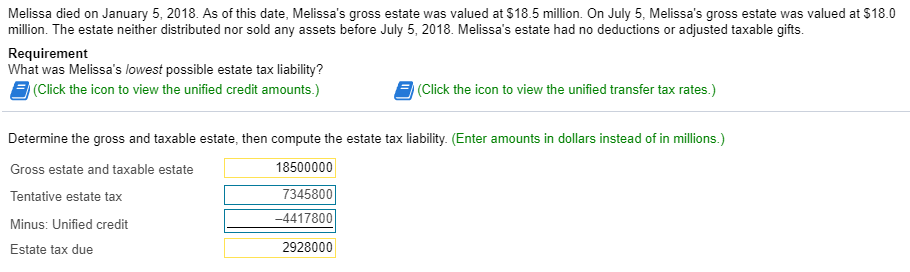

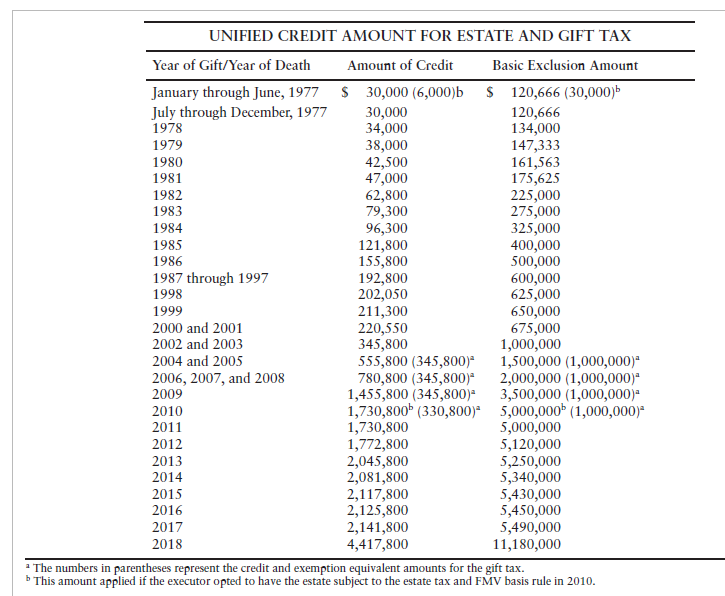

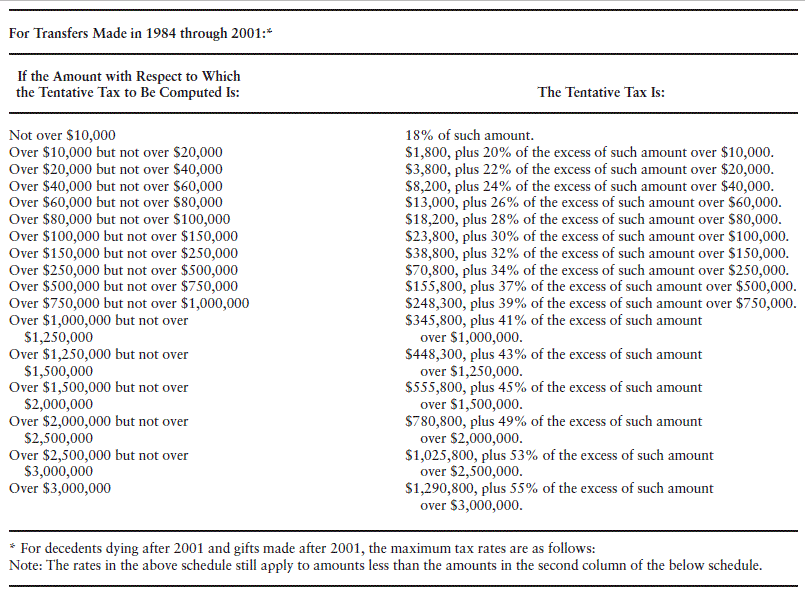

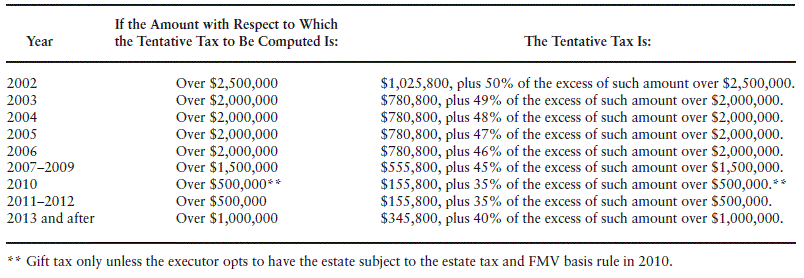

January 5, 2018. As of this date, Melissa's gross estate was valued at $18.5 million. On July 5, Melissa's gross estate was valued at $18.0 Melissa died on million. The estate neither distributed nor sold any assets before July 5, 2018. Melissa's estate had no deductions or adjusted taxable gifts. Requirement What was Melissa's lowest possible estate tax liability? (Click the icon to view the unified credit amounts.) (Click the icon to view the unified transfer tax rates.) Determine the gross and taxable estate, then compute the estate tax liability. (Enter amounts in dollars instead of in millions.) 18500000 Gross estate and taxable estate 7345800 Tentative estate tax -4417800 Minus: Unified credit 2928000 Estate tax due UNIFIED CREDIT AMOUNT FOR ESTATE AND GIFT TAX Year of Gift/Year of Death Amount of Credit Basic Exclusion Amount S 120,666 (30,000)b January through June, 1977 July through December, 1977 S 30,000 (6,000)b 30,000 34,000 38,000 42,500 47,000 62,800 79,300 96,300 121,800 155,800 192,800 202,050 211,300 220,550 345,800 555,800 (345,800) 780,800 (345,800) 1,455,800 (345,800) 1,730,800 (330,800)* 1,730,800 1,772,800 2,045,800 2,081,800 2,117,800 2,125,800 2,141,800 4,417,800 120,666 134,000 147,333 161,563 175,625 225,000 275,000 325,000 400,000 500,000 600,000 625,000 650,000 675,000 1,000,000 1,500,000 (1,000,000)* 2,000,000 (1,000,000)* 3,500,000 (1,000,000) 5,000,000 (1,000,000) 5,000,000 5,120,000 5,250,000 5,340,000 5,430,000 5,450,000 5,490,000 11,180,000 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 through 1997 1998 1999 2000 and 2001 2002 and 2003 2004 and 2005 2006, 2007, and 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 The numbers in parentheses represent the credit and exemption equivalent amounts for the gift tax b This amount applied if the executor opted to have the estate subject to the estate tax and FMV basis rule in 2010 For Transfers Made in 1984 through 2001:* If the Amount with Respect to Which the Tentative Tax to Be Computed Is The Tentative Tax Is: 18% of such amount $1,800, plus 20% of the excess of such amount over $10,000 $3,800, plus 22% of the excess of such amount over $8,200, plus 24% of the excess of such amount over $13,000, plus 26% of the excess of such amount over $18,200, plus 28% of the excess of such amount over $23,800, plus 30% of the excess of such amount over $100,000. $38,800, plus 32% of the excess of such amount over $150,000. $70,800, plus 34% of the excess of such amount over $250,000. $155,800, plus 37% of the excess of such amount over $500,000. $248,300, plus 39% of the excess of such amount over $750,000. $345,800, plus 41% of the excess of such amount over $1,000,000 $448,300, plus 43% of the excess of such amount over $1,250,000 $555,800, plus 45% of the excess of such amount over $1,500,000 $780,800, plus 49% of the excess of such amount Not over $10,000 Over $10,000 but not over $20,000 Over $20,000 but not over Over $40,000 but not ove Over $60,000 but not over $80,000 Over $80,000 but not over $100,000 Over $100,000 but not over $150,000 Over $150,000 but not over $250,000 Over $250,000 but not over $500,000 Over $500,000 but not over $750,000 Over $750,000 but not over $1,000,000 Over $1,000,000 but not over S1,250,000 Over $1,250,000 but not over $1,500,000 Over $1,500,000 but not over $2,000,000 Over $2,000,000 but not over S2,500,000 Over $2,500,000 but not over $3,000,000 Over $3,000,000 $20,000 $40,000 $60,000 $80,000 $40,000 $60,000 ver $2,000,000. over $1,025,800, plus 53% of the excess of such amount $2,500,000 $1,290,800, plus 55% of the excess of such amount over $3,000,000 over For decedents dying after 2001 and gifts made after 2001, the maximum tax rates are as follows Note: The rates in the above schedule still apply to amounts less than the amounts in the second column of the below schedule If the Amount with Respect to Which the Tentative Tax to Be Computed Is The Tentative Tax Is: Year $1,025,800, plus 50% of the excess of such amount over $2,500,000. $780,800, plus 49% of the excess of such amount over $780,800, plus 48% of the excess of such $780,800, plus 47% of the excess of such $780,800, plus 46% of the excess of such $555,800, plus 45% of the excess of such amount over $1,500,000 $155,800, plus 35% of the excess of such amount over $500,000.* $155,800, plus 35% of the excess of such amount over $500,000. $345,800, plus 40% of the excess of such amount over Over $2,500,000 Over $2,000,000 Over $2,000,000 Over $2,000,000 Over $2,000,000 Over $1,500,000 Over $500,000** Over $500,000 Over $1,000,000 2002 $2,000,000 $2,000,000 $2,000,000 $2,000,000 2003 2004 amount over 2005 amount over 2006 amount over 2007-2009 2010 2011-2012 $1,000,000 2013 and after Gift tax only unless the executor opts to have the estate subject to the estate tax and FMV basis rule in 2010. January 5, 2018. As of this date, Melissa's gross estate was valued at $18.5 million. On July 5, Melissa's gross estate was valued at $18.0 Melissa died on million. The estate neither distributed nor sold any assets before July 5, 2018. Melissa's estate had no deductions or adjusted taxable gifts. Requirement What was Melissa's lowest possible estate tax liability? (Click the icon to view the unified credit amounts.) (Click the icon to view the unified transfer tax rates.) Determine the gross and taxable estate, then compute the estate tax liability. (Enter amounts in dollars instead of in millions.) 18500000 Gross estate and taxable estate 7345800 Tentative estate tax -4417800 Minus: Unified credit 2928000 Estate tax due UNIFIED CREDIT AMOUNT FOR ESTATE AND GIFT TAX Year of Gift/Year of Death Amount of Credit Basic Exclusion Amount S 120,666 (30,000)b January through June, 1977 July through December, 1977 S 30,000 (6,000)b 30,000 34,000 38,000 42,500 47,000 62,800 79,300 96,300 121,800 155,800 192,800 202,050 211,300 220,550 345,800 555,800 (345,800) 780,800 (345,800) 1,455,800 (345,800) 1,730,800 (330,800)* 1,730,800 1,772,800 2,045,800 2,081,800 2,117,800 2,125,800 2,141,800 4,417,800 120,666 134,000 147,333 161,563 175,625 225,000 275,000 325,000 400,000 500,000 600,000 625,000 650,000 675,000 1,000,000 1,500,000 (1,000,000)* 2,000,000 (1,000,000)* 3,500,000 (1,000,000) 5,000,000 (1,000,000) 5,000,000 5,120,000 5,250,000 5,340,000 5,430,000 5,450,000 5,490,000 11,180,000 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 through 1997 1998 1999 2000 and 2001 2002 and 2003 2004 and 2005 2006, 2007, and 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 The numbers in parentheses represent the credit and exemption equivalent amounts for the gift tax b This amount applied if the executor opted to have the estate subject to the estate tax and FMV basis rule in 2010 For Transfers Made in 1984 through 2001:* If the Amount with Respect to Which the Tentative Tax to Be Computed Is The Tentative Tax Is: 18% of such amount $1,800, plus 20% of the excess of such amount over $10,000 $3,800, plus 22% of the excess of such amount over $8,200, plus 24% of the excess of such amount over $13,000, plus 26% of the excess of such amount over $18,200, plus 28% of the excess of such amount over $23,800, plus 30% of the excess of such amount over $100,000. $38,800, plus 32% of the excess of such amount over $150,000. $70,800, plus 34% of the excess of such amount over $250,000. $155,800, plus 37% of the excess of such amount over $500,000. $248,300, plus 39% of the excess of such amount over $750,000. $345,800, plus 41% of the excess of such amount over $1,000,000 $448,300, plus 43% of the excess of such amount over $1,250,000 $555,800, plus 45% of the excess of such amount over $1,500,000 $780,800, plus 49% of the excess of such amount Not over $10,000 Over $10,000 but not over $20,000 Over $20,000 but not over Over $40,000 but not ove Over $60,000 but not over $80,000 Over $80,000 but not over $100,000 Over $100,000 but not over $150,000 Over $150,000 but not over $250,000 Over $250,000 but not over $500,000 Over $500,000 but not over $750,000 Over $750,000 but not over $1,000,000 Over $1,000,000 but not over S1,250,000 Over $1,250,000 but not over $1,500,000 Over $1,500,000 but not over $2,000,000 Over $2,000,000 but not over S2,500,000 Over $2,500,000 but not over $3,000,000 Over $3,000,000 $20,000 $40,000 $60,000 $80,000 $40,000 $60,000 ver $2,000,000. over $1,025,800, plus 53% of the excess of such amount $2,500,000 $1,290,800, plus 55% of the excess of such amount over $3,000,000 over For decedents dying after 2001 and gifts made after 2001, the maximum tax rates are as follows Note: The rates in the above schedule still apply to amounts less than the amounts in the second column of the below schedule If the Amount with Respect to Which the Tentative Tax to Be Computed Is The Tentative Tax Is: Year $1,025,800, plus 50% of the excess of such amount over $2,500,000. $780,800, plus 49% of the excess of such amount over $780,800, plus 48% of the excess of such $780,800, plus 47% of the excess of such $780,800, plus 46% of the excess of such $555,800, plus 45% of the excess of such amount over $1,500,000 $155,800, plus 35% of the excess of such amount over $500,000.* $155,800, plus 35% of the excess of such amount over $500,000. $345,800, plus 40% of the excess of such amount over Over $2,500,000 Over $2,000,000 Over $2,000,000 Over $2,000,000 Over $2,000,000 Over $1,500,000 Over $500,000** Over $500,000 Over $1,000,000 2002 $2,000,000 $2,000,000 $2,000,000 $2,000,000 2003 2004 amount over 2005 amount over 2006 amount over 2007-2009 2010 2011-2012 $1,000,000 2013 and after Gift tax only unless the executor opts to have the estate subject to the estate tax and FMV basis rule in 2010