JOHNAQUELCH JAMES T. KI NDL E '1' Brannigan Foods: Strategic Marketing Planning On a rainy New Jersey morning in November. 3013. Bert Clark. vice-president and

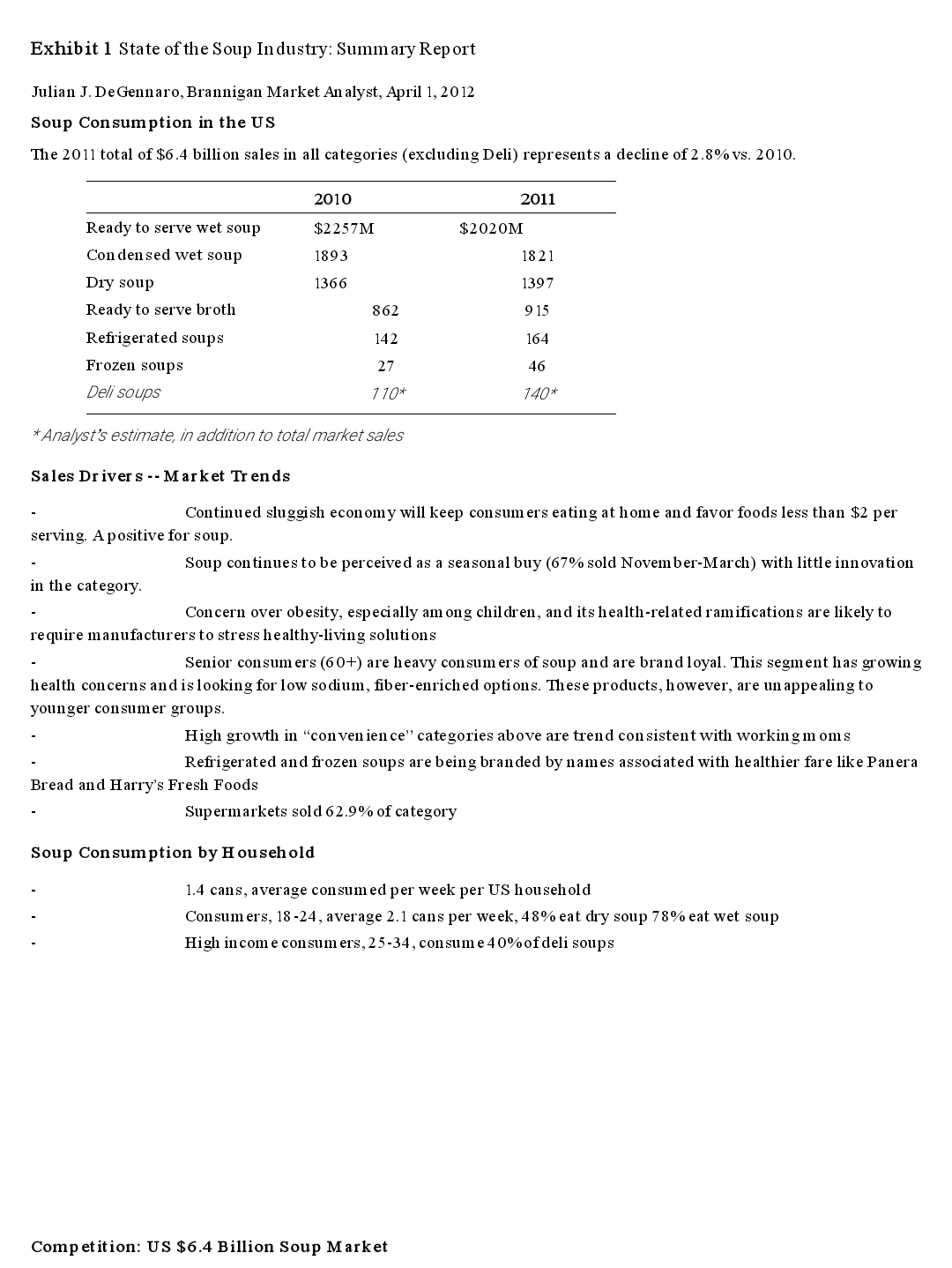

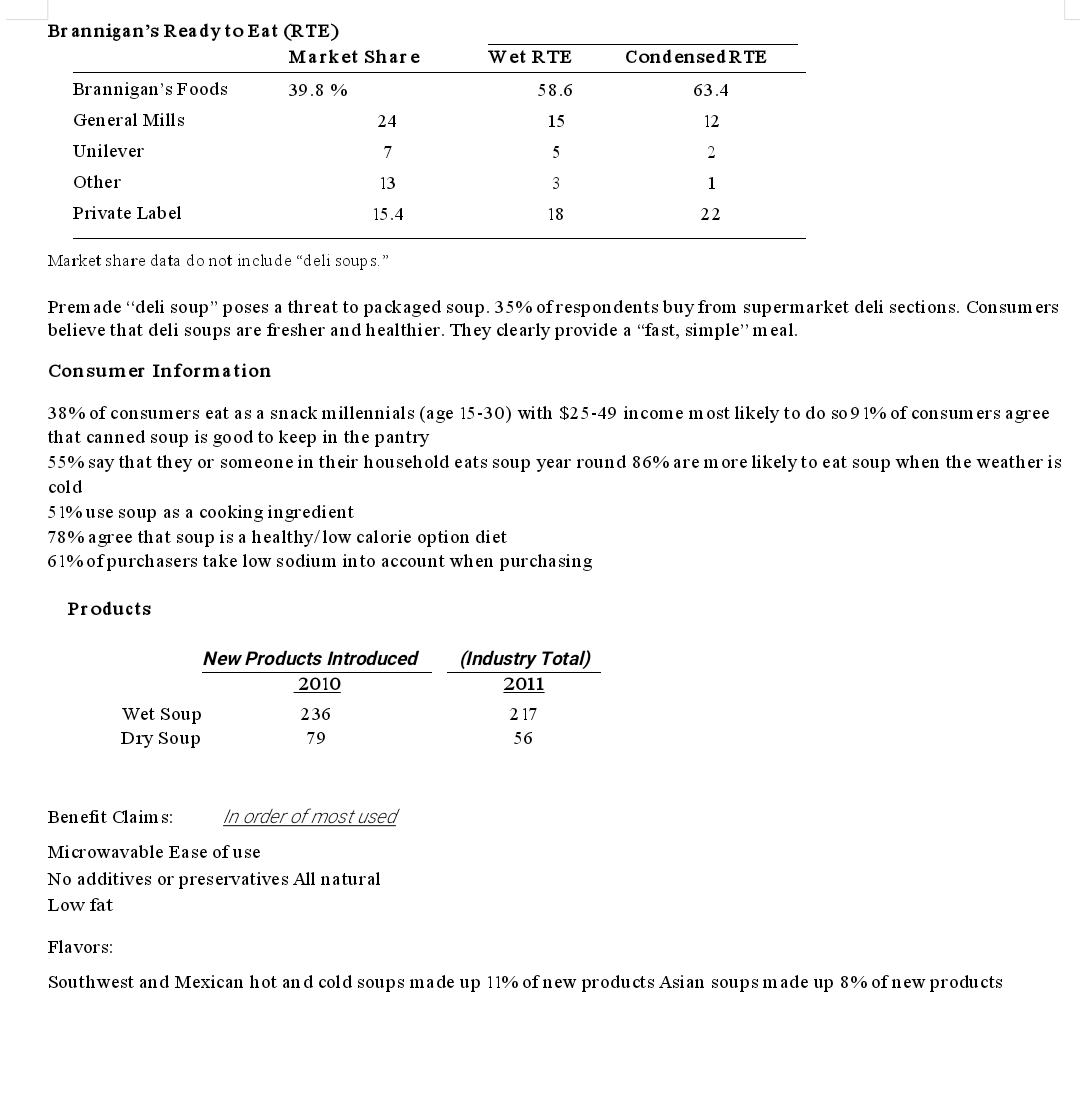

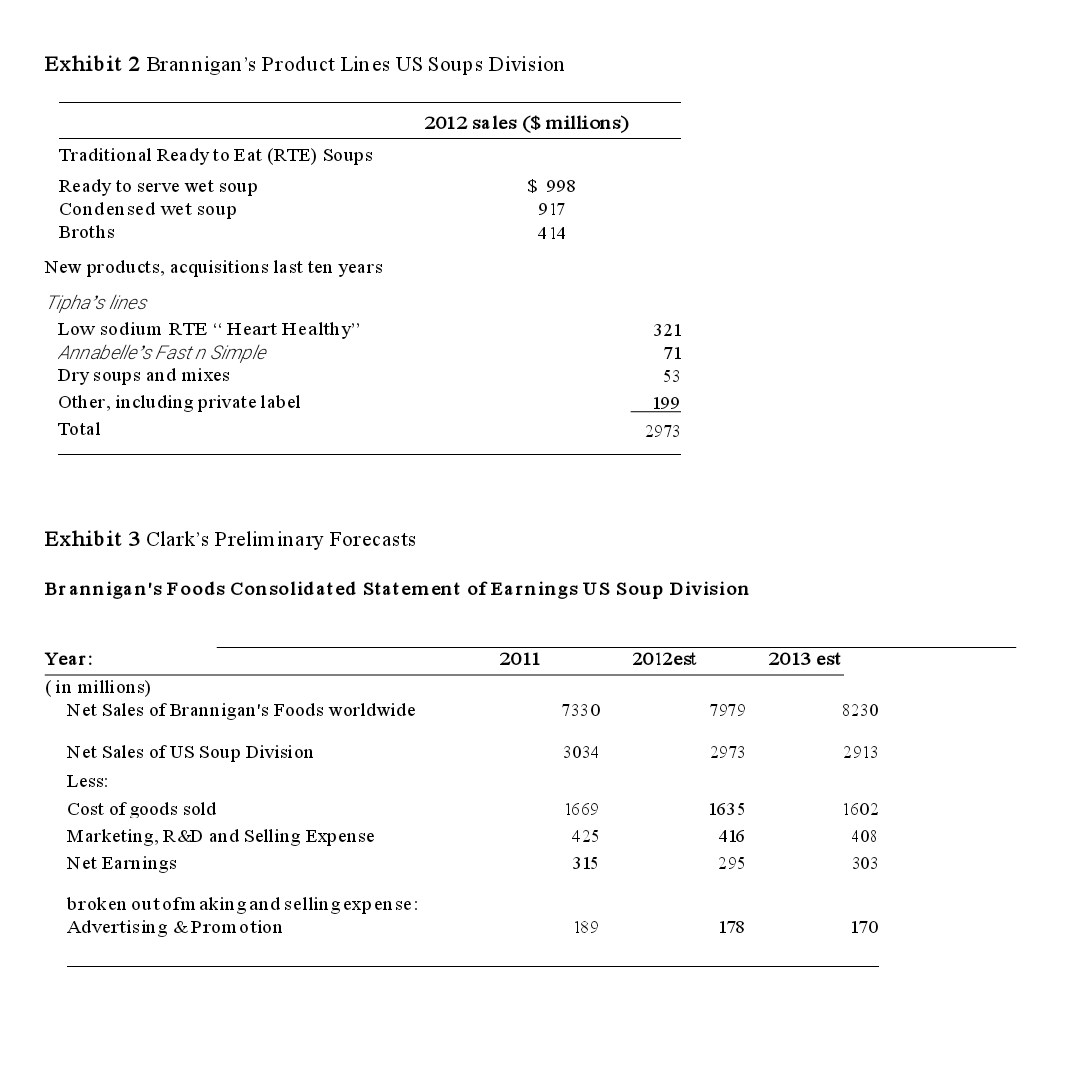

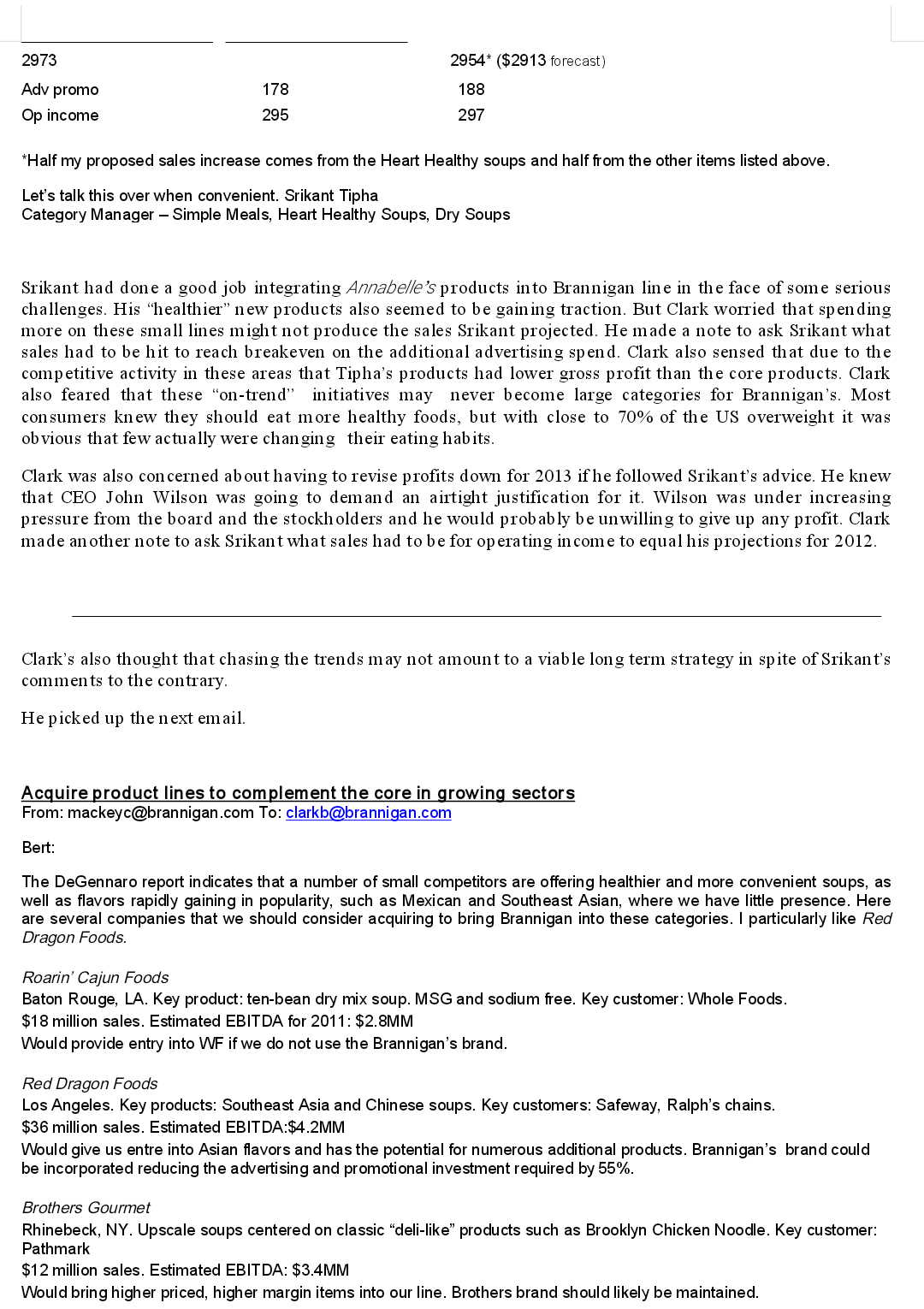

JOHNAQUELCH JAMES T. KI NDL E '1' Brannigan Foods: Strategic Marketing Planning On a rainy New Jersey morning in November. 3013. Bert Clark. vice-president and general manager of Brannigan Foods' Soup Division. scanned his in-box for new messages. He saw that each of his four key managers had digested analyst Julian DeGennaro's annual \"State of the Soup Industry\" summaly report (Exhibit 1) and had responded to Clark's request that they recommend their best investment bets for the division. (See Exhibit 2 for Brannigan's product lines.) In Clark's 16-year career with Brannigan he couldn't remember a tougher. more complicated challenge than the one he now faced. The soup industry had been in steady decline for severalyears. and the division's sales. market share. and profitability had slipped for the last three. Clark skimmed his managers' emails. hoping for new concepts and fresh. timely arguments. Each manager had indeed sketched a proposal \"most likely to turn the division around." Unfortunately. the proposals bore no resemblance to each other. Clark decided to revisit DeGennaro's report and then consider each proposal in depth. The Soup Industry in 2012 As he reviewed DeGennaro's findings. Clark was particularly concerned about the major consumer trends affecting the sale of soup. Condensed and ready-to-eat (RTE) soups were still a staple in most diets in the United States. However. the growing concern about health and obesity had led to a reduction in processed foods in general and products with high sodium content in particular. This trend was especially pronounced among the so-called baby boomer generation (born between 1946 and 1964). the first wave ofwhich was now entering retirement. This group was the largest and most brand-loyal segment of soup consumers. as the report indicated. Products had to be targeted to them. However. this had serious long-term implications for Brannigan as it also needed to engage younger generations of consumers. Clark felt. in fact. that this was one of the most pressing needs for the company. The other critical trend lay in the US. population's increasing desire. especially among working mothers. for fa st. simple meals. Clark needed to win this consumer from a wide array of strong competitors. The rapidly increasing sales ofpremade \"deli soups\". d1y-miX soups. and 111icrowavable packaged soups. while not nearly as large as the canned soups categ01y. was consistent with Exhibit 1 State of the Soup Industry: Summary Report Julian J. DeGennaro, Brannigan Market Analyst, April 1, 2012 Soup Consumption in the US The 2011 total of $6.4 billion sales in all categories (excluding Deli) represents a decline of 2.8% vs. 2010. 2010 2011 Ready to serve wet soup $2257M $2020M Condensed wet soup 1893 1821 Dry soup 1366 1397 Ready to serve broth 862 915 Refrigerated soups 142 164 Frozen soups 27 46 Deli soups 1 10 140* *Analyst's estimate, in addition to total market sales Sales Drivers -- Market Trends Continued sluggish economy will keep consumers eating at home and favor foods less than $2 per serving. A positive for soup. Soup continues to be perceived as a seasonal buy (67% sold November-March) with little innovation in the category. Concern over obesity, especially among children, and its health-related ramifications are likely to require manufacturers to stress healthy-living solutions Senior consumers (60+) are heavy consumers of soup and are brand loyal. This segment has growing health concerns and is looking for low sodium, fiber-enriched options. These products, however, are un appealing to younger consumer groups. High growth in "convenience" categories above are trend consistent with working moms Refrigerated and frozen soups are being branded by names associated with healthier fare like Panera Bread and Harry's Fresh Foods Supermarkets sold 62.9% of category Soup Consumption by Household 1.4 cans, average consumed per week per US household Consumers, 18-24, average 2.1 cans per week, 48% eat dry soup 78% eat wet soup High in com e consumers, 25-34, consume 40% of deli soups Competition: US $6.4 Billion Soup MarketBrannigan's Ready to Eat (RTE) Market Share Wet RTE Condensed RTE Brannigan's Foods 39.8% 58.6 63.4 General Mills 24 15 12 Unilever 7 5 2 Other 13 3 Private Label 15.4 18 22 Market share data do not include "deli soups." Premade "deli soup" poses a threat to packaged soup. 35% of respondents buy from supermarket deli sections. Consumers believe that deli soups are fresher and healthier. They clearly provide a "fast, simple" meal. Consumer Information 38% of consumers eat as a snack millennials (age 15-30) with $25-49 income most likely to do so 9 1% of consumers agree that canned soup is good to keep in the pantry 55% say that they or someone in their household eats soup year round 86% are more likely to eat soup when the weather is cold 5 1% use soup as a cooking ingredient 78% agree that soup is a healthy/low calorie option diet 61% of purchasers take low sodium into account when purchasing Products New Products Introduced (Industry Total) 2010 2011 Wet Soup 236 2 17 Dry Soup 79 56 Benefit Claims: In order of most used Microwavable Ease of use No additives or preservatives All natural Low fat Flavors: Southwest and Mexican hot and cold soups made up 11% of new products Asian soups made up 8% of new productsAnalyst's comments regarding new products Brannigan's new product success rate of 7% parallels the general food industry. The low-sodium products introduced over the past five years now make up around 10% of the division's RTE soups, but have only allowed for some price increases. They have not increased soup consumption overall. These new items have not resulted in increased retail shelf space for Brannigan. Brannigan's long effort to break into dry soups -- most recently with a microwavable soft pouch package -- has failed to pay back the $15MM investment in it. Refrigerated and frozen soups are in channel locations that Brannigan has been unable to penetrate due to retailer reluctance to cede additional store space to the brand. Strategic Challenges Sales ofBrannigan RTE Soups* $ millions Ready to Eat Condensed Soups 080 Ready to Serve Wet Soup 1156 * Includes "Heart Healthy" low-sodium soups Cream of Mushroom, Chicken Noodle, and Tomato are the most popular flavors in RTE Soups, selling 2.5 billion cans per year -- 41% of all soup sold. Brannigan has 60% share of the RTE soup market; RTE soups and broths provide 78% of division's sales; 86% of its profits. Brannigan's RTE soups are mature products, in slow decline (1-2% per year in $s; 2-3% in volume) Consumers perceive Brannigan to be behind competitors in the following:**Health trends Diet claims Convenience offerings Flavors -- especially popular regional ones Seasonal products outside of cold weather ** 2010 Nielsen Survey Retailers perceive Brannigan to be: The category leader in soups Not innovative Less profitable than store brands and competitorsExhibit 2 Brannigan's Product Lines US Soups Division 2012 sales ($ millions) Traditional Ready to Eat (RTE) Soups Ready to serve wet soup $ 998 Condensed wet soup 917 Broths 414 New products, acquisitions last ten years Tipha's lines Low sodium RTE "Heart Healthy" 321 Annabelle's Fast n Simple 71 Dry soups and mixes 53 Other, including private label 199 Total 2973 Exhibit 3 Clark's Preliminary Forecasts Brannigan's Foods Consolidated Statement of Earnings US Soup Division Year: 2011 2012est 2013 est ( in millions) Net Sales of Brannigan's Foods worldwide 7330 7979 8230 Net Sales of US Soup Division 3034 2973 2913 Less: Cost of goods sold 1669 1635 1602 Marketing, R&D and Selling Expense 425 416 408 Net Earnings 315 295 303 broken out ofm akin g and selling expense: Advertising & Promotion 189 178 170this trend. Clark noted with some satisfaction that Brannigan maintained the leading market share of shelf- stable soups and that three years of price increases had helped to keep profit from declining as much as sales. His division was responsible for more than half the profits of the company's U.S. divisions (40% of sales) and he wasn't going to back off his growth goals of in creasing those profits by 3% next year. Clark's Challenge to His Reports Could his team help him come up with a focused, coherent plan for growth? Clark thought back to the four strategic challenges he had presented to them: 1. Can new benefits be added to the current lines to increase their growth and profitability? N Does an acquisition make sense to strengthen or diversify our lines? 3. What new products might we develop internally that address the health and convenience trends? Or do we have enough new products already that can reverse the slide if they are properly marketed? 4 What marketing strategy should be employed in reference to each of the above and how much should be put behind the drive for next year versus what we should invest for our long-term objectives? Clark wasn't certain that these four options were exhaustive, but they were sure to surface the best ideas his team could come up with. To anchor their thinking in financial reality, he had also included his preliminary forecast for sales, marketing costs, and net income for next year (Exhibit 3). Now Clark read through the messages from the four people he most depended upon: Srikant Tipha, Director of the Simple Mealsunit; Claire Mackey, Director of Finance and Planning; Anna Chong, Chief Innovation Officer; and Bob Pugh, Director of Sales and Marketing. Invest in the growing sectors From: tiphas@brannigan.com To: clarkb@brannigan.com Hi Bert JJ's Report is spot-on. We need to continue to reinforce the strategy we've been following in the past few years by upping the investments in the on-trend winners in the growing categories of dry soups, healthier soups, and fast meals. Increasing our investment in these soups will have a positive impact on our brand image, bringing it into the 21st century, as well as driving long-term growth. I believe the Fast & Simple meal-in-a-pouch soups line that we purchased from Annabelle's Foods several years ago is finally on the right track. Sales are growing at 12% per year because the line addresses the needs of working mothers and professionals looking for a fast but healthy meal. The low-sodium Heart Healthy soups introduced several years ago are also gaining traction and market share, as shown in the report, as they are well positioned to address the concerns of over-50 consumers.The dry soups category is also expanding. We only have a few offerings at this point, but they are very promising. The dry soup mixes also help us address the retailer's desire to squeeze more prot from our shelf space. Two dry mix packs can be sold in the space of one can, increasing the sales potential by180%. Here's a plan: 1. Reinforce awareness of our new items and induce trial by' Increasing the advertising investment in the Fast :2 Simple soup meals and the HearrHeafrhy soup line. We' re somewhat behind our competitors in this space, but our retailer and consumer market strength should allow us to grow market share rapidly, ifwe spend appropriately. 2. Provide promotional couponing and sampling ofthe hot new avors, in particular the dry mix Gazpacho and the Teriyaki Beef Fast a Simple meal. The Gazpacho will provide an added bonus of' Increasing sales during the warmer months, decreasing seasonality. The Teriyaki Beef positions us in the fast growing Asian soups category. 3. Continue to promote dry soups, even ifthey cannibalize Ready-to-Eat (RTE) soups. l'm proposing an increase in our advertising and promotion spending of$18 million (the numbers below are based on the forecast you provided). Exhibit 3 This should help stop the slide in sales and market share, although it will reduce next year's prots. We should make this move for the long-term revitalization ofthe brand and to gain leadership in the growing categories. Present division sales this year with additional advertising spending next year 2973 2954* ($2913 forecast) Adv promo 178 188 Op income 295 297 "Half my proposed sales increase comes from the Heart Healthy soups and half from the other items listed above. Let's talk this over when convenient. Srikant Tipha Category Manager - Simple Meals, Heart Healthy Soups, Dry Soups Srikant had done a good job integrating Annabelle's products into Brannigan line in the face of some serious challenges. His "healthier" new products also seemed to be gaining traction. But Clark worried that spending more on these small lines might not produce the sales Srikant projected. He made a note to ask Srikant what sales had to be hit to reach breakeven on the additional advertising spend. Clark also sensed that due to the competitive activity in these areas that Tipha's products had lower gross profit than the core products. Clark also feared that these "on-trend" initiatives may never become large categories for Brannigan's. Most consumers knew they should eat more healthy foods, but with close to 70% of the US overweight it was obvious that few actually were changing their eating habits. Clark was also concerned about having to revise profits down for 2013 if he followed Srikant's advice. He knew that CEO John Wilson was going to demand an airtight justification for it. Wilson was under increasing pressure from the board and the stockholders and he would probably be unwilling to give up any profit. Clark made an other note to ask Srikant what sales had to be for operating in come to equal his projections for 2012 Clark's also thought that chasing the trends may not amount to a viable long term strategy in spite of Srikant's comments to the contrary. He picked up the next email. Acquire product lines to complement the core in growing sectors From: mackeyc@brannigan.com To: clarkb@brannigan.com Bert: The DeGennaro report indicates that a number of small competitors are offering healthier and more convenient soups, as well as flavors rapidly gaining in popularity, such as Mexican and Southeast Asian, where we have little presence. Here are several companies that we should consider acquiring to bring Brannigan into these categories. I particularly like Red Dragon Foods. Roarin' Cajun Foods Baton Rouge, LA. Key product: ten-bean dry mix soup. MSG and sodium free. Key customer: Whole Foods. $18 million sales. Estimated EBITDA for 2011: $2.8MM Would provide entry into WF if we do not use the Brannigan's brand. Red Dragon Foods Los Angeles. Key products: Southeast Asia and Chinese soups. Key customers: Safeway, Ralph's chains. $36 million sales. Estimated EBITDA:$4.2MM Would give us entre into Asian flavors and has the potential for numerous additional products. Brannigan's brand could be incorporated reducing the advertising and promotional investment required by 55%. Brothers Gourmet Rhinebeck, NY. Upscale soups centered on classic "deli-like" products such as Brooklyn Chicken Noodle. Key customer: Pathmark $12 million sales. Estimated EBITDA: $3.4MM Would bring higher priced, higher margin items into our line. Brothers brand should likely be maintained.Speculating, the price for any ofthese would likely be in the six to seven times EBITDA range. Interest rates are about 4% now so debt service would be low and would not impact prot signicantly. Of course, with the recent down year, any negative impact on prot is going to be scrutinized. My best guess is that any of these acquisitions will add around 1.5 to 3.5% to our sales within ve years if we invest appropriately in marketing them. Cannibalization is hard to project. Red Dragon, as an example, should cannibalize less than 0.3% of our total sales ifwe were to acquire it and keep its brand. Let me know ifyou would like to begin due diligence on any of the above companies... Claire Mackey, Director of Finance & Planning Clark had vivid memories of the acquisition of AnnabC/b's Foods soups' division five years ago. It was supposed to accelerate the growth of the division's 5352' 63 SNIPp/C categoly. but folding nnebcc's line into existing offerings had been a nightmare. Its plant was plagued with production miscues as efforts to take Annabcc's products into major retail channels ovelwhelmed its capabilities. The acquisition did add volume to the division. though. and Brannigan's customers eventually responded favorably. but the projected breakeven of two years turned into five. Clark knew that Brannigan needed presence in these new flavors and the healthier soups the companies Claire identified offered. Acquisition seemed like an expedient way to obtain it. The acquisition prices seemed reasonable. but the issue of bran ding and marketing investment was complex. Clark felt that a minimum of 30% of sales would need to be spent for advertising and promotion if the acquired company's brand was continued. That percentage would have to continue for at least three years in order to grow the acquired line. The cost of advertising and promotion would be about half that number if the Brannigan's brand could be used instead ofthe acquired brand. A plus was that the cost of the acquisition would be reflected in the balance sheet. Only interest and depreciationiamortization would affect operating income. Also. Brannigan's could provide 111anufacturing and operating synergies that should increase gross profit margins about 10% within two years. Clark knew the companies Ma ckey listed operated with about the same gross profit margins Brannigan's enjoyed in its core lines (45%) and their brands all commanded higher per unit selling prices than Brannigan's core products. Cannibalization was a critical consideration. Clark felt Mackey's estimate was shy by half. Moreover. Brannigan faced a paradox from its retail partners. Most large retailers were t1ying to consolidate the numb er of vendors they dealt with. and from that perspective they would view Brannigan's purchasing a small company favorably. However. most retailers were wary ofhaving their larger vendors. like Brannigan. gain shelf space. Clark knew that ifa small company were acquired retailers would exert pressure on Brannigan to take out some of its weaker products so that Brannigan would have no net gain in shelf space after the acquisition. This same set ofretailer concerns applied to new products. IfBrannigan's kept using the acquired brand name. the pressure from retailers to give 11p shelf space would be less. however. Clark estimated that maintaining the acquired brand. rather than changing to Brannigan's brand. would allow Brannigan to keep more than 90% of the acquired brand's shelf space. reducing cannibalization by 70% The marketing costs would be much higher. though. as outlined above. Against all these factors. Clark knew that the company was looking for a minimum of10% ROI after five years of sales. Bert moved on to the next email from his ChiefInnovation Officer --------------- the head ofR&D. Invest in organic growth from internally developed new products From: chonga@brannigan.com To: clarkb@brannigan.com Hl Bert The soup report is dead on in highlighting consumer trends that we need to get in front of and lead rather than follow. Brannigan is a 100-yearold line with mature products in mature categories. Maybe we can get more boomers back to green bean and mushroom soup casseroles but it doesn't seem likely, given what we know about the market trends. That said, I sure hope we don't think the best way to grow is to buy another barking dog just because they have some snappy products that we could easily duplicate. Here are my suggestions to reverse the market share and prot decline and move growth back to 3-4%: . Milk our cash cows and invest in the rising stars. Srikant and l are in complete agreement that we should increase the advertising and promotional support for our new products. It is by far the most protable way for us to go long term. . Avoid thinking that we can short circuit the new product development process by just buying some small companies. Developing the products internally is far less expensive and ultimately much more protable. Look at the struggle Srikant has had with the Annabelleis Foodsproducts. - Several new products are ready to launch that have tested well with consumers. | recommend increased spending for the new Ready-to- Eat (RTE) products from R&D including: \"To-Your-Health Chicken Noodle\" and \"Fast-and-Simple Mediterranean Tomato Basil.\" These reinforce our traditional strengths and strongly address consumers' changing needs. . Up the R&D budget from $14 million to $19 million to increase the pace of new product creation and development. Here are several projects in development we feel have great potential: - Packaged \"deli soups\" - Simple Healthy \"weight watchers\" soups with a diet component - \"Active Lifestyles\" soups and broths - Convenient \"Great Meals\" related to, but different from, soups such as a dry or wet macaroni and cheese mix to be added to a pasta by the consumer. These concepts squarely address the opportunities outlined in Julian's report and they could add signicant growth and prot to our division. Here is an example of how I see the investmentr'return requirements to launch ten \"typical\" new products, ultimately ending up with one big new product winner (sales of more than 1% of the division's within two years):* $ in millions 2012* 2013 2014 2015 Development R&D $2 Marketing testing and launch 6 On-going support 5 3 Net new volume 15 24 30 Incremental gross prot 7 12 16 * 2012 RED budget of $14lvllvl covers development of numerous products. Brannigan would likely have more than 100 in various stages of completion conception. marl~.et research. testing. and launch. The $2lvllvl shown is an "estimate" of development costs for 10 products. The other expenses shown are estimates forthe same 10 products. Please call to discuss. I hope we can move quickly to increase support for our vital new product development efforts. Anna Chong, Chief Innovation Ofcer Clark considered all the new product bombs he'd lived through during his career. along with the ve1y low success rate for new products for the industry as a whole. outlined in the report. He thought Anna had some promising ideas. though. and the report did highlight consumer desire for innovation in the categ01y. The new RTE avors Anna proposed built on the most popular soups Brannigan offered and would permit a price increase of approximately $.10 a can. He thought this could result in an incremental net earnings increase of 11p to $13 million after spending 6% ofthe proposed advertising budget just for these specific new products. significantly more costly than shown in Chong's chart. Possibly. 11p to $6 million in additional gross profit might be achieved if additional shelf space could be obtained for the new products. Clark felt that gaining shelf space for the new RTE products had about a 5% chance of occurring and was therefore ve1y unlikely. But the profit gain 'om the price premium for the new RTE soups. even if all the sales were cannibalized (ve1y likely if Brannigan has to take out core product to put in the new RTE soups) 'om Brannigan's core RTE soups. had a 90% chance of occurring. As far as increasing R&D investment. he was wa1y of the continued optimism Anna and her team projected. Actually calculating new product investment returns was complicated by a number offa ctors. It was very hard to assign precise R&D costs to specific products that made it out of the lab to launch, as only a few did. Chong indicated that from about 100 ideas, ten new products were launched into the marketplace. This cost about $8MM per year as shown on the chart. Clark hadreviewed data showing that of these ten new products, nine lasted in the market for less than two years. One of ten, though, would reach Brannigan's threshold for success outlined above ($30MM in sales two years from launch). Total profit from the sales from the nine new products that "failed" usually exceeded the amount invested in their development, however, even including the marketing expenses for them. The larger "cost" to Brannigan concerned its retailers who were becoming increasingly intolerant of the cost to them of bringing in new products with short life-cycles that failed to meet their sales and profit expectations. Stocking fees, returns, and other charges that could be as much as a $1000 a store for each new product brought in and subsequently removed were a constant for Brannigan. And, Clark had no idea how to calculate the additional cost of the loss of retailers' goodwill. Clark reached for the last email. Invest in the core From pughb@brannigan.com To: clarkb@brannigan.com Bert, We've worked together a long time so I'll shoot straight. I hope the report is a wake-up call. The Brannigan Soups core canned and RTE soups account for 64% of division sales and $210MM, or 71%, of the division's total profit. We have to act. I know the team doesn't necessarily see things my way, but we've been milking the core RTE wet soup lines to fund new products and acquisitions for the past five years. That strategy may have MBA logic behind it, but it's not working. To keep profits up, our price increases on core products have been raised an average of 2% per year for the past five years. Now we're getting push-back from our major customers. Wal-Mart's private label soups have grown over 5% per year during the past five years while our shelf space in their stores has decreased by 3% there in that period. We can probably maintain a 15% to 20% price premium, but our 30%-higher pricing "gap" is just too large for consumers to ignore. At the same time, we've cut back advertising and promotion spending for our core products in order to meet the yearly profit goals. These actions have resulted in a reduction in perceived "value" by our consumers and a diminution of the brand, a direct cause of our sales decline. I signed off on this. The acquisition of Annabelle's isn't living up to expectations, but it's not a disaster either. New products are another matter. The Heart Healthy line was a big investment and it has done little except to cannibalize our core products, as our market share continues to slide. We put these new products out there and the first thing our key retail partners ask us to do is take something out to make room for them on the shelf. As many a parent has put it, "You need to dance with the one who brought you." We need to stop flirting with tiny companies and niche products and instead defend and fortify what the company has built over decades. Here are the actions | recommend. The time to implement them is now: Take a five cent price-per-can cut on the core ready-to-eat wet soups. Increase the A&P budget by $20MM to restore fair share support for the brand. Bring back the Brannigan "Boys and Girls Love Soup" campaign to attract younger customers to the core RTE soups. Bring the manufacturing plants into the 21* century to rationalize what the price cuts will cost. Marcus (Operations Senior VP) indicated that would require about $22 million in capital. Wholesale cost per can of RTE soups was approximately $1. 14 in 2011 Let the sales force know in no uncertain terms that we're concentrating on growing the core Brannigan Soups as the number one goal this year.With those actions, and assuming commodities prices are stable, operating income decline can be halted while we increase the sales volume and recapture market share. Here's my forecast: (millions) this year next year Cans of soup RTE est 1,669 1800 - 2000 Advertising promotion $189 $209 We've worked too hard over the past twelve years to let the big dog prot engine slip thher. Let's talk. Bob Pugh, VP Sales and Marketing, Brannigan Soups Clark thought Bob's view was shared by Brannigan's senior management and much ofthe sales force. He had serious reservations about cutting price. however. Retailers would favor it. of course. but would it really induce consumers to eat more soup from Brannigan? Clark glanced at the rain outside and thought about the strong team he'd surrounded himself with. He reflected on their proposals and wondered whose ideas were most likely to provide the short-term numbers so desperately needed and which would strengthen the long-term direction of the company and its venerable brand. He typed a few points onto his computer thatneeded to be clarified from ea ch proposal: worst case. prob able. best case. He thought ab out the decision factors that might be pertinent and typed a quick list: Volume vs. profit Short term versus long term Brand equity vs. Brand constraint Category trend vs. performance Health Convenience Risk of options Opp ortun ities and resource limits W11 at we do well Com p etition John Wilson was expecting a formal budget and action plan on his desk next week. The plan had to detail Clark's forecast for next year along with a three year overall sales and operating profit projection. Clark wondered how his forecast might change in light ofhis manager's proposals

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance