Answered step by step

Verified Expert Solution

Question

1 Approved Answer

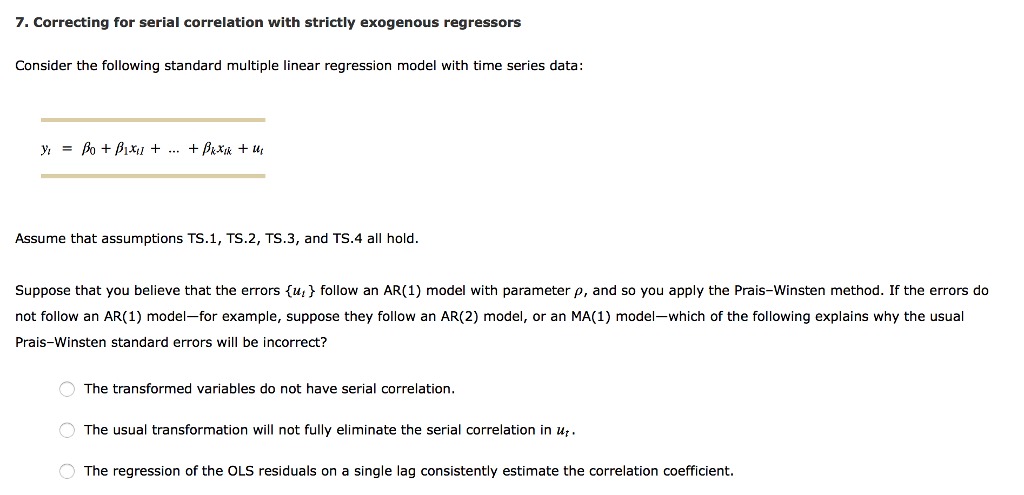

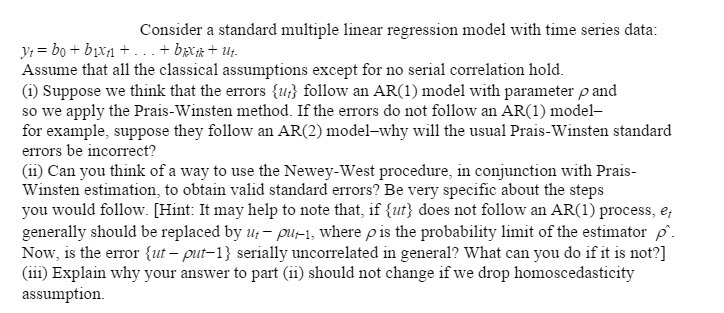

Kindly help me solve this 7. Correcting for serial correlation with strictly exogenous regressors Consider the following standard multiple linear regression model with time series

Kindly help me solve this

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Society, Economy, Religion And Festivals Of Tiwas In Assam

Authors: Bandana Baruah

1st Edition

9351288633, 9789351288633