Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Is the price of this callable bond lower or higher than an otherwise comparable non-callable bond? And why? (10 MARKS) 1. The two-year binomial interest-rate

Is the price of this callable bond lower or higher than an otherwise comparable non-callable bond? And why? (10 MARKS)

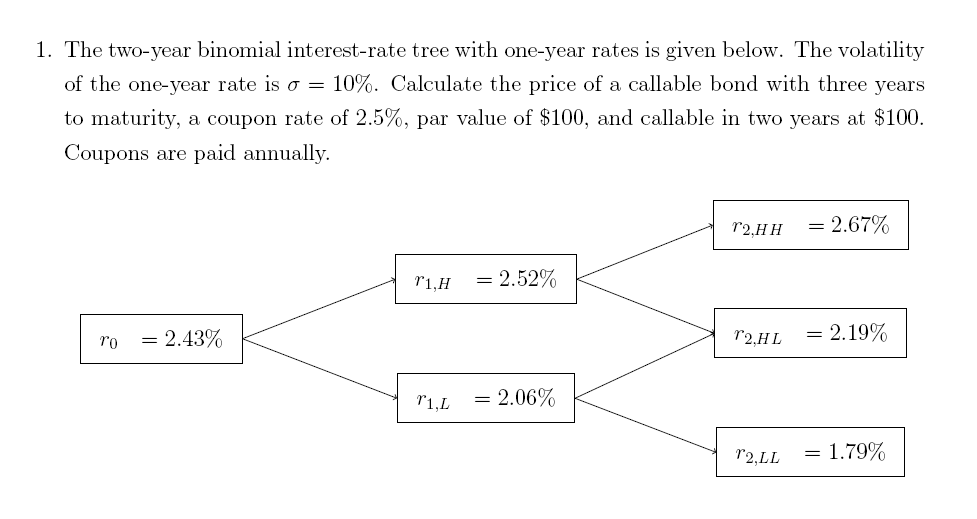

1. The two-year binomial interest-rate tree with one-year rates is given below. The volatility of the one-year rate is o = 10%. Calculate the price of a callable bond with three years to maturity, a coupon rate of 2.5%, par value of $100, and callable in two years at $100. Coupons are paid annually. r2.HH 2.67% r1.H = 2.52% = 2.43% ro 2.HL = 2.19% 11,1 = 2.06% 12,LL = 1.79%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Amazon Mechanical Turk Start To Make Money Online

Authors: Ines Mechler

1st Edition

1542974267, 978-1542974264