Answered step by step

Verified Expert Solution

Question

1 Approved Answer

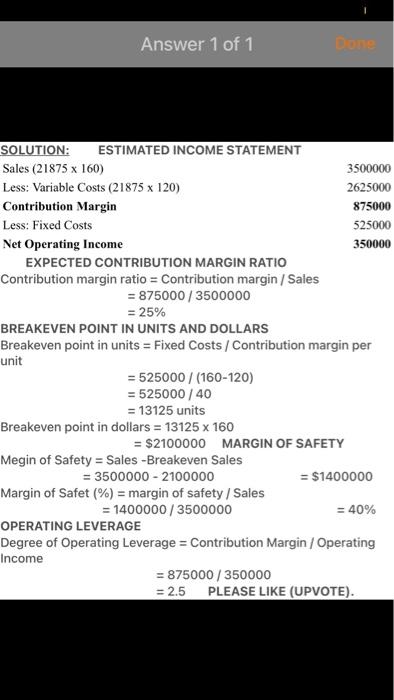

just do number 4 the cost volume profit chart indicating break even sales Chapter 19 Cost-Volume-Profit Analysis PR 19-6A Contribution margin, break-even sales, cost-volume-profit chart.

just do number 4 the cost volume profit chart indicating break even sales

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Your Windows Infrastructure Intranet And Internet Security A Practical Audit Program For Assurance Professionals

Authors: Nwabueze Ohia

1st Edition

1521804133, 978-1521804131