Answered step by step

Verified Expert Solution

Question

1 Approved Answer

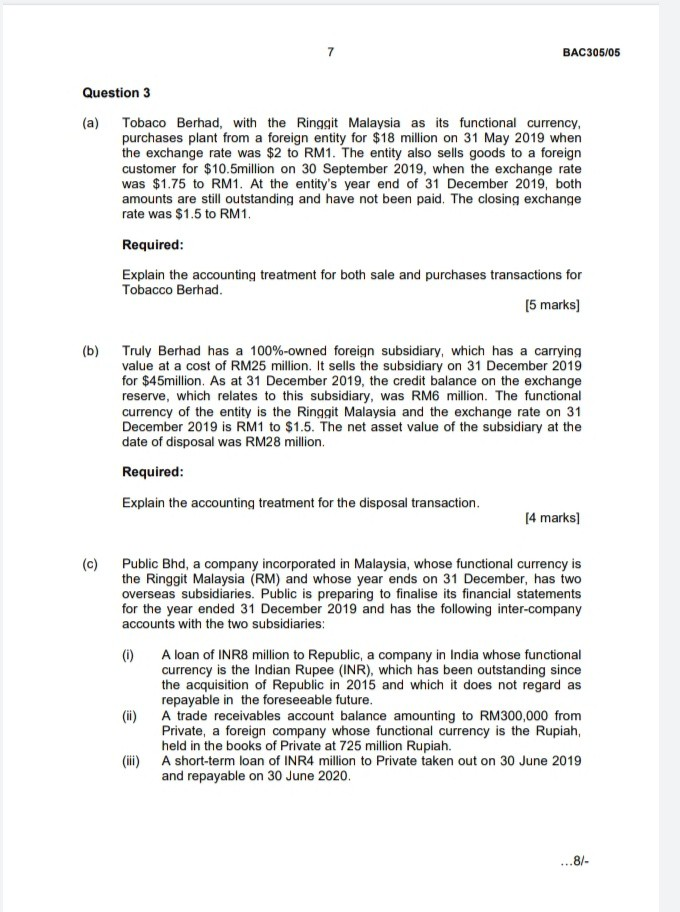

kindly please post me answer for both part (i)&(ii) thanks BAC305/05 Question 3 (a) Tobaco Berhad, with the Ringgit Malaysia as its functional currency, purchases

kindly please post me answer for both part (i)&(ii) thanks

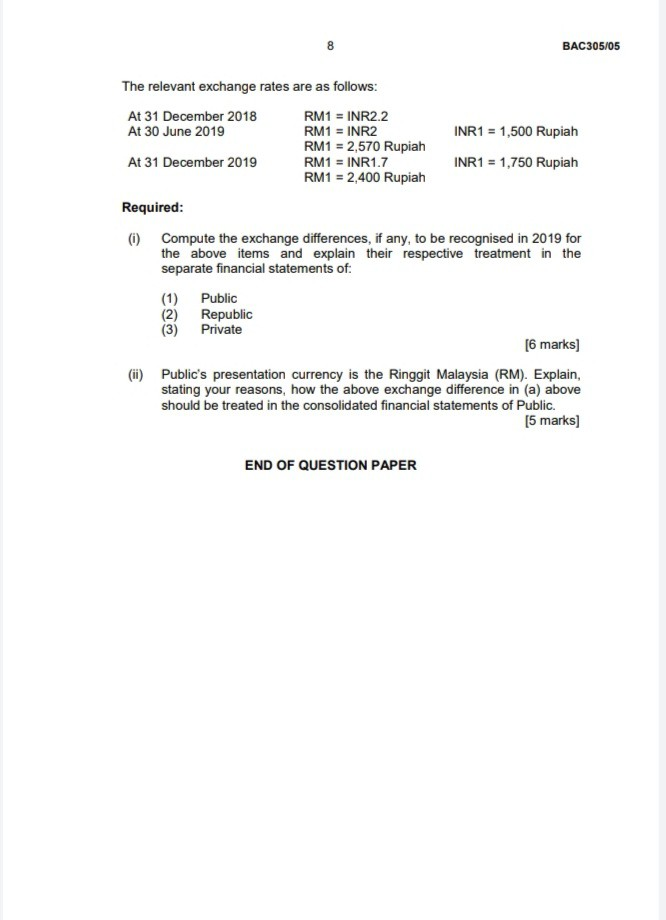

BAC305/05 Question 3 (a) Tobaco Berhad, with the Ringgit Malaysia as its functional currency, purchases plant from a foreign entity for $18 million on 31 May 2019 when the exchange rate was $2 to RM1. The entity also sells goods to a foreign customer for $10.5million on 30 September 2019, when the exchange rate was $1.75 to RM1. At the entity's year end of 31 December 2019, both amounts are still outstanding and have not been paid. The closing exchange rate was $1.5 to RM1. Required: Explain the accounting treatment for both sale and purchases transactions for Tobacco Berhad (5 marks) (b) Truly Berhad has a 100%-owned foreign subsidiary, which has a carrying value at a cost of RM25 million. It sells the subsidiary on 31 December 2019 for $45million. As at 31 December 2019, the credit balance on the exchange reserve, which relates to this subsidiary, was RM6 million. The functional currency of the entity is the Ringgit Malaysia and the exchange rate on 31 December 2019 is RM1 to $1.5. The net asset value of the subsidiary at the date of disposal was RM28 million. Required: Explain the accounting treatment for the disposal transaction. [4 marks) (c) Public Bhd, a company incorporated in Malaysia, whose functional currency is the Ringgit Malaysia (RM) and whose year ends on 31 December, has two overseas subsidiaries. Public is preparing to finalise its financial statements for the year ended 31 December 2019 and has the following inter-company accounts with the two subsidiaries: (0) A loan of INR8 million to Republic, a company in India whose functional currency is the Indian Rupee (INR), which has been outstanding since the acquisition of Republic in 2015 and which it does not regard as repayable in the foreseeable future. (ii) A trade receivables account balance amounting to RM300,000 from Private, a foreign company whose functional currency is the Rupiah, held in the books of Private at 725 million Rupiah. (ii) A short-term loan of INR4 million to Private taken out on 30 June 2019 and repayable on 30 June 2020. ...8/- 8 BAC305/05 The relevant exchange rates are as follows: At 31 December 2018 RM1 = INR2.2 At 30 June 2019 RM1 = INR2 INR1 = 1,500 Rupiah RM1 = 2,570 Rupiah At 31 December 2019 RM1 = INR1.7 INR1 = 1,750 Rupiah RM1 = 2,400 Rupiah Required: (0) Compute the exchange differences, if any, to be recognised in 2019 for the above items and explain their respective treatment in the separate financial statements of: (1) Public (2) Republic Private [6 marks) (ii) Public's presentation currency is the Ringgit Malaysia (RM). Explain, stating your reasons, how the above exchange difference in (a) above should be treated in the consolidated financial statements of Public. [5 marks) END OF QUESTION PAPER BAC305/05 Question 3 (a) Tobaco Berhad, with the Ringgit Malaysia as its functional currency, purchases plant from a foreign entity for $18 million on 31 May 2019 when the exchange rate was $2 to RM1. The entity also sells goods to a foreign customer for $10.5million on 30 September 2019, when the exchange rate was $1.75 to RM1. At the entity's year end of 31 December 2019, both amounts are still outstanding and have not been paid. The closing exchange rate was $1.5 to RM1. Required: Explain the accounting treatment for both sale and purchases transactions for Tobacco Berhad (5 marks) (b) Truly Berhad has a 100%-owned foreign subsidiary, which has a carrying value at a cost of RM25 million. It sells the subsidiary on 31 December 2019 for $45million. As at 31 December 2019, the credit balance on the exchange reserve, which relates to this subsidiary, was RM6 million. The functional currency of the entity is the Ringgit Malaysia and the exchange rate on 31 December 2019 is RM1 to $1.5. The net asset value of the subsidiary at the date of disposal was RM28 million. Required: Explain the accounting treatment for the disposal transaction. [4 marks) (c) Public Bhd, a company incorporated in Malaysia, whose functional currency is the Ringgit Malaysia (RM) and whose year ends on 31 December, has two overseas subsidiaries. Public is preparing to finalise its financial statements for the year ended 31 December 2019 and has the following inter-company accounts with the two subsidiaries: (0) A loan of INR8 million to Republic, a company in India whose functional currency is the Indian Rupee (INR), which has been outstanding since the acquisition of Republic in 2015 and which it does not regard as repayable in the foreseeable future. (ii) A trade receivables account balance amounting to RM300,000 from Private, a foreign company whose functional currency is the Rupiah, held in the books of Private at 725 million Rupiah. (ii) A short-term loan of INR4 million to Private taken out on 30 June 2019 and repayable on 30 June 2020. ...8/- 8 BAC305/05 The relevant exchange rates are as follows: At 31 December 2018 RM1 = INR2.2 At 30 June 2019 RM1 = INR2 INR1 = 1,500 Rupiah RM1 = 2,570 Rupiah At 31 December 2019 RM1 = INR1.7 INR1 = 1,750 Rupiah RM1 = 2,400 Rupiah Required: (0) Compute the exchange differences, if any, to be recognised in 2019 for the above items and explain their respective treatment in the separate financial statements of: (1) Public (2) Republic Private [6 marks) (ii) Public's presentation currency is the Ringgit Malaysia (RM). Explain, stating your reasons, how the above exchange difference in (a) above should be treated in the consolidated financial statements of Public. [5 marks) END OF QUESTION PAPERStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Conservation Easement Audit Techniques Guide

Authors: U.S. Internal Revenue Service

1st Edition

0359516998, 978-0359516995