Answered step by step

Verified Expert Solution

Question

1 Approved Answer

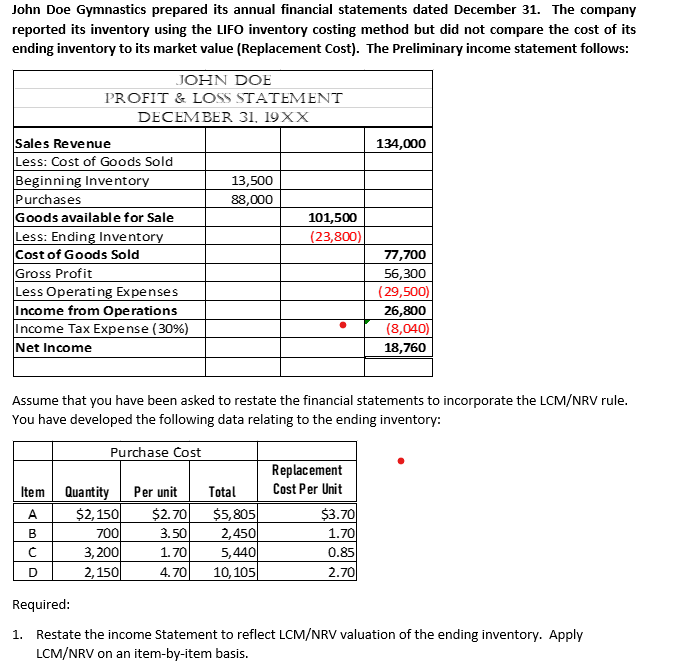

John Doe Gymnastics prepared its annual financial statements dated December 31. The company reported its inventory using the LIFO inventory costing method but did not

John Doe Gymnastics prepared its annual financial statements dated December 31. The company reported its inventory using the LIFO inventory costing method but did not compare the cost of its ending inventory to its market value (Replacement Cost). The Preliminary income statement follows: Assume that you have been asked to restate the financial statements to incorporate the LCM/NRV rule. You have developed the following data relating to the ending inventory: Required: 1. Restate the income Statement to reflect LCM/NRV valuation of the ending inventory. Apply LCM/NRV on an item-by-item basis

John Doe Gymnastics prepared its annual financial statements dated December 31. The company reported its inventory using the LIFO inventory costing method but did not compare the cost of its ending inventory to its market value (Replacement Cost). The Preliminary income statement follows: Assume that you have been asked to restate the financial statements to incorporate the LCM/NRV rule. You have developed the following data relating to the ending inventory: Required: 1. Restate the income Statement to reflect LCM/NRV valuation of the ending inventory. Apply LCM/NRV on an item-by-item basis Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Towards A Strategic Human Resource Management Roles Of HR Audit And Org Culture

Authors: Adel Al Samman

1st Edition

3330653051, 978-3330653054