Answered step by step

Verified Expert Solution

Question

1 Approved Answer

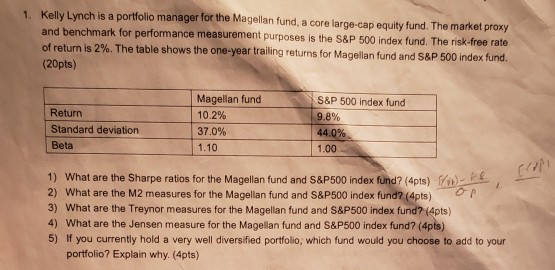

Kelly Lynch is a portfolio manager for the Magellan fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is

Kelly Lynch is a portfolio manager for the Magellan fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500 index fund. The risk-free rate of return is 2%. The table shows the one-year trailing returns for Magellan fund and S&P 500 index fund (20pts) 1. S&P 500 index fund Return Standard deviation Beta Magellan fund 10.2% 37.0% 1.10 1.00 1) What are the Sharpe ratios for the Magellan fund and S&P 500 index fund? (4pts) 2) What are the M2 measures for the Magellan fund and S&P500 index fund? (4pts) 3) What are the Treynor measures for the Magellan fund and S&P500 index fund? (4pts) 4) What are the Jensen measure for the Magellan fund and S&P500 index fund? (4pts) 5) If you currently hold a very well diversified portfolio, which fund would you choose to add to your portfolio? Explain why. (4pts)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jack Kapoor, Les Dlabay, Robert J. Hughes

11th edition

9781259278617, 77861647, 1259278611, 978-0077861643