Answered step by step

Verified Expert Solution

Question

1 Approved Answer

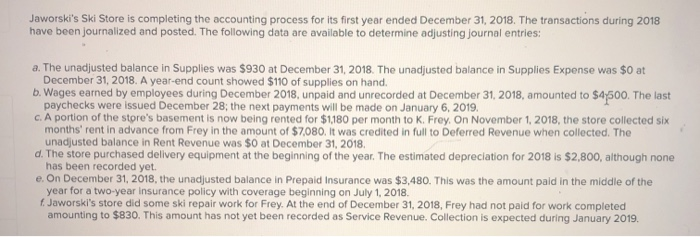

Jaworski's Ski Store is completing the accounting process for its first year ended December 31, 2018. The transactions during 2018 have been journalized and posted.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Property Companies An Industry Accounting And Auditing Guide

Authors: Accountancy Books

1st Edition

1853558079, 978-1853558078