JUST ANSWER PARTS L,M,N,O AS PER CHEGG RULE

JUST ANSWER PARTS L,M,N,O AS PER CHEGG RULE

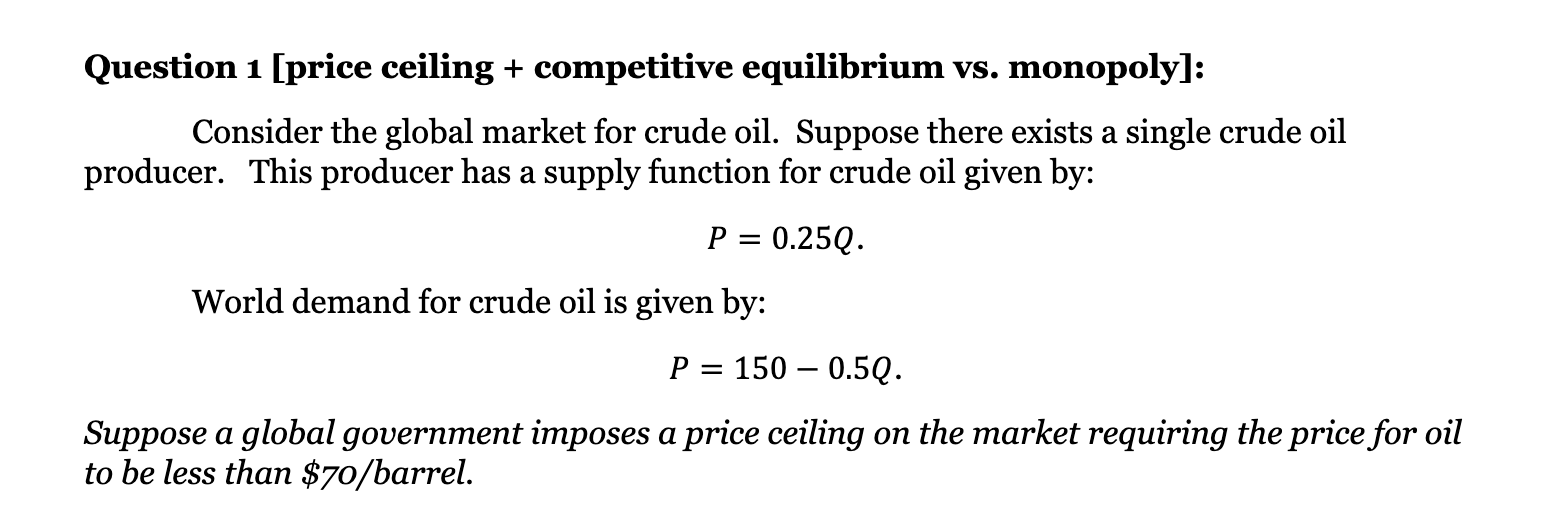

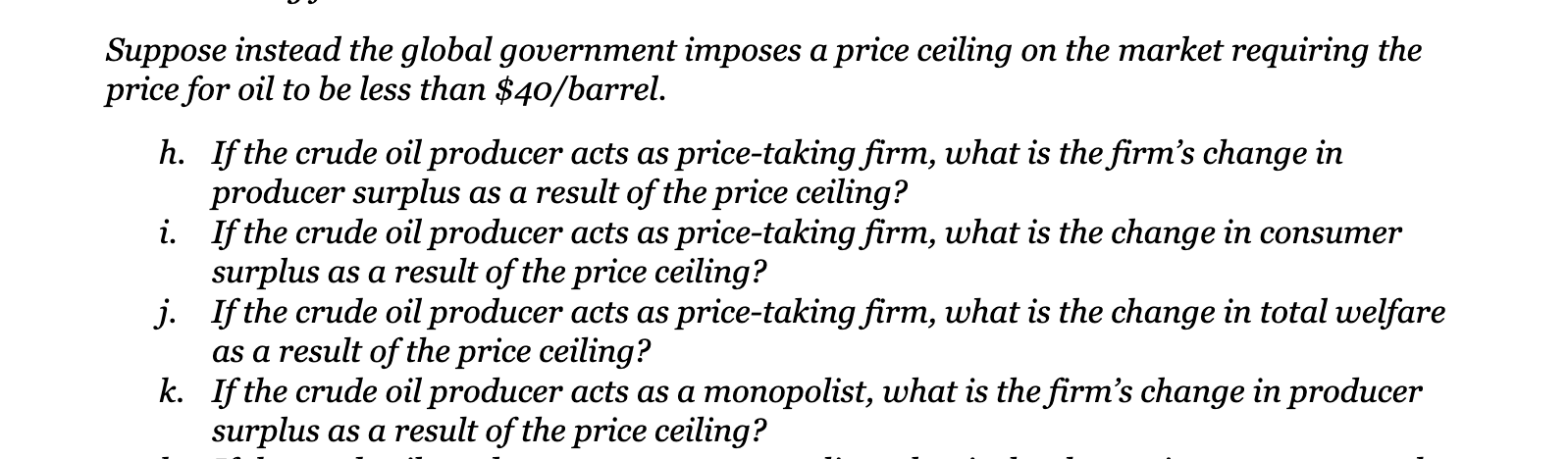

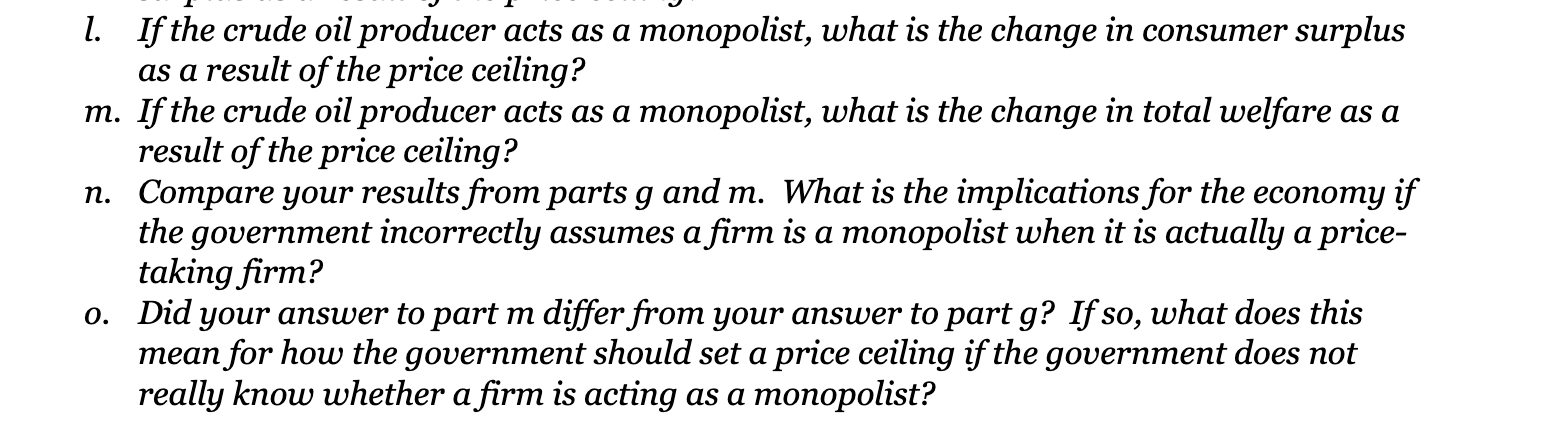

Question 1 [price ceiling + competitive equilibrium vs. monopoly]: Consider the global market for crude oil. Suppose there exists a single crude oil producer. This producer has a supply function for crude oil given by: P = 0.250. World demand for crude oil is given by: P = 150 0.5Q. Suppose a global government imposes a price ceiling on the market requiring the price for oil to be less than $70/barrel. Suppose instead the global government imposes a price ceiling on the market requiring the price for oil to be less than $40/barrel. h. If the crude oil producer acts as price-taking firm, what is the firm's change in producer surplus as a result of the price ceiling? i. If the crude oil producer acts as price-taking firm, what is the change in consumer surplus as a result of the price ceiling? j. If the crude oil producer acts as price-taking firm, what is the change in total welfare as a result of the price ceiling? k. If the crude oil producer acts as a monopolist, what is the firm's change in producer surplus as a result of the price ceiling? 1. If the crude oil producer acts as a monopolist, what is the change in consumer surplus as a result of the price ceiling? m. If the crude oil producer acts as a monopolist, what is the change in total welfare as a result of the price ceiling? n. Compare your results from parts g and m. What is the implications for the economy if the government incorrectly assumes a firm is a monopolist when it is actually a price- taking firm? 0. Did your answer to part m differ from your answer to part g? If so, what does this mean for how the government should set a price ceiling if the government does not really know whether a firm is acting as a monopolist? Question 1 [price ceiling + competitive equilibrium vs. monopoly]: Consider the global market for crude oil. Suppose there exists a single crude oil producer. This producer has a supply function for crude oil given by: P = 0.250. World demand for crude oil is given by: P = 150 0.5Q. Suppose a global government imposes a price ceiling on the market requiring the price for oil to be less than $70/barrel. Suppose instead the global government imposes a price ceiling on the market requiring the price for oil to be less than $40/barrel. h. If the crude oil producer acts as price-taking firm, what is the firm's change in producer surplus as a result of the price ceiling? i. If the crude oil producer acts as price-taking firm, what is the change in consumer surplus as a result of the price ceiling? j. If the crude oil producer acts as price-taking firm, what is the change in total welfare as a result of the price ceiling? k. If the crude oil producer acts as a monopolist, what is the firm's change in producer surplus as a result of the price ceiling? 1. If the crude oil producer acts as a monopolist, what is the change in consumer surplus as a result of the price ceiling? m. If the crude oil producer acts as a monopolist, what is the change in total welfare as a result of the price ceiling? n. Compare your results from parts g and m. What is the implications for the economy if the government incorrectly assumes a firm is a monopolist when it is actually a price- taking firm? 0. Did your answer to part m differ from your answer to part g? If so, what does this mean for how the government should set a price ceiling if the government does not really know whether a firm is acting as a monopolist