Answered step by step

Verified Expert Solution

Question

1 Approved Answer

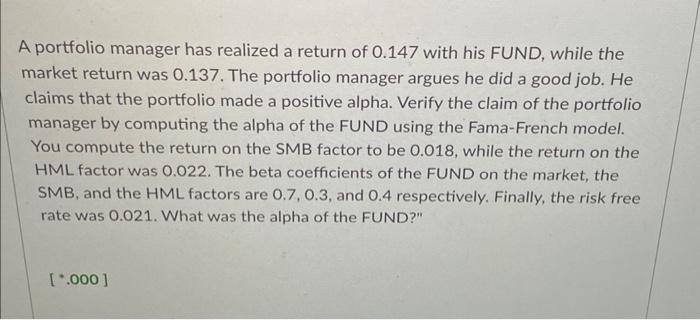

investments A portfolio manager has realized a return of 0.147 with his FUND, while the market return was 0.137. The portfolio manager argues he did

investments

A portfolio manager has realized a return of 0.147 with his FUND, while the market return was 0.137. The portfolio manager argues he did a good job. He claims that the portfolio made a positive alpha. Verify the claim of the portfolio manager by computing the alpha of the FUND using the Fama-French model. You compute the return on the SMB factor to be 0.018, while the return on the HML factor was 0.022. The beta coefficients of the FUND on the market, the SMB, and the HML factors are 0.7,0.3, and 0.4 respectively. Finally, the risk free rate was 0.021. What was the alpha of the FUND Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Basics Of Public Budgeting And Financial Management

Authors: Charles E. Menifield

4th Edition

0761872116, 978-0761872115