Answered step by step

Verified Expert Solution

Question

1 Approved Answer

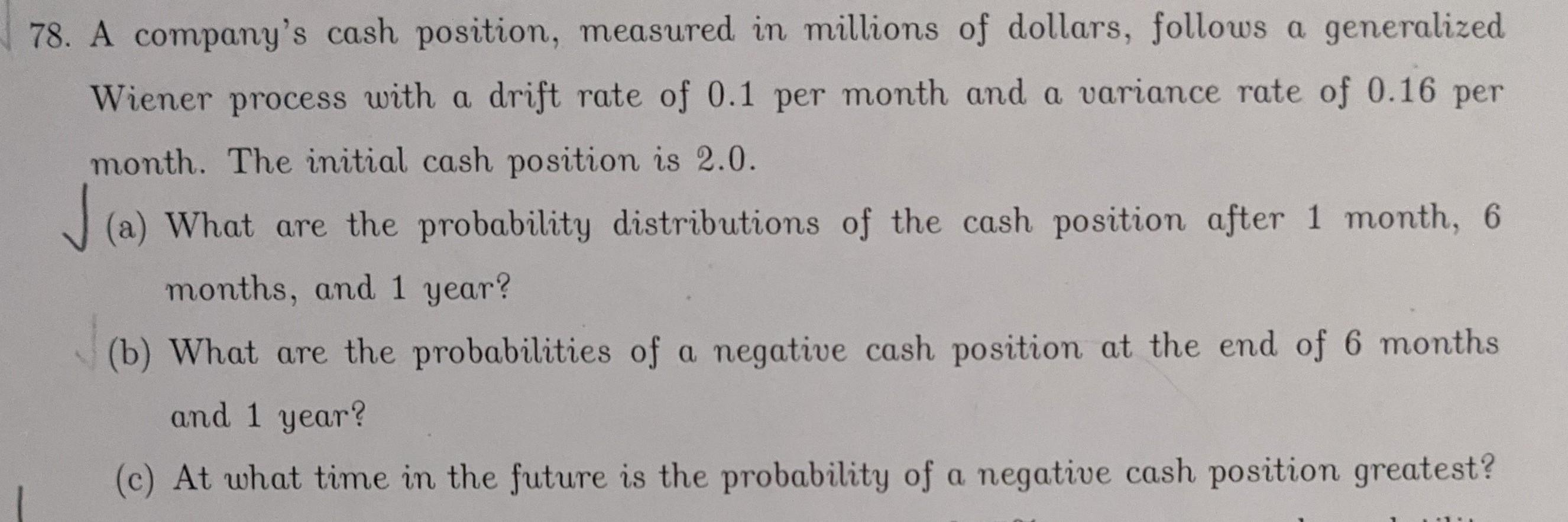

J , 78. A company's cash position, measured in millions of dollars, follows a generalized Wiener process with a drift rate of 0.1 per month

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance Discussion Papers Managing Beliefs About Monetary Policy Under Discretion

Authors: United States Federal Reserve Board, Elmar Mertens

1st Edition

1288704577, 9781288704576