Kindly help

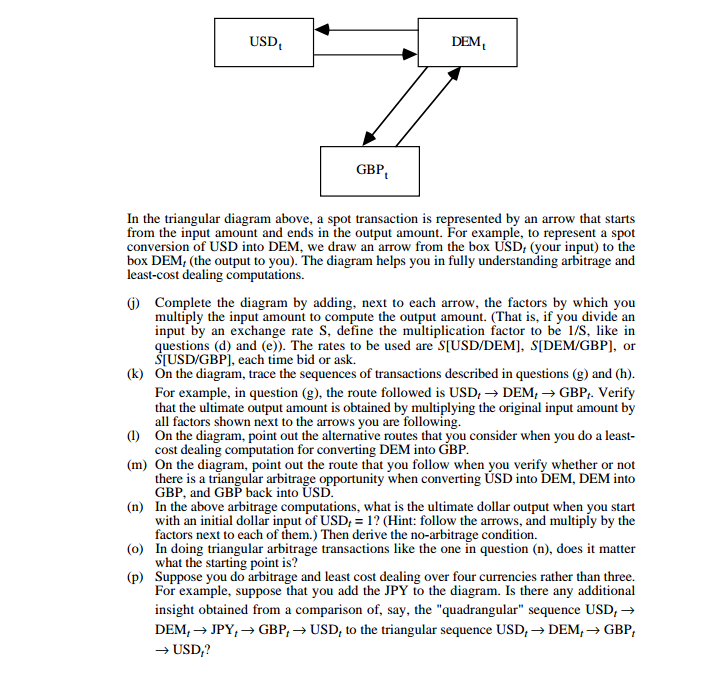

Question VIII (25 points - Arbitrage in infrastructure) Read the following Economist article about stock exchanges in Europe. Then answer the questions that follow. Stock Exchanges in Europe The Hunt For Liquidity Jul 28th 2001 From The Economist print edition Competition among Europe's stock exchanges is Liquidity will thus be key in determining the winners keener, thanks to bear markets, new technology and and losers in this battle of the bourses. And liquidity the euro. Liquidity and trading costs will decide who comes with size, one of the reasons why stock wins. exchanges are often described as natural monopolies. On this measure, the LSE is still some AS BUSINESSES go, stock exchanges are rather curious. They are under pressure to consolidate, yet way in front of its rivals. It attracted more new listings last year than either Deutsche Borse or Euronext, trading platforms proliferate. Considerable with higher turnover (see chart). Still, London will economies of scale exist in their activities, yet tiny have to pedal hard to keep ahead, for continental upstarts and small national exchanges can do well. rivals as well as young upstarts are catching up. On Exchanges ought to be run like multinational its first day of business, Virt-X, an electronic companies, yet they are too often still the financial exchange launched in July, pinched 23% of all markets' equivalent of the national football team. trading in Britain of the shares of GlaxoSmithKline, a America has only three national and five regional drugs company. exchanges, but Western Europe still has more than 30 stock exchanges. Most will probably not survive A fight for the pie the next ten years. Some will be taken over, others Turnover on European stockmarkets, % of total may simply shut down. And one or two are likely to year to June 2001 emerge as dominant forces in the cross-border trading of blue-chip shares, the highest-profile and most lucrative bit of the industry. Deutsche Borse 14.6 - This race for the top spot is different from competition in other businesses. For a start, many exchanges in Europe are only now beginning to be Euronext Total: London 19.1 43.2 run as proper companies, rather than as member- C6,494bn dominated public utilities. The three biggest, the London Stock Exchange (LSE), Deutsche Borse and Other Euronext (the merger of the Paris, Amsterdam and 17.2 Brussels bourses), have just shed their mutual L Swiss exchange 5.1 structure. The LSE became a fully listed company on Source: Federation of European Stock Exchanges July 20th, Euronext went public at the beginning of the month, and Deutsche Borse made its Given the steep increase in trading activity over the stockmarket debut in February. past few years, there ought to be liquidity aplenty. More than ever, exchanges will now have to find out Cross-border equity portfolio flows in the world's what exactly their customers want. This ought to be developed markets are reckoned to have quintupled self-evident: a cheap and effective trading system. in the past five years, to $1.1 trillion. European flows But it is not that simple. Certainly, those who trade have grown by even more. The launch of the single on stock exchanges want low direct costs-that is, currency has set in train a huge reshuffling of brokers' commissions and fees for confirming a portfolios. Institutional investors in Europe now tend trade, for clearing it (registering a share's new to judge sectors almost entirely from a pan-European ownership) and for settling it, when money changes not a national perspective. hands. Yet they also want low indirect costs, in the Yet liquidity is by no means abundant. Cross-border form of narrow dealing spreads-that is, the equity flows appear vulnerable to sudden drying up. difference between buy and sell prices. The more This has been especially true since Russia's default liquid a market is, the narrower the spreads and the on its bonds in August 1998, followed by the collapse less prices are moved by quantities of orders. of Long-Term Capital Management, a hedge fund. Liquidity, as one trader puts it, is "what gets business Subsequently, international investment banks and away". It is the best measure of a stockmarket's cost- asset managers have only slowly recommitted risk effectiveness. capital to trading equities.MS&E247s International Investments 8/18/06 Final Exam Page 15 of 16 Other, more structural, factors also point to a dearth the average cost at Virt-X is only euro2. Jiway offers of liquidity. The rise in the number of international retail brokers a one-stop shop for pan-European investors has led to a demand for tradable securities share-dealing and settlement for 6,000 different that is not matched by supply, notes Avinash shares. Persaud at State Street, an American bank. Liquidity Although it might make sense for stock exchanges to is squeezed by these investors' tendencies to act join forces, many bourses in Europe fiercely defend alike: models for managing short-term risk promote their turf, preferring to carry on independently. similar investment patterns. Merging exchanges allows liquidity to be pooled; it Still, while liquidity remains tight, trading costs have also offers the means for more efficient clearing and come down-mainly because computers are settlement. Here, the Germans and the British do not replacing people as trading is automated. However, see eye to eye. Deutsche Borse is all for alliances, though costs in Europe vary greatly, they are such as its union with the Vienna Stock Exchange, generally still high. Benn Steil, at the Council on but it does not want to give up its vertical "silo", which Foreign Relations in New York, puts this down to the includes its own clearing and settlement through heavy European use of intermediaries (that is, old- Clearstream. The LSE does not rule out mergers fashioned stockbrokers) when executing trades, and either-perhaps with Virt-X, or even with Liffe, to Europe's painfully high costs for clearing and London's derivatives exchange. But it wants to see settlement-which can be as much as ten times settlement systems consolidated, favouring a merger more than those in America. between Clearstream and Euroclear. Deutsche Low costs are the chief selling-point of the upstart Borse wants these to remain separate; one mainly exchanges in Europe. Thanks largely to their having settles equity trades, the other chiefly bond found more efficient solutions for clearing and transactions. settlement, Virt-X and Jiway, an electronic exchange Whether exchanges forge alliances or go it alone, for retail investors, are much cheaper than the the challenges of attracting and retaining liquidity will established bunch. Virt-X, for instance, offers a prove formidable. Cheaper technology allows trading "multi-settlement" system that encourages a certain systems to multiply. Traders can look instantly for the amount of competition on price between Euroclear, best prices. Orders can swiftly be re-routed. That Crest and SIS, the three big settlement agencies. means that exchanges with an apparently From a survey of market participants, Virt-X claims impregnable franchise can lose it almost overnight- that the average cost of cross-border equity trades in something that no longer makes for sound sleeping Europe is between euro10 ($8.50) and euro80, while for those who run them. a. (5 points) Define liquidity in the context of the article. b. (10 points) Discuss what makes one exchange more appealing than another from the companies' (customers') viewpoint. That is, if you are considering listing your company in one of the exchanges, what factors will attract you to a particular exchange instead of another one? Does the "critical mass" (i.e., the number of companies already listed on a particular exchange) matter in your decision? c. (10 points) Comment and elaborate on the following underlined segment in the title of the article: "Competition among Europe's stock exchanges is keener, thanks to bear markets, new technology and the euro. Liquidity and trading costs will decide who wins."International Financial Markets and the Firm Exercises + Solutions 1-5 ME2. A spot transaction can always be thought of as paying an amount of one currency to the bank, and in return for an amount of a second currency. Let us define the amount you pay to the bank as your input into the transaction, and the amount you receive in return as the output you get from the transaction. Let us further denote amounts of cash money of currency X by X. For example, define USD, as an amount of immediately available dollars, GBP, as an amount of immediately available pounds, and so on. Let us first familiarize ourselves with the concepts of input and output amounts: (a) If you sell an amount USD, for a total proceeds of DEM, which is the input amount? Which is the output amount? (b) If you buy an amount USD, for a total payment of DEM, which is the input amount? Which is the output amount? (c) If you sell an amount DEM, for GBP,, which is the input amount? Which is the output amount? We now have to discover which exchange rate, bid or ask, goes with each transaction: d) Define a "factor" to be either S or 1/S. If the spot rates quoted to you are S[USD/DEM]bid and S[USD/DEMJask, by what factor do you multiply the input amount to compute the corresponding output amount, when you buy DEM with USD? . when you sell DEM for USD? (Specify whether you multiply by S or 1/S, and whether you use bid or ask.) (e) If the spot rates quoted to you are S[DEM/GBP]bid and S[DEM/GBP]ask, by what factor do you multiply the input amount to compute the corresponding output amount, when you buy GBP with DEM? when you sell GBP for DEM? (f) In your answer to the two previous questions, verify the Law of the Worst Rate: Whenever the multiplication factor is S rather than 1/S-that is, whenever you multiply an input amount by an exchange rate-you use the smaller exchange rate (the bid rate). Whenever the factor is 1/S (that is, whenever you divide), you take the larger exchange rate (the ask rate). In short, the relevant rate is the one that produces the smaller output from a given input. Let us now consider triangular arbitrage and least cost dealing (g) Suppose that you convert an amount USD, into DEM,, and then immediately convert this latter amount into pounds, what is the ultimate output (in pounds)? (h) Suppose you then convert the proceeds GBP, obtained in question (g), back into dollars. What are the proceeds in dollars? (i) Use your answer in (h) to verify the Law of the Worst Possible Combination.In the triangular diagram above, a spot transaction is represented by an arrow that starts from the input amount and ends in the output amount. For example, to represent a spot conversion of USD into DEM, we draw an arrow from the box USD, {your input} to the box DEM; [the output to you}. The diagram helps you in fully understanding arbitrage and least-oost dealing computations. {ll fit} {I} {In} to} to) Complete the diagram by adding, next to each arrow, the factors by which you multiply the input amount to compute the output amount. {That is, if you divide an input by an exchange rate 51, dene the multiplication factor to be US, like in questions (d) and (e21). The rates to he used are 5[USDJ"DEM], S[DEhIffGEP], or Sl'USDJ'GBP], each time bid or ask. (in the diagram, trace the sequences of transactions described in questions (g) and {h}. For example, in question {g}, the route followed is USD, } DEM, } GEE. Verify that the ultimate output amount is obtained by multiplying the original input amount by all factors shown next to the arrows you are following. On the diagram, point out the alternative routes that you consider when you do a least- cost dealing computation for converting DEM into GDP. (in the diagram, point out the route that you follow when you verify whether or not there is a triangular arbitrage opportunity when converting USD into DEM, DEM into GDP, and GDP back into USD. In the above arbitrage computations, what is the ultimate dollar output when you start with an initial dollar input of USD, = 1'? (Hint: follow the arrows, and multiply by the factors next to each of them.) Then derive the no-arbitrage condition. In doing triangular arbitrage transactions like the one in question {n}, does it matter what the starting point is? Suppose you do arbitrage and least most dealing over four currencies rather than three. For example, suppose that you add the JPY to the diagram. Is there any additional insight obtained from a comparison of, say, the "quadrangular\" sequence USD, :r DEM, :> IPY, ) GB P, } UE'rDt to the triangular sequence USD, ) DEM,:r GDP, } USDJ' Exercises E1. You have just graduated from the University of Florida and are leaving on a whirlwind tour of Europe. You wish to spend USD 1,000 each in Germany, France, and Great Britian (USD 3,000 in total). Your bank offers you the following bid-ask quotes: USD/DEM 0.58-0.60, USD/FRF 0.16-0.18, and USD/GBP 1.48-1.51. (a) If you accept these quotes, how many DEM, FRF, and GBP do you have at departure? (b) If you return with DEM 300, FRF 1,000, and GBP 75, and the exchange rates are unchanged, how many USD do you have? (c) Suppose that instead of selling your remaining DEM 300 once you return home, you want to sell them in Paris. At the train station, you are offered FRF/DEM 3.33-3.55, while a bank three blocks from the station offers FRF/DEM 3.39-3.49. At what rate are you willing to sell your DEM 300? How many FRF will you receive?TO-MAPailing LACKCISCS ME1. When discussing triangular arbitrage and least-cost dealing, we considered only the spot market. (a) Is it also possible to construct synthetic forward deals? (b) If so, what are the synthetic forward bid and ask rates? (c) How should the actual (direct) forward rates be related to the synthetic rates