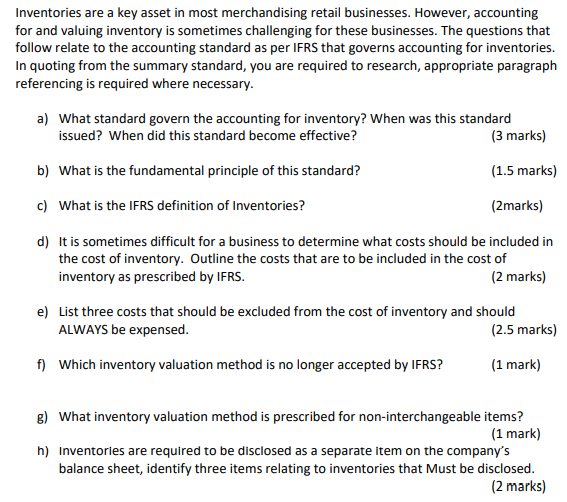

Inventories are a key asset in most merchandising retail businesses. However, accounting for and valuing inventory is sometimes challenging for these businesses. The questions that follow relate to the accounting standard as per IFRS that governs accounting for inventories. In quoting from the summary standard, you are required to research, appropriate paragraph referencing is required where necessary. a) What standard govern the accounting for inventory? When was this standard issued? When did this standard become effective? (3 marks) b) What is the fundamental principle of this standard? (1.5 marks) c) What is the IFRS definition of Inventories? (2marks) d) It is sometimes difficult for a business to determine what costs should be included in the cost of inventory. Outline the costs that are to be included in the cost of inventory as prescribed by IFRS. (2 marks) e) List three costs that should be excluded from the cost of inventory and should ALWAYS be expensed. (2.5 marks) f) Which inventory valuation method is no longer accepted by IFRS? (1 mark) g) What inventory valuation method is prescribed for non-interchangeable items? (1 mark) h) Inventories are required to be disclosed as a separate item on the company's balance sheet, identify three items relating to inventories that Must be disclosed. (2 marks) Inventories are a key asset in most merchandising retail businesses. However, accounting for and valuing inventory is sometimes challenging for these businesses. The questions that follow relate to the accounting standard as per IFRS that governs accounting for inventories. In quoting from the summary standard, you are required to research, appropriate paragraph referencing is required where necessary. a) What standard govern the accounting for inventory? When was this standard issued? When did this standard become effective? (3 marks) b) What is the fundamental principle of this standard? (1.5 marks) c) What is the IFRS definition of Inventories? (2marks) d) It is sometimes difficult for a business to determine what costs should be included in the cost of inventory. Outline the costs that are to be included in the cost of inventory as prescribed by IFRS. (2 marks) e) List three costs that should be excluded from the cost of inventory and should ALWAYS be expensed. (2.5 marks) f) Which inventory valuation method is no longer accepted by IFRS? (1 mark) g) What inventory valuation method is prescribed for non-interchangeable items? (1 mark) h) Inventories are required to be disclosed as a separate item on the company's balance sheet, identify three items relating to inventories that Must be disclosed. (2 marks)