Answered step by step

Verified Expert Solution

Question

1 Approved Answer

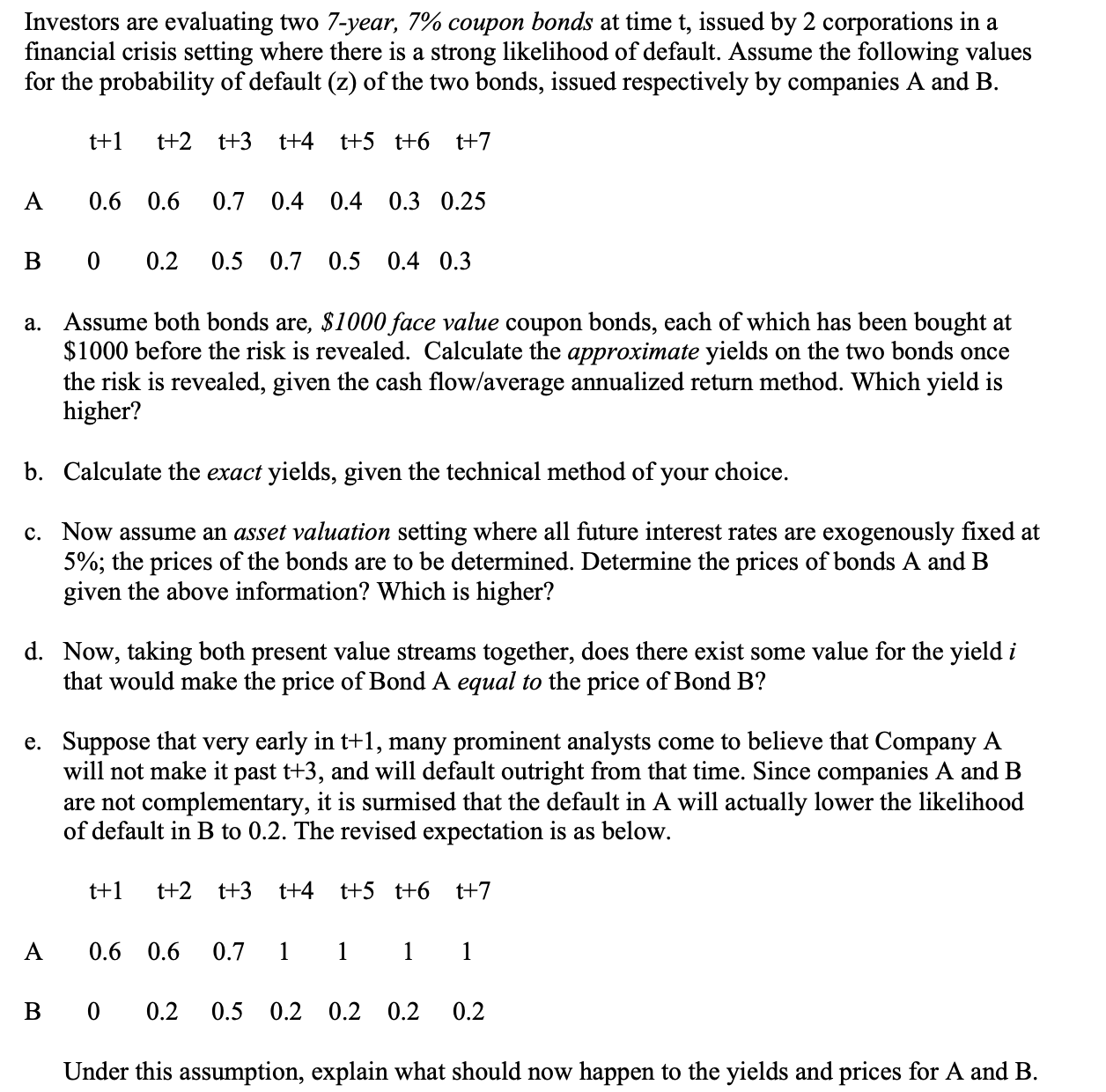

Investors are evaluating two 7 - year, 7 % coupon bonds at time t , issued by 2 corporations in a financial crisis setting where

Investors are evaluating two year, coupon bonds at time issued by corporations in a

financial crisis setting where there is a strong likelihood of default. Assume the following values

for the probability of default of the two bonds, issued respectively by companies A and B

a Assume both bonds are, $ face value coupon bonds, each of which has been bought at

$ before the risk is revealed. Calculate the approximate yields on the two bonds once

the risk is revealed, given the cash flowaverage annualized return method. Which yield is

higher?

b Calculate the exact yields, given the technical method of your choice.

c Now assume an asset valuation setting where all future interest rates are exogenously fixed at

; the prices of the bonds are to be determined. Determine the prices of bonds A and B

given the above information? Which is higher?

d Now, taking both present value streams together, does there exist some value for the yield

that would make the price of Bond A equal to the price of Bond B

e Suppose that very early in many prominent analysts come to believe that Company

will not make it past and will default outright from that time. Since companies A and

are not complementary, it is surmised that the default in A will actually lower the likelihood

of default in B to The revised expectation is as below.

Under this assumption, explain what should now happen to the yields and prices for A and B

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: J . chris leach, Ronald w. melicher

4th edition

538478152, 978-0538478151