Question

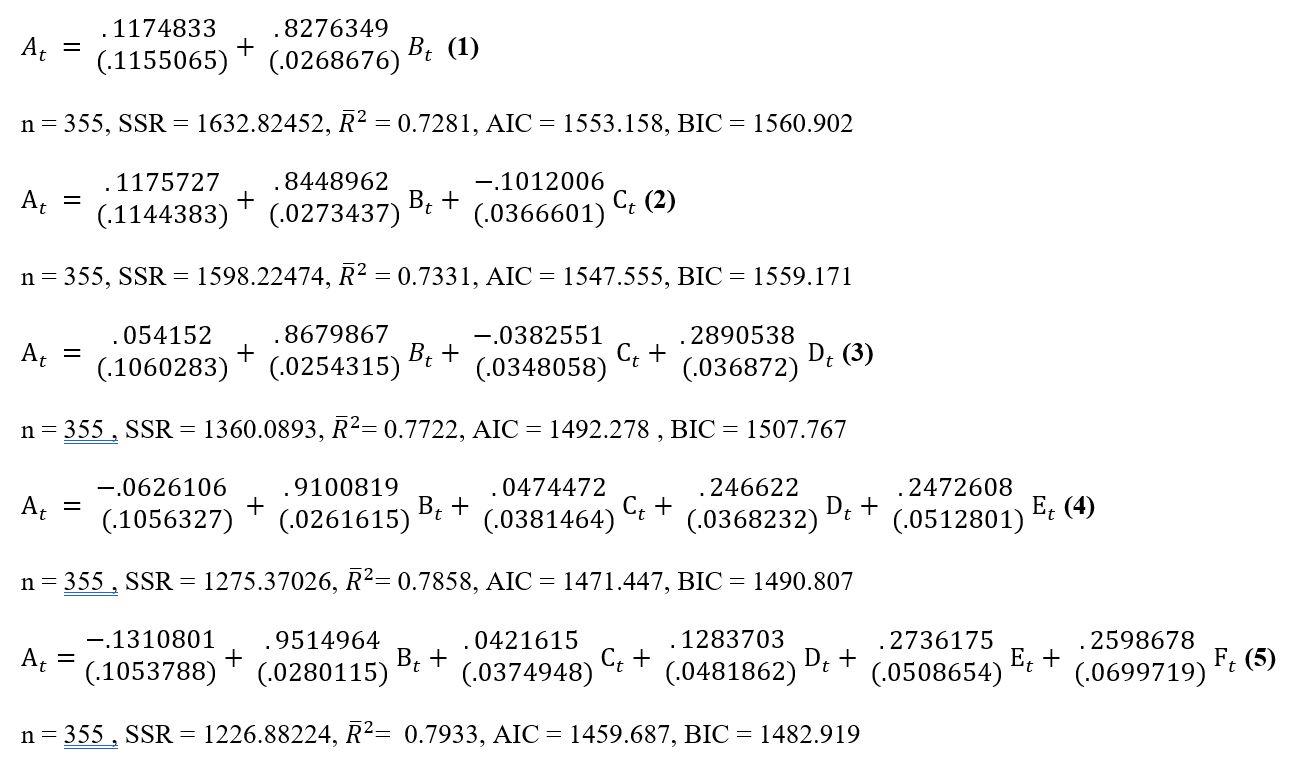

iv. Which OLS regression model below, would you choose as an asset pricing model and why? [15 marks] Standard error is in brackets underneath parameter

iv. Which OLS regression model below, would you choose as an asset pricing model and why? [15 marks]

Standard error is in brackets underneath parameter estimate.

OLS regression models were derived from the variables below:

| A | Excess return on the portfolio | Risk factor associated with the portfolio |

| B | Excess return on the market* | Risk factor associated with the overall market |

| C | Small minus Big | Risk factor associated with the size of stocks |

| D | High minus Low | Risk factor associated with the value of stocks |

| E | Robust minus Weak | Risk factor associated with the profitability of stocks |

| F | Conservative minus Aggressive | Risk factor associated with the investment style of stocks |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

10th edition

77861671, 978-0077861674