Answered step by step

Verified Expert Solution

Question

1 Approved Answer

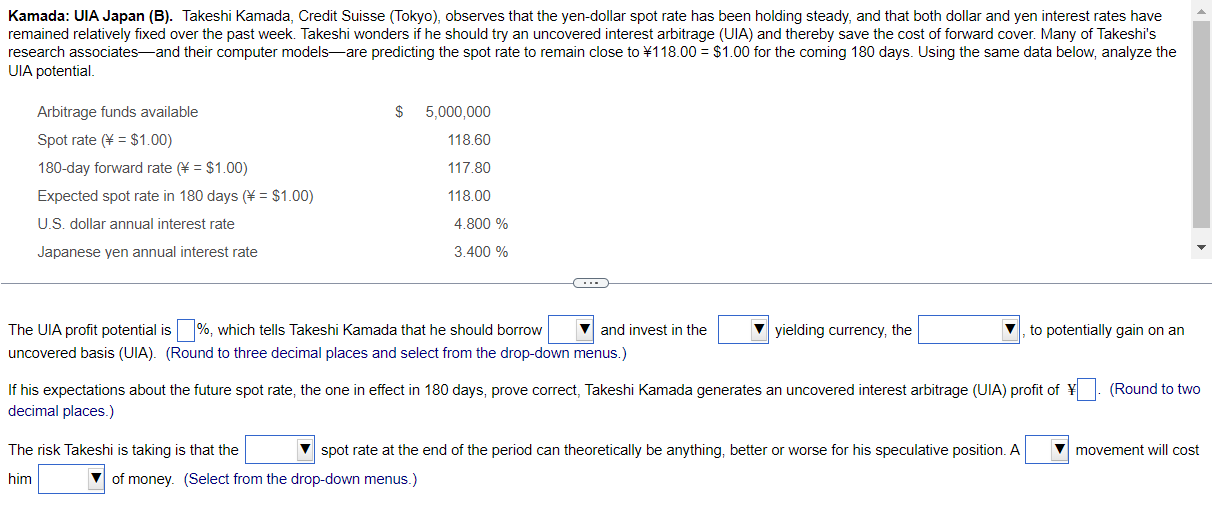

Kamada: UIA Japan (B). Takeshi Kamada, Credit Suisse (Tokyo), observes that the yen-dollar spot rate has been holding steady, and that both dollar and yen

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The History Of Lloyd S And Of Marine Insurance In Great Britain

Authors: Frederick Martin

1st Edition

1421206269, 978-1421206264