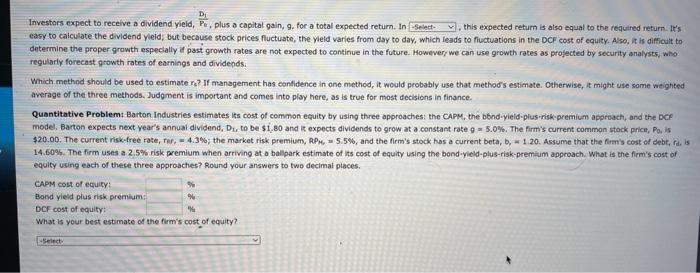

Investors expect to receive a dividend yield, PeD1, plus a capital gain, 9 , for a total expected return. In , this expected return is also equal to the required refurn. It's easy to calculate the dividend yield; but because stock prices fluctuate, the yield varies from day to day, which leads to fluctuations in the DCF cost of equity. Also, it is difficult to determine the proper growth especlally if past growth rates are not expected to continue in the future. Howevery we can use growth rates as projected by security analysts, who regularly forecast growth rates of earnings and dividepds: Which method should be used to estimate rs ? If management has conflidence in one method, it would probably use that method's estimate. Otherwise, it might use same weighted average of the three methods. Judgment is important and comes into play here, as is true for most decisions in finance. Quantitative Problem: Barton Industries estimates its cost of common equity by using three approaches: the CAPM, the bbnd-yield-plus-risk-premium approach, and the DCF model. Barton expects next vear's annual dividend, D4, to be $1,80 and it expects dividends to grow at a constant rate 9=5.0%, The firm's current common stock price, P. is $20.00. The current risk-free rate, rer, =4.3%; the market risk premium, APM=5.5%, and the firm's stock has a current beta, b,=1.20. Assume that the firm's cost of debt, ri, is 14.50%. The firm uses a 2.5% risk premium when arriving at a ballpark estimate of its cost of equity using the bond-yield-plus-risk-premium approach. What is the firm's cost of equity using each of these three approaches? Round your answers to two decimal places. CAPM cost of equity: Bond yield plus risk premium: DCF cost of equity: 5 4 44 What is your best estimate of the firm's cost of equity? Investors expect to receive a dividend yield, PeD1, plus a capital gain, 9 , for a total expected return. In , this expected return is also equal to the required refurn. It's easy to calculate the dividend yield; but because stock prices fluctuate, the yield varies from day to day, which leads to fluctuations in the DCF cost of equity. Also, it is difficult to determine the proper growth especlally if past growth rates are not expected to continue in the future. Howevery we can use growth rates as projected by security analysts, who regularly forecast growth rates of earnings and dividepds: Which method should be used to estimate rs ? If management has conflidence in one method, it would probably use that method's estimate. Otherwise, it might use same weighted average of the three methods. Judgment is important and comes into play here, as is true for most decisions in finance. Quantitative Problem: Barton Industries estimates its cost of common equity by using three approaches: the CAPM, the bbnd-yield-plus-risk-premium approach, and the DCF model. Barton expects next vear's annual dividend, D4, to be $1,80 and it expects dividends to grow at a constant rate 9=5.0%, The firm's current common stock price, P. is $20.00. The current risk-free rate, rer, =4.3%; the market risk premium, APM=5.5%, and the firm's stock has a current beta, b,=1.20. Assume that the firm's cost of debt, ri, is 14.50%. The firm uses a 2.5% risk premium when arriving at a ballpark estimate of its cost of equity using the bond-yield-plus-risk-premium approach. What is the firm's cost of equity using each of these three approaches? Round your answers to two decimal places. CAPM cost of equity: Bond yield plus risk premium: DCF cost of equity: 5 4 44 What is your best estimate of the firm's cost of equity