Answered step by step

Verified Expert Solution

Question

1 Approved Answer

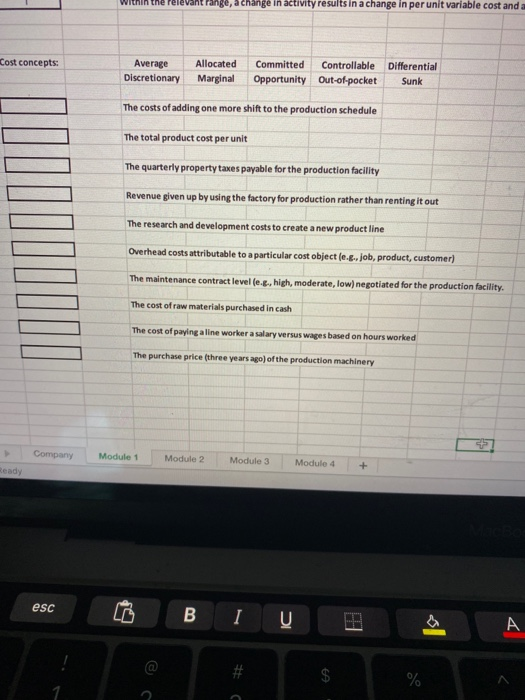

ithin the rere nge, a change in activity results in a change in per unit variable cost and a Cost concepts: Average Discretionary Allocated Marginal

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sm Auditing Integrated Appr Review Copy

Authors: ARENS LO, EBBECKE

7th Edition

0135914396, 978-0135914397