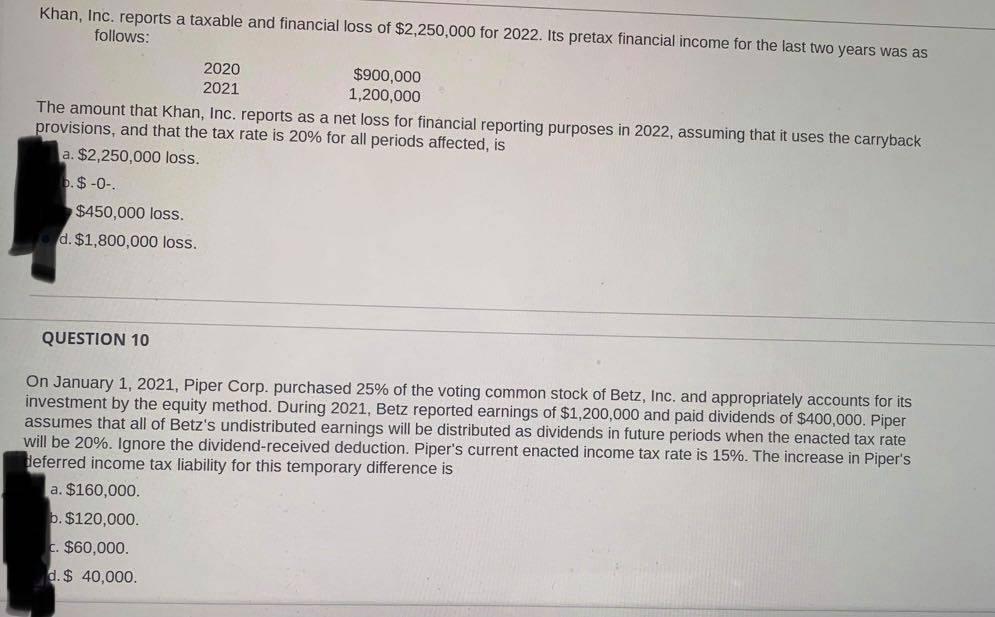

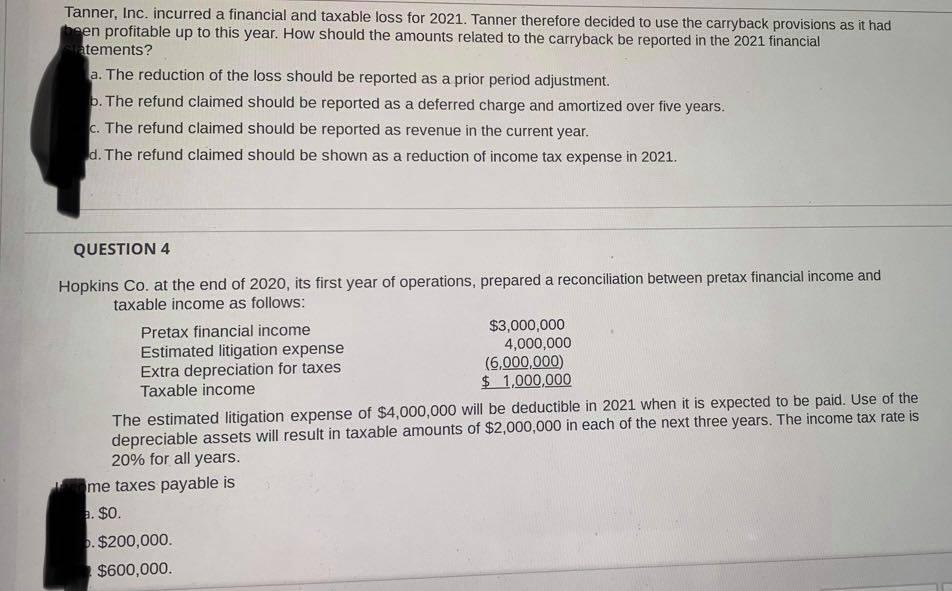

Khan, Inc. reports a taxable and financial loss of $2,250,000 for 2022. Its pretax financial income for the last two years was as follows: 2020 $900,000 2021 1,200,000 The amount that Khan, Inc. reports as a net loss for financial reporting purposes in 2022, assuming that it uses the carryback provisions, and that the tax rate is 20% for all periods affected, is a. $2,250,000 loss. b.$-0- $450,000 loss. d. $1,800,000 loss. QUESTION 10 On January 1, 2021, Piper Corp. purchased 25% of the voting common stock of Betz, Inc. and appropriately accounts for its investment by the equity method. During 2021, Betz reported earnings of $1,200,000 and paid dividends of $400,000. Piper assumes that all of Betz's undistributed earnings will be distributed as dividends in future periods when the enacted tax rate will be 20%. Ignore the dividend-received deduction. Piper's current enacted income tax rate is 15%. The increase in Piper's deferred income tax liability for this temporary difference is a. $160,000. b. $120,000. C. $60,000 d. $ 40,000 Tanner, Inc. incurred a financial and taxable loss for 2021. Tanner therefore decided to use the carryback provisions as it had been profitable up to this year. How should the amounts related to the carryback be reported in the 2021 financial atements? a. The reduction of the loss should be reported as a prior period adjustment b. The refund claimed should be reported as a deferred charge and amortized over five years. C. The refund claimed should be reported as revenue in the current year. d. The refund claimed should be shown as a reduction of income tax expense in 2021. QUESTION 4 Hopkins Co. at the end of 2020, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $3,000,000 Estimated litigation expense 4,000,000 Extra depreciation for taxes (6,000,000) Taxable income $ 1,000,000 The estimated litigation expense of $4,000,000 will be deductible in 2021 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $2,000,000 in each of the next three years. The income tax rate is 20% for all years. me taxes payable is 3. $0. D. $200,000. $600,000 Khan, Inc. reports a taxable and financial loss of $2,250,000 for 2022. Its pretax financial income for the last two years was as follows: 2020 $900,000 2021 1,200,000 The amount that Khan, Inc. reports as a net loss for financial reporting purposes in 2022, assuming that it uses the carryback provisions, and that the tax rate is 20% for all periods affected, is a. $2,250,000 loss. b.$-0- $450,000 loss. d. $1,800,000 loss. QUESTION 10 On January 1, 2021, Piper Corp. purchased 25% of the voting common stock of Betz, Inc. and appropriately accounts for its investment by the equity method. During 2021, Betz reported earnings of $1,200,000 and paid dividends of $400,000. Piper assumes that all of Betz's undistributed earnings will be distributed as dividends in future periods when the enacted tax rate will be 20%. Ignore the dividend-received deduction. Piper's current enacted income tax rate is 15%. The increase in Piper's deferred income tax liability for this temporary difference is a. $160,000. b. $120,000. C. $60,000 d. $ 40,000 Tanner, Inc. incurred a financial and taxable loss for 2021. Tanner therefore decided to use the carryback provisions as it had been profitable up to this year. How should the amounts related to the carryback be reported in the 2021 financial atements? a. The reduction of the loss should be reported as a prior period adjustment b. The refund claimed should be reported as a deferred charge and amortized over five years. C. The refund claimed should be reported as revenue in the current year. d. The refund claimed should be shown as a reduction of income tax expense in 2021. QUESTION 4 Hopkins Co. at the end of 2020, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $3,000,000 Estimated litigation expense 4,000,000 Extra depreciation for taxes (6,000,000) Taxable income $ 1,000,000 The estimated litigation expense of $4,000,000 will be deductible in 2021 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $2,000,000 in each of the next three years. The income tax rate is 20% for all years. me taxes payable is 3. $0. D. $200,000. $600,000