Answered step by step

Verified Expert Solution

Question

1 Approved Answer

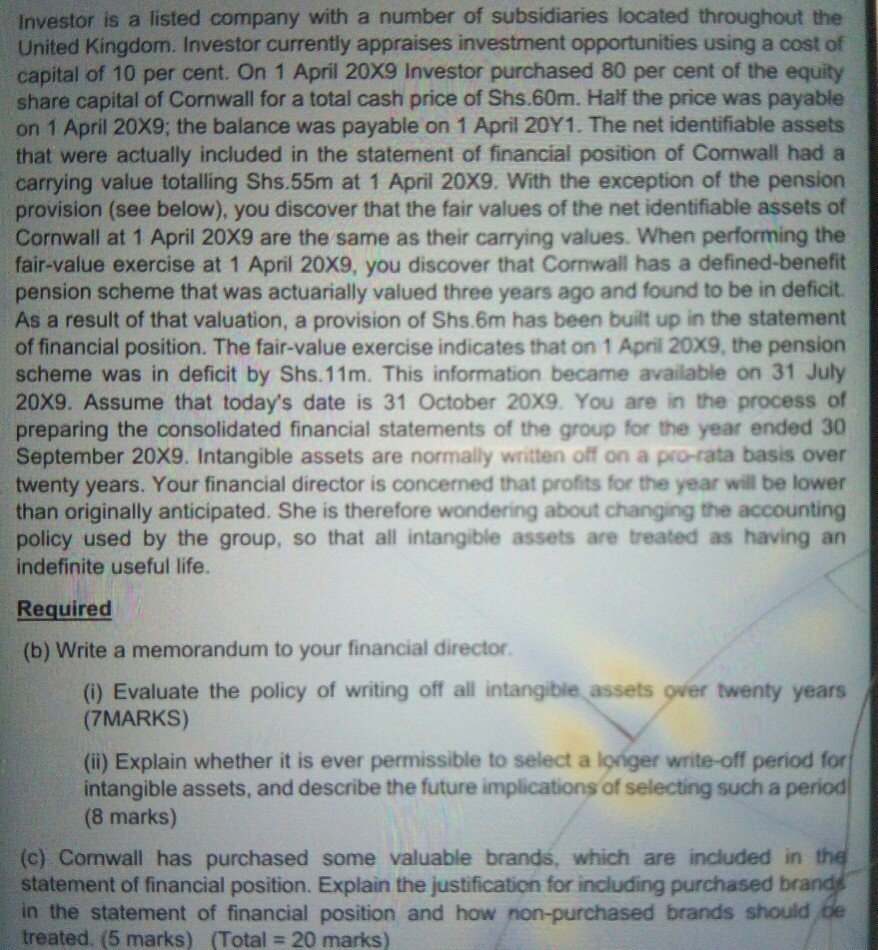

Investor is a listed company with a number of subsidiaries located throughout the United Kingdom. Investor currently appraises investment opportunities using a cost of capital

Investor is a listed company with a number of subsidiaries located throughout the United Kingdom. Investor currently appraises investment opportunities using a cost of capital of 10 per cent. On 1 April 20X9 Investor purchased 80 per cent of the equity share capital of Cornwall for a total cash price of Shs.60m. Half the price was payable on 1 April 20X9; the balance was payable on 1 April 20Y1. The net identifiable assets that were actually included in the statement of financial position of Comwall had a carrying value totalling Shs.55m at 1 April 20X9. With the exception of the pension provision (see below), you discover that the fair values of the net identifiable assets of Cornwall at 1 April 20x9 are the same as their carrying values. When performing the fair-value exercise at 1 April 20X9, you discover that Cornwall has a defined-benefit pension scheme that was actuarially valued three years ago and found to be in deficit. As a result of that valuation, a provision of Shs.6m has been built up in the statement of financial position. The fair-value exercise indicates that on 1 April 20X9, the pension scheme was in deficit by Shs. 11m. This information became available on 31 July 20X9. Assume that today's date is 31 October 20X9. You are in the process of preparing the consolidated financial statements of the group for the year ended 30 September 20X9. Intangible assets are normally written off on a pro-rata basis over twenty years. Your financial director is concerned that profits for the year will be lower than originally anticipated. She is therefore wondering about changing the accounting policy used by the group, so that all intangible assets are treated as having an indefinite useful life. Required (b) Write a memorandum to your financial director (1) Evaluate the policy of writing off all intangible assets over twenty years (7MARKS) (ii) Explain whether it is ever permissible to select a longer write-off period for intangible assets, and describe the future implications of selecting such a period (8 marks) (c) Cornwall has purchased some valuable brands, which are included in the statement of financial position. Explain the justification for including purchased brands in the statement of financial position and how non-purchased brands should de treated. (5 marks) (Total = 20 marks) Investor is a listed company with a number of subsidiaries located throughout the United Kingdom. Investor currently appraises investment opportunities using a cost of capital of 10 per cent. On 1 April 20X9 Investor purchased 80 per cent of the equity share capital of Cornwall for a total cash price of Shs.60m. Half the price was payable on 1 April 20X9; the balance was payable on 1 April 20Y1. The net identifiable assets that were actually included in the statement of financial position of Comwall had a carrying value totalling Shs.55m at 1 April 20X9. With the exception of the pension provision (see below), you discover that the fair values of the net identifiable assets of Cornwall at 1 April 20x9 are the same as their carrying values. When performing the fair-value exercise at 1 April 20X9, you discover that Cornwall has a defined-benefit pension scheme that was actuarially valued three years ago and found to be in deficit. As a result of that valuation, a provision of Shs.6m has been built up in the statement of financial position. The fair-value exercise indicates that on 1 April 20X9, the pension scheme was in deficit by Shs. 11m. This information became available on 31 July 20X9. Assume that today's date is 31 October 20X9. You are in the process of preparing the consolidated financial statements of the group for the year ended 30 September 20X9. Intangible assets are normally written off on a pro-rata basis over twenty years. Your financial director is concerned that profits for the year will be lower than originally anticipated. She is therefore wondering about changing the accounting policy used by the group, so that all intangible assets are treated as having an indefinite useful life. Required (b) Write a memorandum to your financial director (1) Evaluate the policy of writing off all intangible assets over twenty years (7MARKS) (ii) Explain whether it is ever permissible to select a longer write-off period for intangible assets, and describe the future implications of selecting such a period (8 marks) (c) Cornwall has purchased some valuable brands, which are included in the statement of financial position. Explain the justification for including purchased brands in the statement of financial position and how non-purchased brands should de treated. (5 marks) (Total = 20 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Of Capital In Managerial Finance

Authors: Dennis Schlegel

2015th Edition

3319151347, 978-3319151342