Answered step by step

Verified Expert Solution

Question

1 Approved Answer

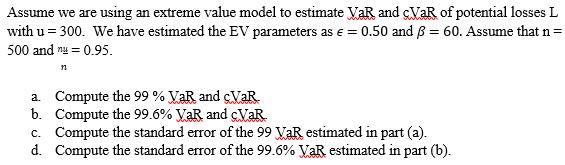

Just the manual solution, please. Thank you! Assume we are using an extreme value model to estimate VaR and cVaR of potential losses L with

Just the manual solution, please. Thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Commodity Futures And Forex Technical Analysis October To November 2020

Authors: Ascencore Site

1st Edition

979-8693096387