Question

I've been stuck on this one for a while and am not quite understanding it U.S. generally accepted accounting principles (GAAP, hereafter) require companies to

I've been stuck on this one for a while and am not quite understanding it

U.S. generally accepted accounting principles (GAAP, hereafter) require companies to report tax expense based on their GAAP pre-tax income. It is often the case that GAAP pre-tax income does not equal taxable income per the tax return. Temporary differences are the primary reason for this. A temporary difference arises when a particular transaction or event effects GAAP income and taxable income in different years. For example, the U.S. tax code allows companies to use accelerated depreciation for fixed assets whereas GAAP requires companies to depreciate fixed assets over their useful lives. Moreover, most companies use straight-line depreciation for financial reporting. Consequently, early in the life of a fixed asset tax depreciation is higher than GAAP depreciation, and thus taxes paid is lower than GAAP tax expense. However, this pattern eventually reverses, and thus later in the life of the same fixed asset tax depreciation is lower than GAAP depreciation and taxes paid is higher than GAAP tax expense. Consequently, over the life of the fixed asset the cumulative depreciation per the tax return is the same as the cumulative depreciation per GAAP; and, the cumulative difference between GAAP tax expense and taxes paid is zero. This is the reason we use the term temporary differences.

Given that for any specific year tax expense and taxes paid might not be equal, the balance sheet will not balance unless additional accounting entries are made. Specifically, the change in cash attributable to the payment of taxes will not equal the change in retained earnings attributable to tax expense, and thus assets will not equal the sum of liabilities and equity. To eliminate this problem accountants report deferred tax assets and deferred tax liabilities. To understand how this works, consider the depreciation example discussed above. Early in the life of the fixed asset taxes paid (and the reduction in cash) is less than tax expense (and the reduction in retained earnings). Hence, to make the balance sheet balance we record a deferred tax liability. This liability will grow during the years when tax depreciation exceeds GAAP depreciation. However, GAAP depreciation will eventually become larger than tax depreciation and when it does the liability will begin to decline until it eventually disappears.

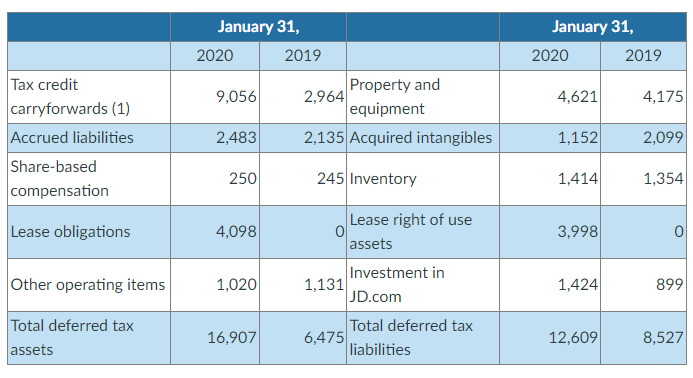

Per GAAP, companies must report the various sources of their deferred tax assets and deferred tax liabilities. For example, in its Annual Report to Shareholders for the 2019 fiscal year, Walmart provided the following table in Note 9 to its financial statements.

- These are excess credits that Walmart can use to reduce future taxable income. Walmart obtained them because it generated operating losses in certain jurisdictions.

When reading the table keep in mind that it shows the sources of deferred tax assets and deferred tax liabilities. Hence, it may initially seem confusing that Accrued liabilities and lease obligations are in the column relating to deferred tax assets. However, this is correct. Specifically, it reflects the fact that Walmart recognized expenses relating to accrued liabilities and lease obligations in its GAAP income. However, these expenses have not be recognized in Walmarts taxable income yet. Hence, GAAP tax expense is currently lower than taxes paid, and thus Walmart recognizes a deferred tax asset to make the balance sheet balance. This difference will eventually reverse when the liability and related expense are recognized for tax purposes.

Which items in the list of Walmarts deferred tax assets are operating assets?

Which items in the list of Walmarts deferred tax liabilities are operating liabilities?

\begin{tabular}{|l|r|r|l|r|r|} \hline & \multicolumn{2}{|c|}{ January 31, } & \multicolumn{2}{c|}{ January 31, } \\ \hline & 2020 & \multicolumn{1}{|c|}{2019} & & 2020 & \multicolumn{1}{c|}{2019} \\ \hline Taxcreditcarryforwards(1) & 9,056 & 2,964 & Propertyandequipment & 4,621 & 4,175 \\ \hline Accrued liabilities & 2,483 & 2,135 & Acquired intangibles & 1,152 & 2,099 \\ \hline Share-basedcompensation & 250 & 245 & Inventory & 1,414 & 1,354 \\ \hline Lease obligations & 1,098 & 0 & Leaserightofuseassets & 3,998 & 0 \\ \hline Other operating items & 16,907 & 6,475 & Totaldeferredtaxliabilities & 1,424 & 899 \\ \hline Totaldeferredtaxassets & J.com & 12,609 & 8,527 \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Robert Libby, Patricia Libby, Daniel Short

5th Edition

0073208140, 978-0073208145