Answered step by step

Verified Expert Solution

Question

1 Approved Answer

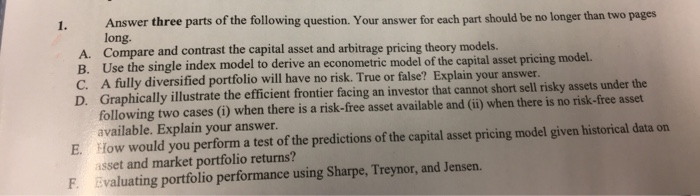

it says to answer 3 parts in this question. so A,B and C please 1. Answer three parts of the following question. Your answer for

it says to answer 3 parts in this question. so A,B and C please  1. Answer three parts of the following question. Your answer for each part should be no longer than two pages long A. Compare and contrast the capital asset and arbitrage pricing theory models. B. Use the single index model to derive an econometric model of the capital asset pricing model. C. A fully diversified portfolio will have no risk. True or false? Explain your answer. D. Graphically illustrate the efficient frontier facing an investor that cannot short sell risky assets under the following two cases (i) when there is a risk-free asset available and (ii) when there is no risk-free asset available. Explain your answer. E How would you perform a test of the predictions of the capital asset pricing model given historical data on asset and market portfolio returns? F. Evaluating portfolio performance using Sharpe, Treynor, and Jensen

1. Answer three parts of the following question. Your answer for each part should be no longer than two pages long A. Compare and contrast the capital asset and arbitrage pricing theory models. B. Use the single index model to derive an econometric model of the capital asset pricing model. C. A fully diversified portfolio will have no risk. True or false? Explain your answer. D. Graphically illustrate the efficient frontier facing an investor that cannot short sell risky assets under the following two cases (i) when there is a risk-free asset available and (ii) when there is no risk-free asset available. Explain your answer. E How would you perform a test of the predictions of the capital asset pricing model given historical data on asset and market portfolio returns? F. Evaluating portfolio performance using Sharpe, Treynor, and Jensen

it says to answer 3 parts in this question. so A,B and C please

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Capital Markets Valuation Capitalization And Transfer Of Private Business Interests

Authors: Robert T. Slee

2nd Edition

0470928328, 978-0470928325