Answered step by step

Verified Expert Solution

Question

1 Approved Answer

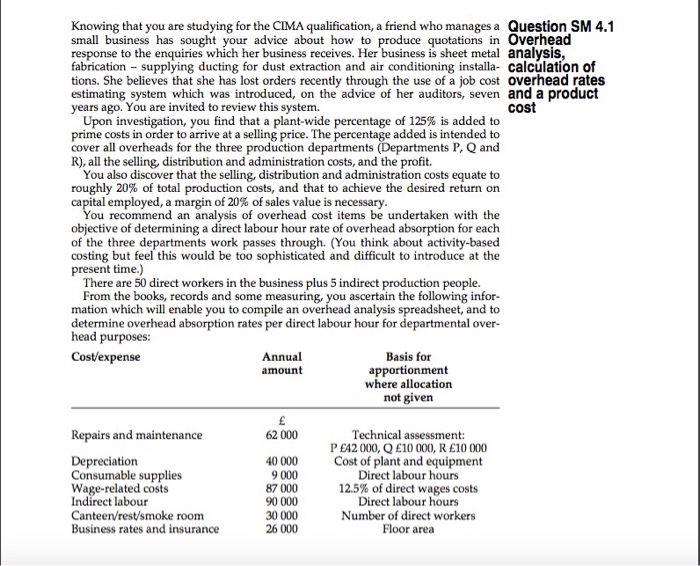

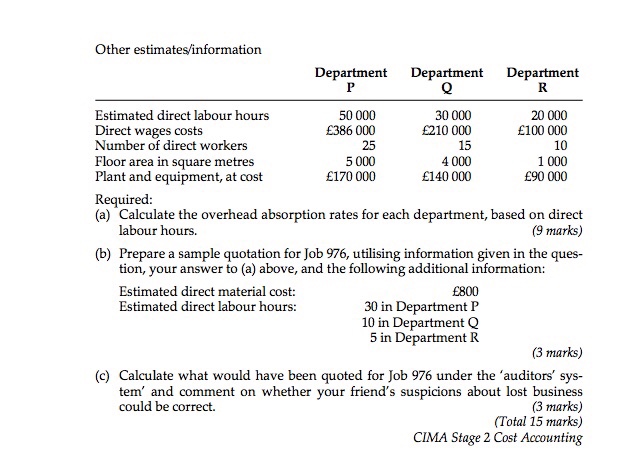

Knowing that you are studying for the CIMA qualification, a friend who manages a Question SM 4.1 small business has sought your advice about how

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Working Conditions And Factory Auditing In The Chinese Toy Industry

Authors: Congressional-Executive Commission On China

1st Edition

1508726515, 978-1508726517