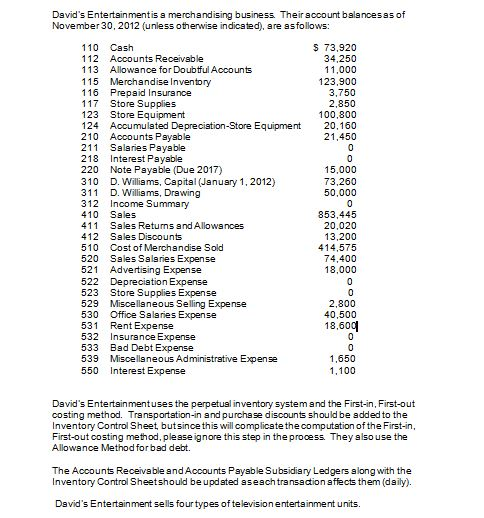

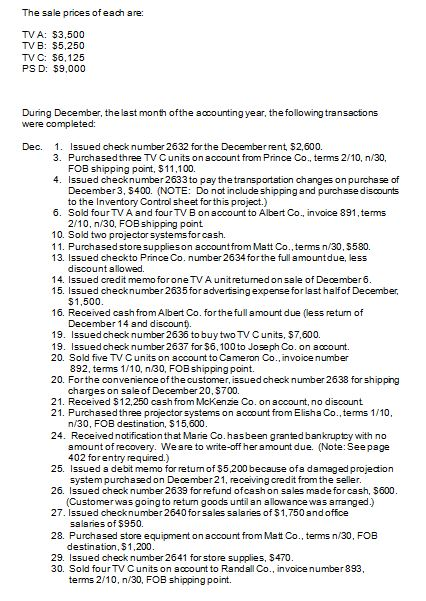

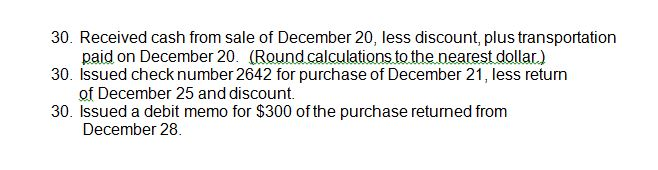

Question

Journalize and post the adjusting entries. Adjustment Data: . Merchandise inventory on December 31 $90,800 b. Insurance expired during the year 1,250 c. Store supplies

Journalize and post the adjusting entries.

Journalize and post the adjusting entries.

Adjustment Data:

. Merchandise inventory on December 31 $90,800

b. Insurance expired during the year 1,250

c. Store supplies on hand on December 31 975

d. Depreciation for the current year needs to be calculated. The business uses

the Straight-line method, the store equipment has a useful life of 10 years

with no salvage value. (NOTE: the purchase and return will not be included

as the dates of the transactions were after the 15th of the month).

e. Accrued salaries on December 31:

Sales salaries $1,400

Office salaries 760 2,160

f. The note payable terms are at 8%, payment is not being made until Jan. 3, 2013. Interest must be recognized for one month.

g. Net realizable value of Accounts Receivable is determined to be $27,950.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Accounting

Authors: Belverd E. Needles, Marian Powers and Susan V. Crosson

12th edition

978-1133603054, 113362698X, 9781285607047, 113360305X, 978-1133626985