Question

(2) Isaac, CPA, is auditing Fun Fitness Inc., a calendar-year corporation. He is performing analytical procedures relative to the sales account for Year 2. He

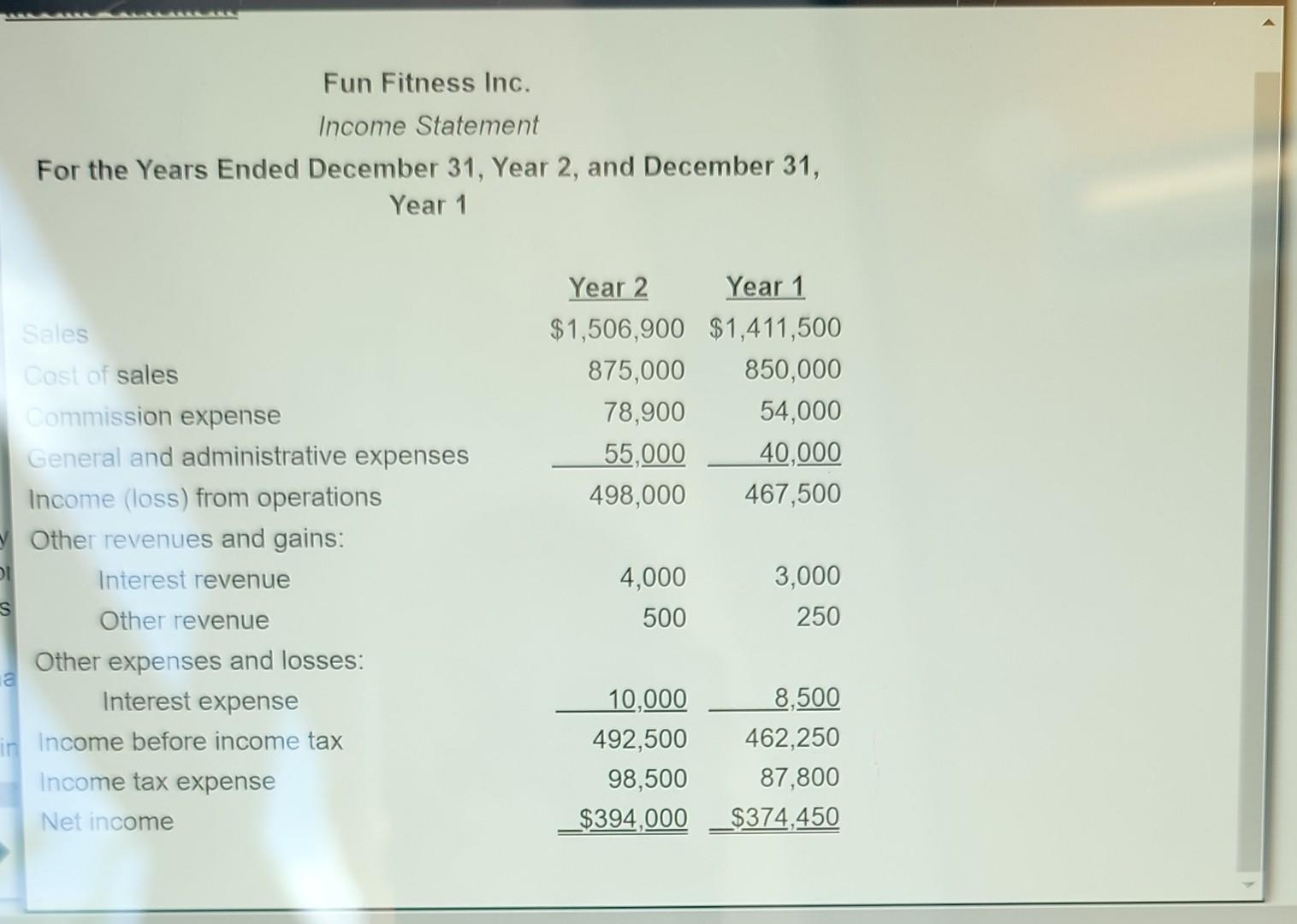

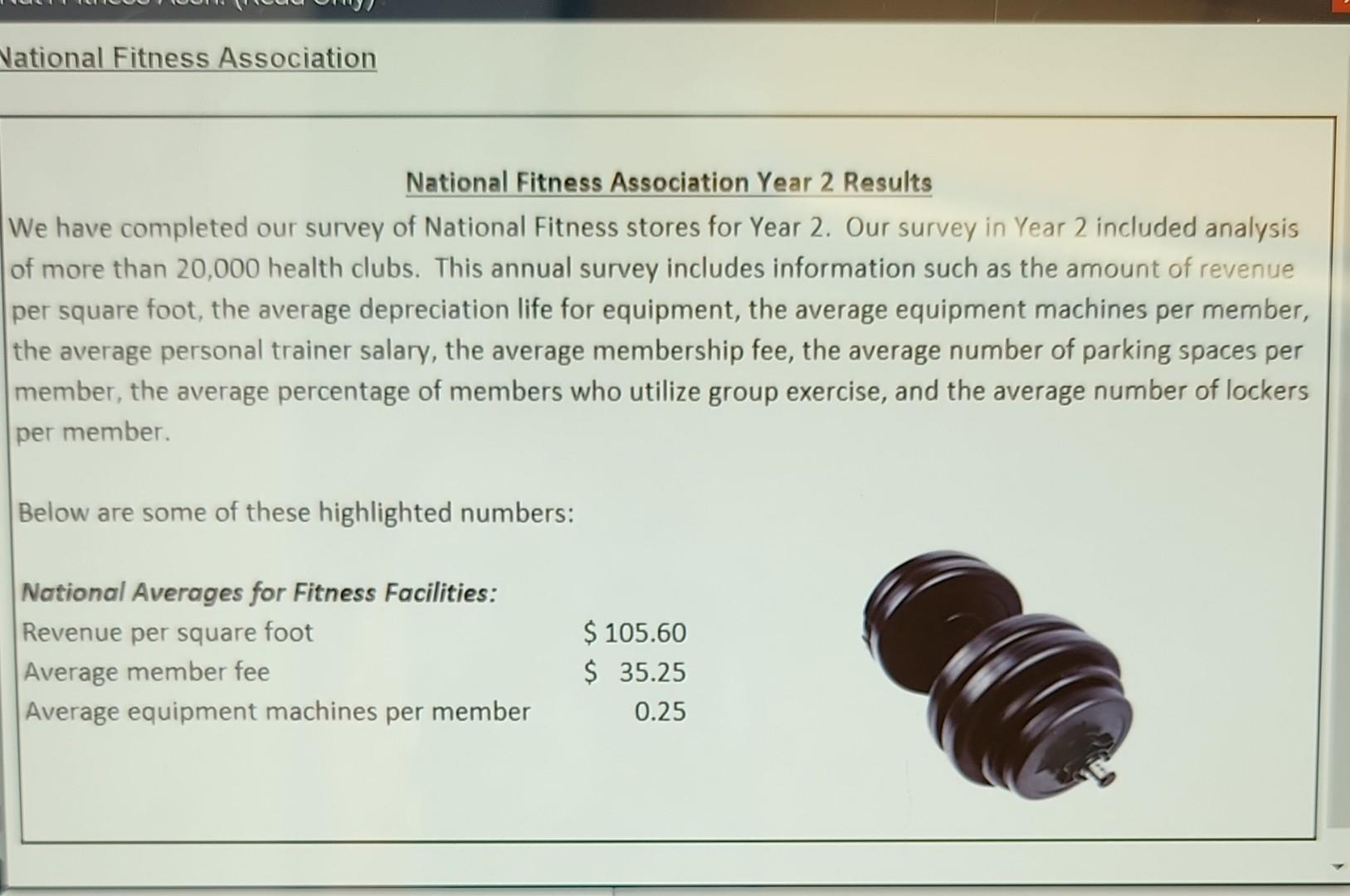

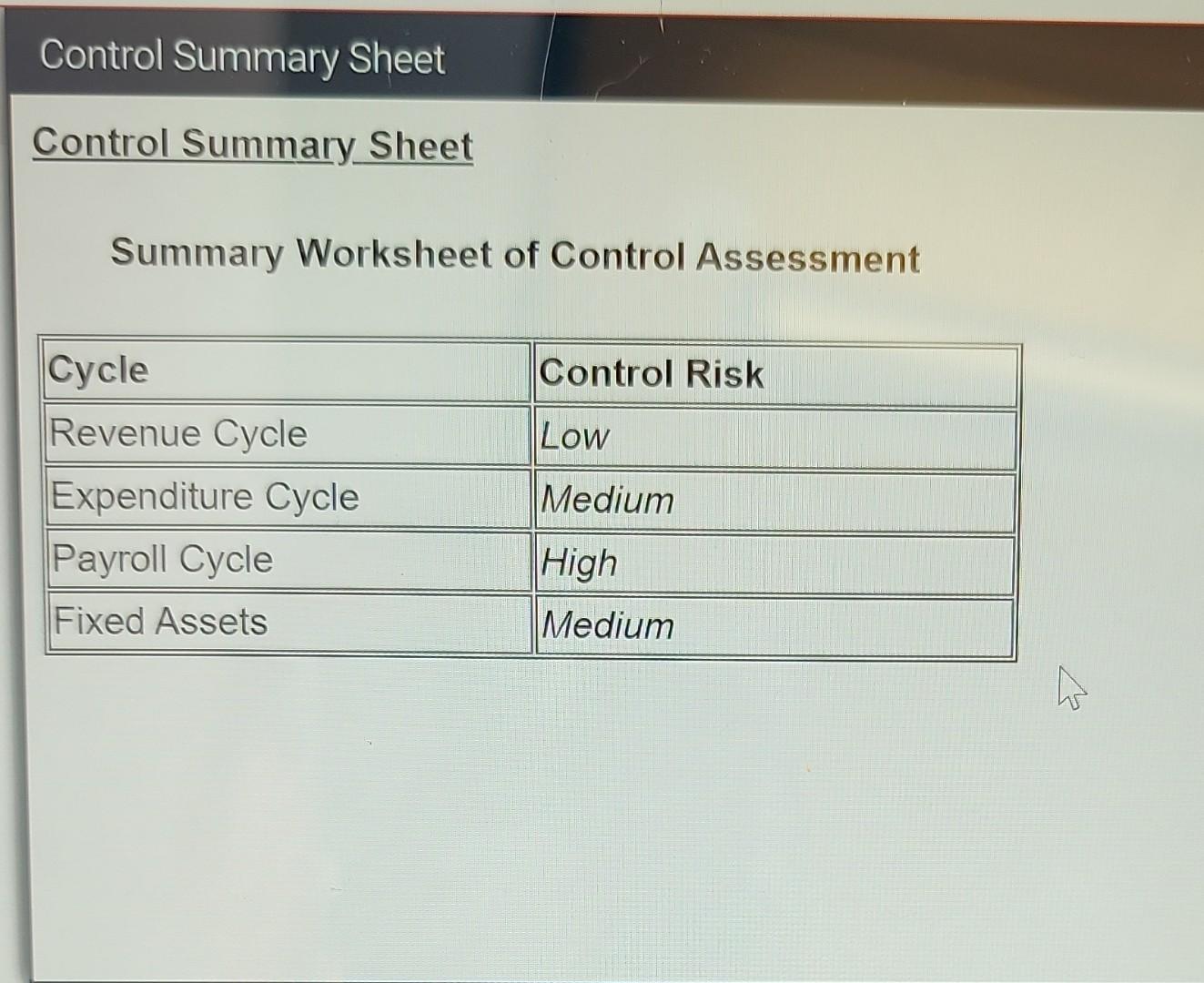

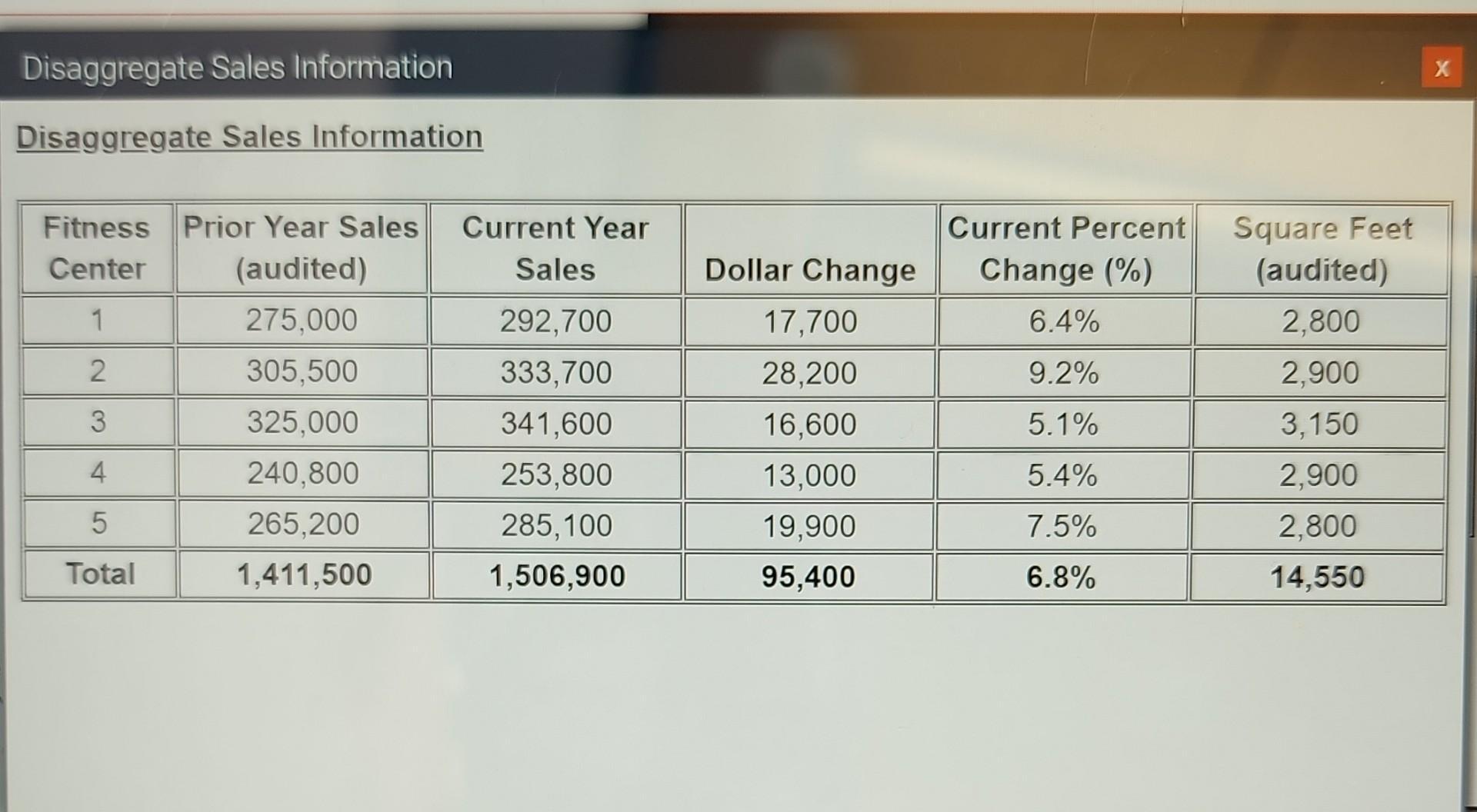

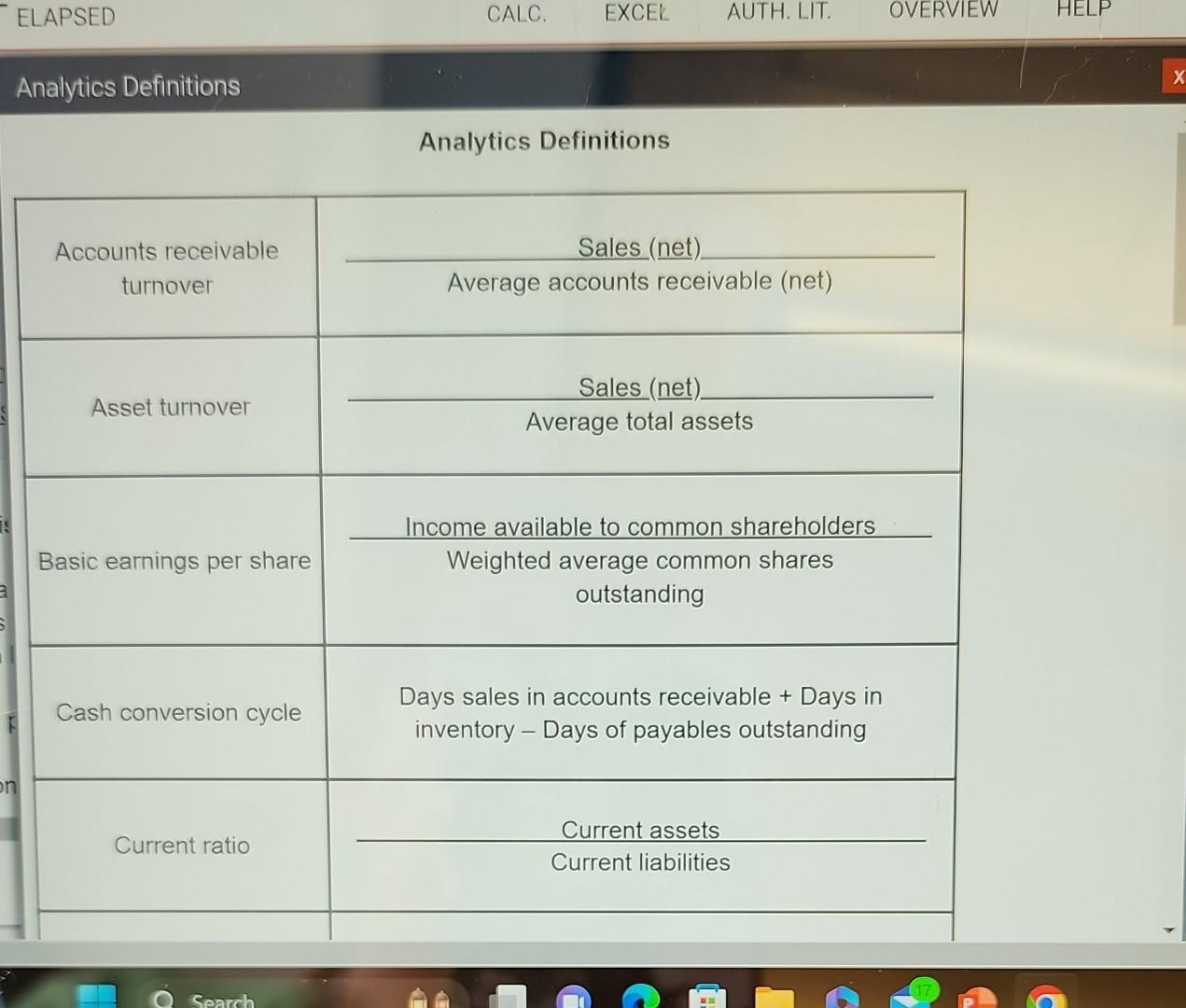

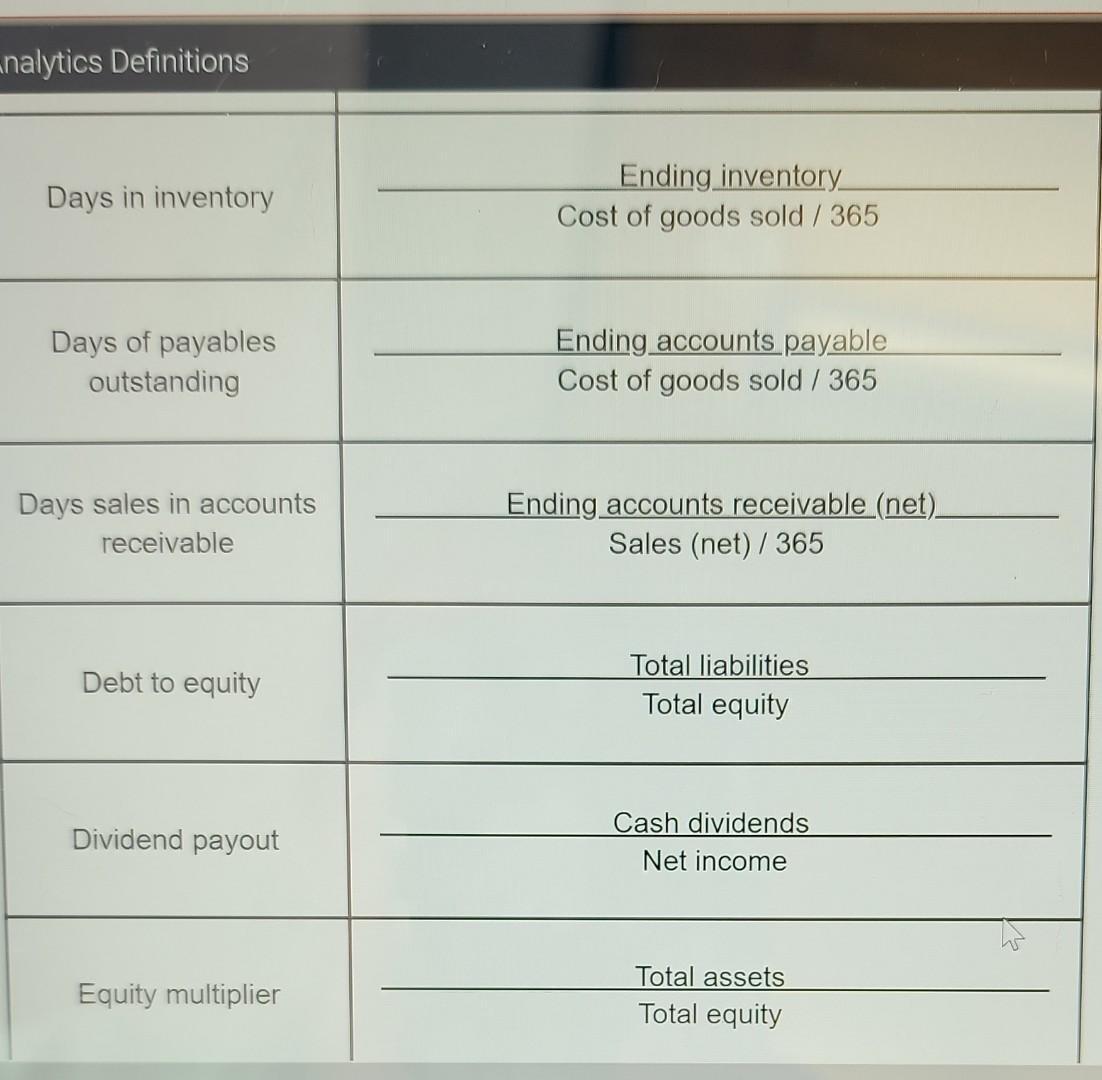

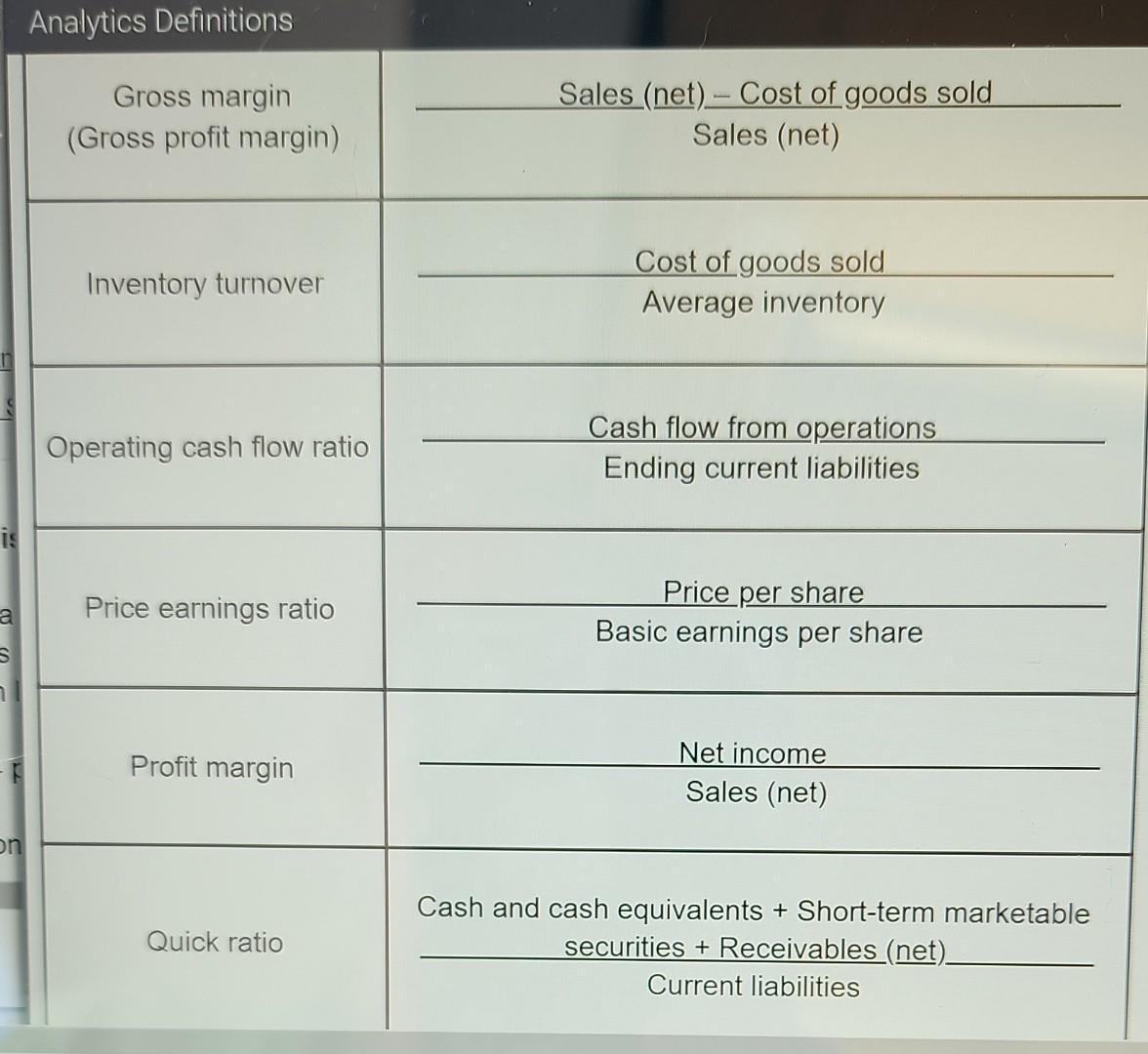

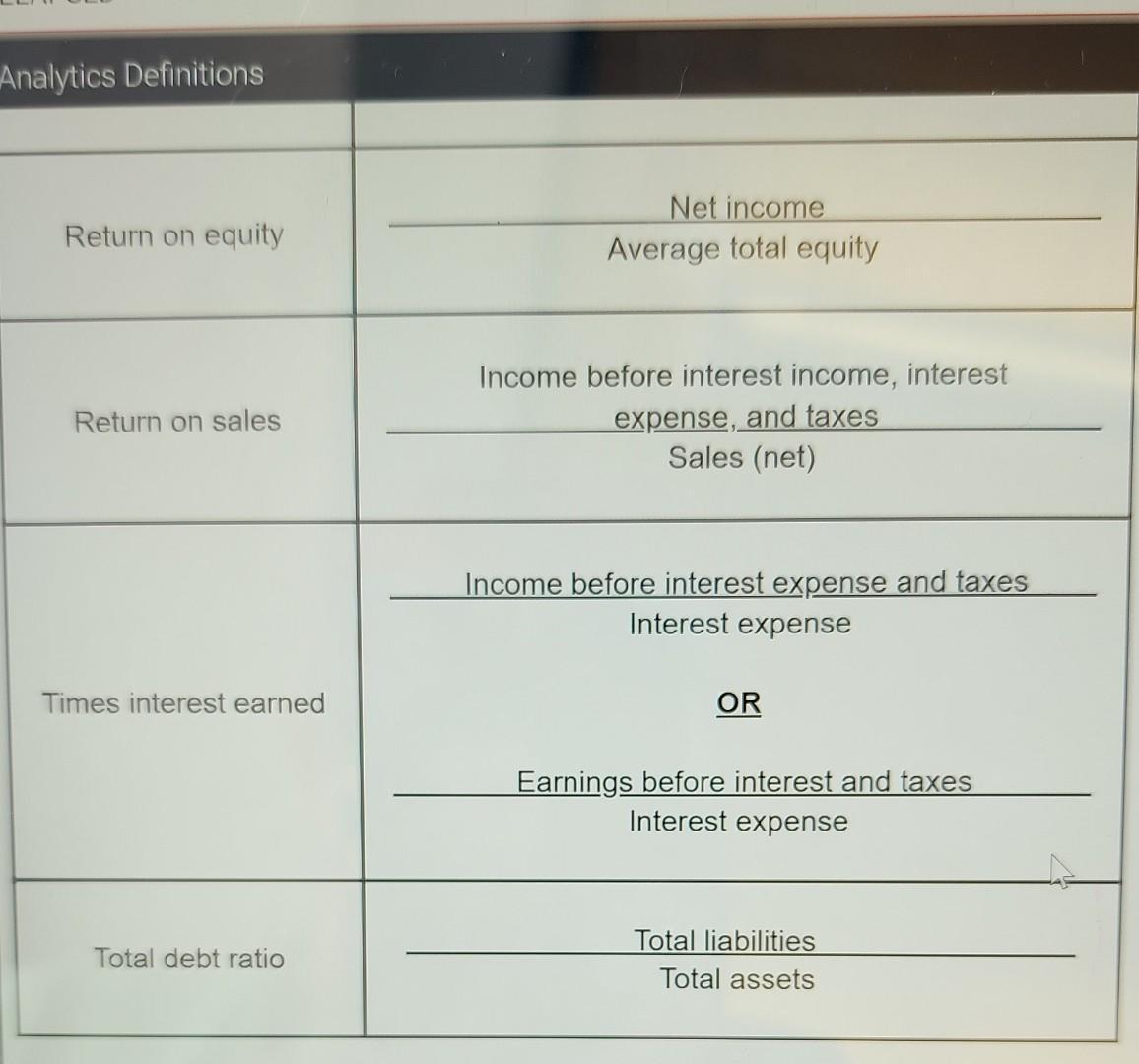

(2) Isaac, CPA, is auditing Fun Fitness Inc., a calendar-year corporation. He is performing analytical procedures relative to the sales account for Year 2. He also audited the consolidated financial statements for Fun Fitness in Year 1 and issued an unmodified opinion. Isaac has set materiality at $40,000, or 4 percent change for year-over-year comparisons. For each type of analytical procedure, consider the information in the exhibits and: • Enter the auditor's calculation/expectation for Year 2. Round all dollar amounts to the nearest dollar and all percentages to the nearest tenth of a percent. • Evaluate the reliability of data from which the expectation is developed. Select from the choices available. Selections may be used once, more than once, or not at all. • Evaluate the significance of the difference for each analytical procedure. Select from the choices available. Selections may be used once, more than once, or not at all. • The information in the Analytics Definitions exhibit must be used for all financial ratio calculations. A B C D 1 Year 2 Year 1 Year-Over-Year Percentage Change 2 Gross margin percentage: 3 Reliability of data: 4 Evaluate the significance of difference: A B C D 1 Year 2 Sales Expected Year 2 Sales Actual Dollar Difference 2 Expectation based on square footage and external industry data: $1,506,900 3 Reliability of data: 4 Evaluate the significance of difference: A B C D 1 Year 2 Sales Expected Year 2 Sales Actual Dollar Difference 2 Expectation based on relationship between sales and commission: $1,506,900 3 Reliability of data: 4 Evaluate the significance of difference: Options for Reliable Data: Reliable or Not reliable Options for Evaluate the Significance of Difference: 1. Difference is material—further investigation necessary 2. Difference is material—no further investigation necessary 3. Difference is immaterial—further investigation necessary 4. Difference is immaterial—no further investigation necessary 5. Method unreliable—perform alternative procedures Internal Memo To: Employees of Fun Fitness Inc. From: HR Date: December 26, Year 1 Happy Holidays! We are excited to announce that in Year National Fitness Association National Fitness Association Year 2 Results We have completed our survey of National Fitness stores for Year 2. Our survey in Disaggregate Sales Information Fitness Center Prior Year Sales (audited) Current Year Sales Dollar Change Current Percent Change (%) Square Feet (audited) 1 275,000 292,700 17,700 6.4% 2,800 2 305,500 333,700 28,200 9.2% 2,900 3 325,000 341,600 16,600 5.1% 3,150 4 240,800 253,800 13,000 5.4% 2,900 5 265,200 285,100 19,900 7.5% 2,800 Total 1,411,500 1,506,900 95,400 6.8% 14,550 Income statement Fun Fitness Inc. Income Statement For the Years Ended December 31, Year 2, and December 31, Year 1 Year 2 Year 1 Sales $1,506,900 $1,411,500 Cost of sales 875,000 850,000 Commission expense 78,900 54,000 General and administrative expenses 55,000 40,000 Income (loss) from operations 498,000 467,500 Other revenues and gains: Interest revenue 4,000 3,000 Other revenue 500 250 Other expenses and losses: Interest expense 10,000 8,500 Income before income tax 492,500 462,250 Income tax expense 98,500 87,800 Net income $394,000 $374,450 Control Summary Sheet Summary Worksheet of Control Assessment Cycle Control Risk Revenue Cycle Low Expenditure Cycle Medium Payroll Cycle High Fixed Assets Medium Analytics Definitions Accounts receivable turnover Sales (net) Average accounts receivable (net) Asset turnover Sales (net) Average total assets Basic earnings per share Income available to common shareholders Weighted average common shares outstanding Cash conversion cycle Days sales in accounts receivable + Days in inventory – Days of payables outstanding Current ratio Current assets Current liabilities Days in inventory Ending inventory Cost of goods sold / 365 Days of payables outstanding Ending accounts payable Cost of goods sold / 365 Days sales in accounts receivable Ending accounts receivable (net) Sales (net) / 365 Debt to equity Total liabilities Total equity Dividend payout Cash dividends Net income Equity multiplier Total assets Total equity Gross margin (Gross profit margin) Sales (net) – Cost of goods sold Sales (net) Inventory turnover Cost of goods sold Average inventory Operating cash flow ratio Cash flow from operations Ending current liabilities Price earnings ratio Price per share Basic earnings per share Profit margin Net income Sales (net) Quick ratio Cash and cash equivalents + Short-term marketable securities + Receivables (net) Current liabilities Return on assets Net income Average total assets Return on equity Net income Average total equity Return on sales Income before interest income, interest expense, and taxes Sales (net)

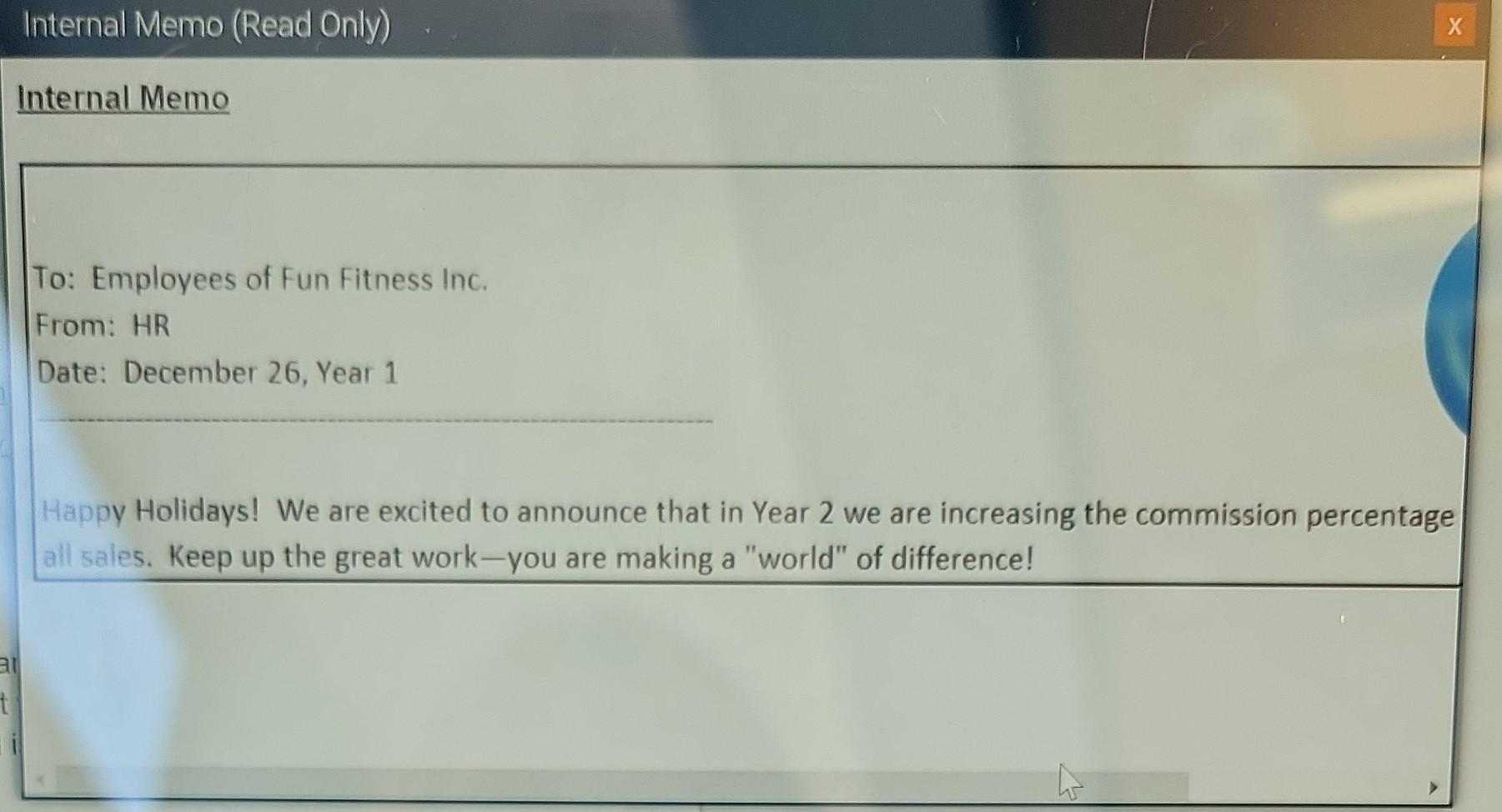

t Internal Memo (Read Only) Internal Memo To: Employees of Fun Fitness Inc. From: HR Date: December 26, Year 1 Happy Holidays! We are excited to announce that in Year 2 we are increasing the commission percentage all sales. Keep up the great work-you are making a "world" of difference! X

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The question is incomplete because it references exhibits and analytical defin...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Business Of Finance

Authors: Withers Hartley 1867 1950

1st Edition

1313069299, 9781313069298